Recent geopolitical escalations in the Middle East, specifically joint strikes involving the United States and Israel on Iran over the weekend, have ignited fresh concerns across global energy and logistics markets. While the immediate focus is on the potential for direct supply disruptions, the broader implications for shipping routes, freight costs, and ultimately, global energy prices, demand a close examination from investors. This analysis leverages proprietary market data and investor sentiment insights to offer a forward-looking perspective on navigating this complex environment, moving beyond mere headlines to actionable investment considerations.

Geopolitical Tensions and the Energy Market’s Nuanced Reaction

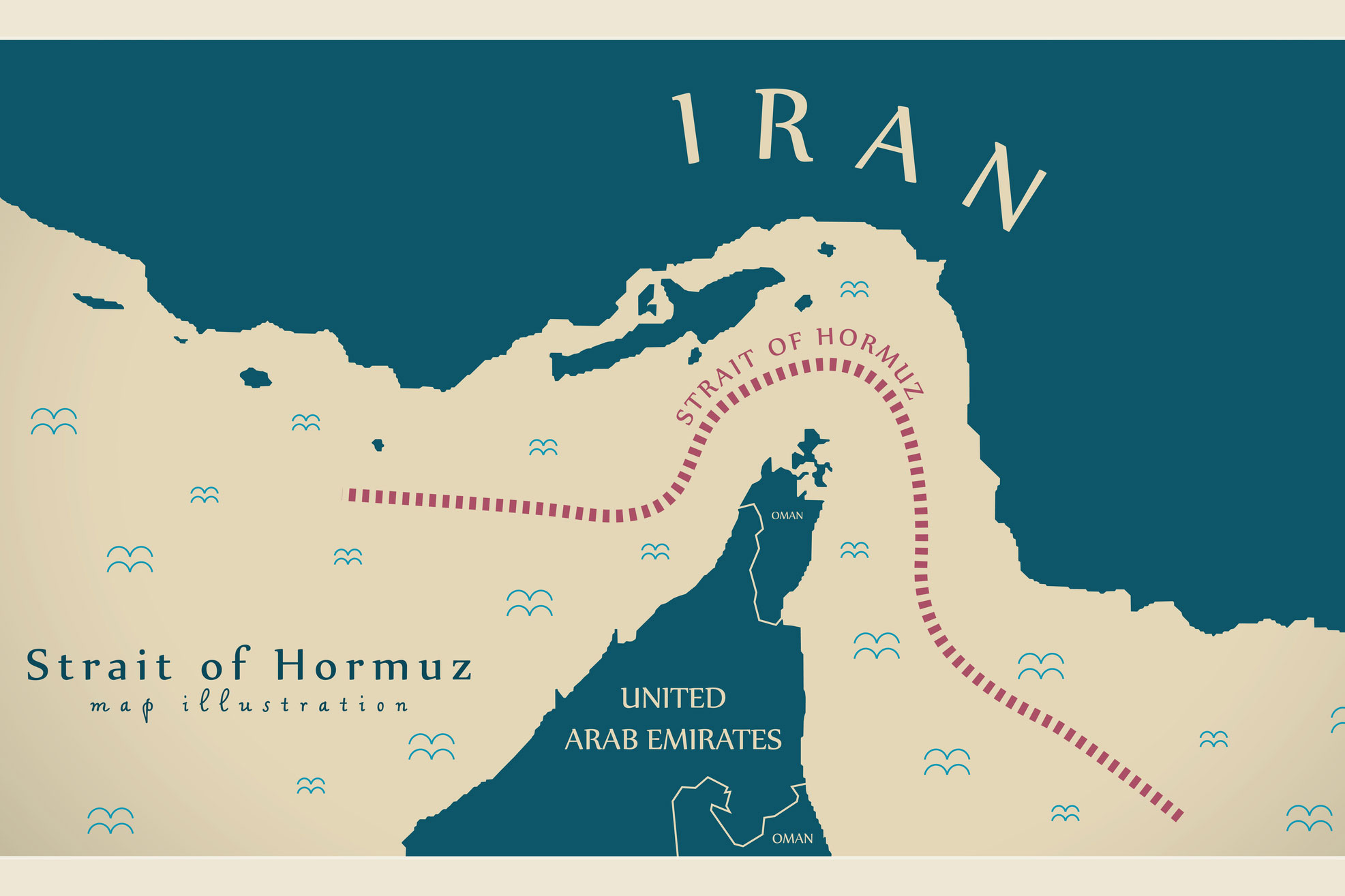

The latest military actions have intensified scrutiny on critical maritime chokepoints, particularly the Strait of Hormuz. This vital waterway is indispensable, facilitating the transit of approximately 20% of global petroleum liquids consumption and roughly one-third of the world’s seaborne crude oil, equating to between 17 million and 20 million barrels per day. Notably, nearly 90% of Saudi Arabia’s oil exports depend on this corridor. Compounding this vulnerability, shipping traffic in the Red Sea and Suez Canal, which typically handles 10% to 15% of global maritime trade, had only just begun to stabilize following earlier disruptions from Houthi militant attacks, underscoring the fragility of global supply lines.

