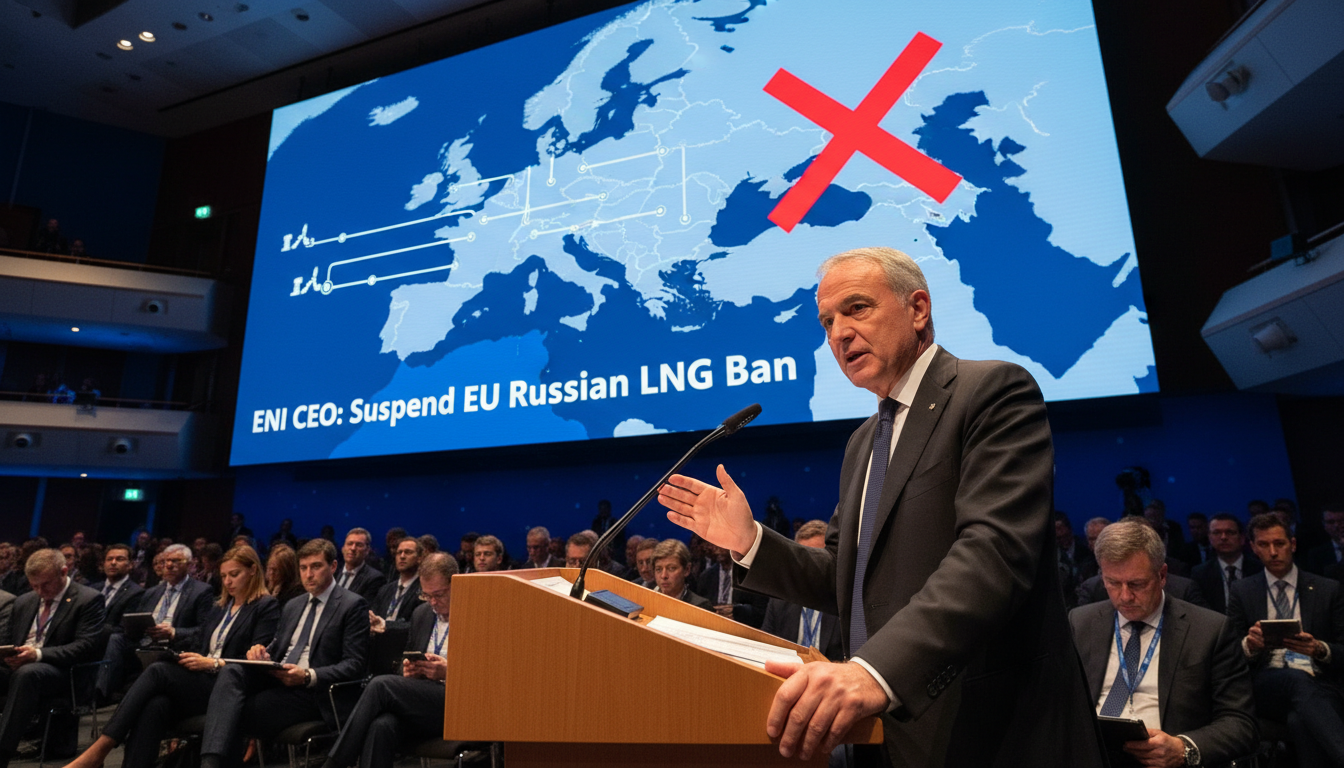

Urgent Call to Reassess EU’s Russian LNG Policy Amidst Global Market Upheaval

In a significant development for global energy markets and European energy security, Claudio Descalzi, the chief executive of Italian energy giant Eni, has advocated for a crucial suspension of the European Union’s impending ban on Russian Liquefied Natural Gas (LNG) imports. This prohibition is currently scheduled to take effect on January 1, 2027. Descalzi’s remarks underscore a growing apprehension within the industry regarding the profound market volatility triggered by escalating geopolitical tensions in the Middle East, a situation that demands immediate re-evaluation of established energy policies.

Speaking at a recent industry event, Descalzi articulated a compelling case for a strategic pause. “It is imperative that the ban on LNG supplies originating from Russia, set to commence on January 1, 2027, be suspended,” he stated. He clarified that his proposition was not for an outright abandonment of the policy but rather a temporary suspension or a more phased implementation. This approach, he argued, is vital to prevent further detrimental impacts on Europe’s industrial sector, which is already grappling with historically elevated energy costs and heightened operational pressures.

