The Accelerating EV Shift and Its Unfolding Impact on Oil Demand

The global energy landscape is undergoing a profound transformation, and the latest developments from the automotive sector underscore the intensifying pressure on future oil demand. BMW’s recent announcement regarding the series production of its sixth-generation electric drive unit for the ‘Neue Klasse’ vehicles at its Steyr plant is more than just a manufacturing milestone; it represents a significant step in scaling up advanced electric vehicle (EV) technology. For oil and gas investors, this move signals an accelerating decline in internal combustion engine (ICE) vehicle production, directly impacting gasoline consumption projections and challenging long-held demand growth assumptions. As major automakers commit substantial capital to EV infrastructure and innovative drivetrain technologies, the structural shift away from fossil fuels in personal transportation gains undeniable momentum, demanding a re-evaluation of long-term investment strategies within the energy sector.

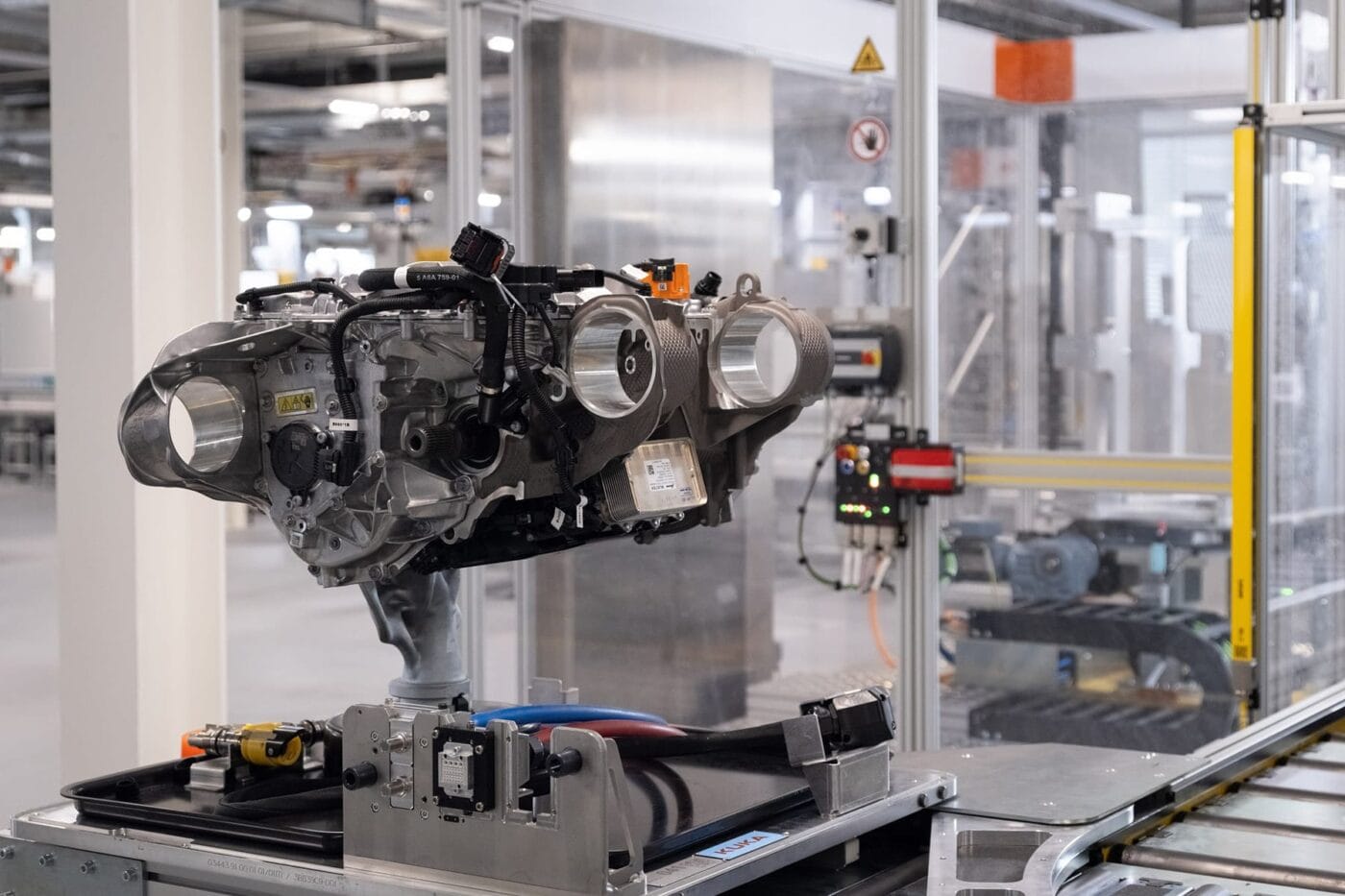

BMW’s Strategic Play: Scaling Up Efficiency and Cost Savings

BMW’s decision to bring the production of its Gen6 electric drive units in-house, particularly the complex inverter components, marks a pivotal strategic shift. The Steyr plant is now manufacturing these drives, leveraging a predominantly Austrian supply chain, with key components like rotors, stators, and inverters produced internally. Notably, the integration of silicon carbide (SiC) semiconductors within an 800-volt system and the adoption of a current-excited synchronous machine (SSM) design, which eliminates the need for permanent magnets, highlight a focus on both efficiency and resource independence. The modular production concept, designed to cater to the entire ‘Neue Klasse’ model range, is projected to generate “positive economies of scale and cost savings in both development and production.” This emphasis on manufacturing efficiency and cost reduction is critical. Cheaper, more efficient EVs translate directly to faster adoption rates, eroding the demand base for refined petroleum products, particularly gasoline, at an accelerated pace. For investors tracking the energy transition, BMW’s move signifies that the technological and economic hurdles to mass EV adoption are being systematically dismantled, solidifying the long-term bearish outlook for gasoline demand.

Navigating Market Volatility Amidst Structural Headwinds

The immediate volatility in crude markets often overshadows these crucial long-term structural shifts. As of today, Brent crude trades at $99.6 per barrel, showing a robust daily gain of 4.92%, with WTI crude similarly up 3.85% to $91.52. This daily rally, however, follows a significant retreat over the past two weeks, during which Brent shed 12.4%, dropping from $108.01 on March 26th to $94.58 just yesterday. Gasoline prices, currently at $3.08 per gallon, also reflect this short-term upward pressure. While these immediate price movements are driven by current supply-demand balances and geopolitical developments, they exist within an increasingly constrained long-term demand environment. The rapid advancements in EV production, exemplified by BMW’s scale-up, directly target and will ultimately depress the gasoline segment. Investors must dissect whether current price strength is a function of genuine, sustainable demand growth or temporary supply disruptions, understanding that the underlying fundamentals are steadily shifting due to advancements in electric mobility.