Despite these significant geopolitical tremors, the immediate market reaction has shown a degree of tempered response. As of today, Brent Crude trades at $92.64, reflecting a -0.64% movement within a day range of $92.57-$94.21. WTI Crude is similarly down, standing at $89.03, a -0.71% shift within its $88.76-$90.71 range. Furthermore, our 14-day Brent trend data indicates a decline from $101.16 on April 1st to $94.09 on April 21st, a -7% drop. This suggests that while risk premiums are undoubtedly present, broader market dynamics, perhaps including demand concerns or a wait-and-see approach regarding the conflict’s sustained impact, are also influencing price discovery. Investors are clearly weighing the potential for disruption against other fundamental factors, preventing an immediate, sharp upward spike, but the underlying risk remains acutely elevated.

Monitoring Forward Indicators: Key Events for Oil & Gas Investors

In this environment of heightened uncertainty, vigilance over upcoming market data releases becomes paramount for energy investors. The next two weeks are packed with critical reports that will offer deeper insights into supply-demand balances and could significantly influence crude price trajectories. Our proprietary calendar highlights several key events:

- On April 22nd, and again on April 29th and May 6th, the EIA Weekly Petroleum Status Report will provide crucial data on U.S. crude oil and refined product inventories, production, and demand. Unexpected builds or drawdowns in crude stocks, especially against a backdrop of geopolitical tensions, could trigger notable market shifts.

- Investors should also closely watch the API Weekly Crude Inventory reports on April 28th and May 5th, which often precede EIA data and offer an early glimpse into inventory trends.

- The Baker Hughes Rig Count, scheduled for April 24th and May 1st, will offer a barometer of U.S. drilling activity, signaling future supply potential.

- Perhaps most significant for a mid-term outlook is the EIA Short-Term Energy Outlook on May 2nd, which will update projections for global supply, demand, and prices, incorporating the latest geopolitical developments into its forecasts.

These forward-looking data points, combined with ongoing news from the Middle East, will be instrumental in assessing whether current price levels accurately reflect the evolving risk landscape or if further adjustments are warranted. Investors should integrate these dates into their analytical frameworks to anticipate potential market volatility and position their portfolios accordingly.

Addressing Investor Concerns: WTI Outlook and Broader Market Dynamics

Our first-party reader intent data reveals a strong focus among OilMarketCap.com investors on the future direction of crude prices, particularly for WTI, with many explicitly asking about its trajectory through the end of 2026. This underscores a collective desire to understand how current geopolitical events will intersect with long-term fundamentals. The question “is WTI going up or down?” encapsulates the current market dilemma: on one hand, the Middle East conflict introduces significant upside risk due to potential supply disruptions and elevated freight costs. The apparent closing of the Strait of Hormuz for certain shipping lines and the prolonged disruption of Red Sea traffic have curtailed global fleet capacity, affecting vessels that represent roughly 2% of the global ocean container fleet, thereby pushing up ocean container rates and insurance premiums.

On the other hand, the market may be grappling with underlying demand concerns, especially if rising energy and freight costs begin to materially impact consumer discretionary spending and industrial activity. This complex interplay of bullish geopolitical catalysts and potentially bearish demand signals creates a challenging environment for price prediction. Investment strategies must therefore remain agile, balancing the immediate reactive potential of geopolitical events with the slower-moving forces of global economic health and demand elasticity. Investors are not just asking about today’s price, but about the sustained impact on their portfolios over the coming quarters and years, highlighting the need for a comprehensive view that integrates both macro and micro factors.

The Expanding Ripple: Freight Costs, Inflation, and Global Demand

The implications of sustained Middle East instability extend far beyond crude oil prices, creating a complex web of challenges for global commerce. The disruption to key maritime corridors will undeniably push container rates incrementally higher across various lanes as transit times lengthen and insurance premiums continue their upward climb. Shippers, seeking to mitigate delay risks, are likely to shift incremental volume to air cargo, which will in turn place upward pressure on airfreight rates across much of the region and beyond. This broader increase in logistics costs will not be confined to specific trade routes; it acts as an inflationary impulse across global supply chains, affecting goods from raw materials to finished products.

While the direct economic impact on U.S. and European markets might initially appear limited due to robust domestic supply chains for some goods, the indirect effects are undeniable. Higher energy costs, coupled with elevated freight expenses, will inevitably feed into producer prices and ultimately, consumer prices. This inflationary pressure could erode consumer purchasing power, potentially dampening discretionary expenditures and broader economic growth. For investors, this means a dual challenge: navigating the direct volatility in energy commodities while also considering the second-order effects on sectors reliant on global trade and consumer spending. The current geopolitical landscape is not merely an energy market event; it is a significant factor reshaping the global economic outlook and investment landscape for the foreseeable future.