The EU’s Staggered Divestment from Russian Gas

The EU’s broader strategy involves a comprehensive, stepwise disengagement from all Russian gas imports by the close of 2027. This includes a prohibition on Russian LNG spot contracts, which came into force on April 25 of the current year. The complete cessation of LNG imports is targeted for the beginning of 2027, followed by a full ban on pipeline gas imports by the autumn of the same year. This ambitious timeline reflects Europe’s concerted effort to diminish its reliance on Russian energy, a policy initially driven by geopolitical imperatives following the conflict in Ukraine. Investors in the energy sector have been closely monitoring this transition, assessing its implications for long-term gas supply contracts, infrastructure development, and overall market stability.

Middle East Tensions Reshape Global LNG Dynamics

The strategic calculus underpinning Europe’s energy future has been significantly complicated by the protracted conflict in the Middle East. This geopolitical flashpoint has injected profound uncertainty into global energy shipping routes and supply chains. Critically, the absence of any LNG cargo transiting the Strait of Hormuz since the commencement of the conflict highlights the severe operational risks and the profound impact on shipping logistics. This disruption has had a direct and discernible effect on global LNG trade patterns. Asian buyers, facing their own regional supply concerns and keen to secure crucial energy resources, have aggressively turned to the spot market, frequently outbidding their European counterparts for available LNG volumes. This intense competition is emerging precisely when Europe requires robust and reliable supplies to adequately replenish its strategic gas storage facilities ahead of the next winter season, creating a challenging arbitrage environment for energy traders and utility companies.

Russia’s Strategic Repositioning and Conditional Offers

Concurrently, Russian officials have indicated a proactive shift in their energy export strategy. Last month, Moscow announced its intention to redirect LNG exports away from the European Union, signaling its readiness to move forward without waiting for the full implementation of the EU’s ban. This strategic pivot aims to secure new, reliable markets, predominantly in Asia, reflecting a recalibration of Russia’s long-term energy partnerships.

Adding another layer of complexity, Kremlin spokesman Dmitry Peskov recently suggested that Russia would be prepared to continue supplying natural gas to Europe, provided there are surplus volumes remaining after fulfilling the increased demands from other global markets. “Should gas volumes remain after meeting the needs of alternative markets, then why not?” Peskov remarked on Sunday. He further elaborated on the current supply landscape: “There is an abundance of gas available at present, and we possess spare capacity. However, these alternative markets exhibit substantial appetite and are submitting numerous requests for additional supplies.” This statement underscores Russia’s evolving posture as a global energy supplier, asserting its capacity while prioritizing burgeoning demand from non-European partners.

Investment Implications for a Volatile Energy Landscape

For investors navigating the intricate world of oil and gas, Descalzi’s call for a suspension of the Russian LNG ban carries significant implications. A potential policy reversal or delay would introduce a new dynamic into European gas pricing, potentially alleviating some of the upward pressure from fierce global competition. It would also signal a pragmatic recognition of immediate energy security needs over long-term strategic divergence. However, it also highlights the persistent geopolitical risks embedded within global energy supply chains and the challenging balancing act for policymakers between economic stability and political objectives.

Energy companies with substantial European exposure, particularly those involved in LNG regasification or gas-fired power generation, would closely monitor such developments. A continued, albeit temporary, reliance on Russian LNG could impact investment decisions in new non-Russian LNG import infrastructure projects, potentially altering their economic viability and return profiles. Furthermore, the competitiveness of Europe’s industrial sector hinges critically on stable and affordable energy. Any measure that mitigates energy costs, even if politically sensitive, would be viewed positively by industries seeking to maintain their global standing.

The dynamic interplay between Middle Eastern geopolitical instability, Asian demand growth, European energy policy shifts, and Russia’s evolving export strategy creates a complex, high-stakes environment for natural gas markets. Investors must remain vigilant, analyzing how these interwoven factors will shape future supply-demand balances, price trajectories, and the strategic direction of major energy players. The discussion around Russian LNG is not merely about volumes; it is about the very resilience and adaptability of the global energy system in a turbulent world.