Upcoming Catalysts and Investor Outlooks

Our proprietary reader intent data reveals a consistent focus on forecasting crude prices, with many investors actively seeking a base-case Brent price forecast for the next quarter and the consensus 2026 outlook. While the long-term demand curve is undeniably influenced by developments like BMW’s accelerated EV production, the immediate horizon remains dominated by supply-side catalysts and inventory data. The upcoming OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting on April 18th, followed by the full Ministerial meeting on April 20th, will be critical. Any signals regarding production cuts or increases will have an immediate impact on price action. Furthermore, the API Weekly Crude Inventory reports on April 21st and 28th, alongside the EIA Weekly Petroleum Status Reports on April 22nd and 29th, will provide crucial insights into the near-term supply-demand balance in the U.S. These reports, coupled with the Baker Hughes Rig Count releases on April 17th and 24th, offer a granular view of drilling activity and potential future supply. For investors aiming to refine their short-to-medium-term Brent forecasts, scrutinizing the outcomes of these events is paramount, even as the shadow of long-term EV adoption grows larger.

Investment Implications: Beyond the Barrel of Oil

For sophisticated oil and gas investors, the narrative extends beyond simply the price per barrel. The rapid technological maturation and scaling of EV production, as showcased by BMW’s modular Gen6 e-drive system, necessitates a nuanced approach to portfolio construction. Companies heavily reliant on gasoline refining margins, for instance, face an increasingly challenging future. The question of how Chinese “tea-pot” refineries are running this quarter, a query frequently posed by our readers, gains added significance when viewed through the lens of long-term gasoline demand erosion. If global gasoline consumption is structurally declining, refining overcapacity, regardless of geographical location, will lead to sustained pressure on margins. Conversely, companies diversifying into renewable energy, carbon capture, or even advanced materials for EV components may present more resilient long-term opportunities. The focus on internal inverter production and SiC semiconductors by BMW underscores the burgeoning market for specialized components and power electronics within the EV ecosystem. Investors should scrutinize the capital expenditure plans and strategic pivots of integrated energy majors, distinguishing between those merely maintaining legacy assets and those actively investing in the infrastructure and technologies of the future energy economy. This strategic foresight is crucial for navigating an investment landscape increasingly shaped by the irreversible momentum of the energy transition.