The geopolitical landscape of global energy supply is undergoing a significant shift, with Venezuela once again emerging as a focal point. The recent US administration announcement regarding the oversight of Venezuelan crude sales signals a pivotal moment for the beleaguered nation’s oil industry and, by extension, the international energy market. This strategy aims to leverage Venezuela’s vast crude reserves not just for economic reconstruction but also to exert strategic influence, promising a complex interplay of politics, economics, and energy security. For investors, understanding the nuances of this evolving situation – from potential supply injections to the investment opportunities for international oil companies – is paramount in navigating the coming months.

The Geopolitical Calculus of Venezuelan Crude

The US administration’s explicit intent to control the flow of Venezuelan oil and its associated revenues represents a direct intervention designed to rebuild the nation’s economy and ensure stability. Energy Secretary Chris Wright articulated this strategy, emphasizing the leverage gained by overseeing oil sales and the resulting cash flow to drive necessary changes within Venezuela. This goes beyond mere sanctions relief; it’s a proactive approach to manage a critical energy asset. President Trump’s earlier statement about Venezuela relinquishing 50 million barrels of oil to the US, valued at approximately $2.8 billion at the time of the announcement in January, highlights the immediate financial component of this strategy. These funds, intended for deposit into government accounts overseen by the US, aim to directly benefit the Venezuelan populace while being protected from existing creditors.

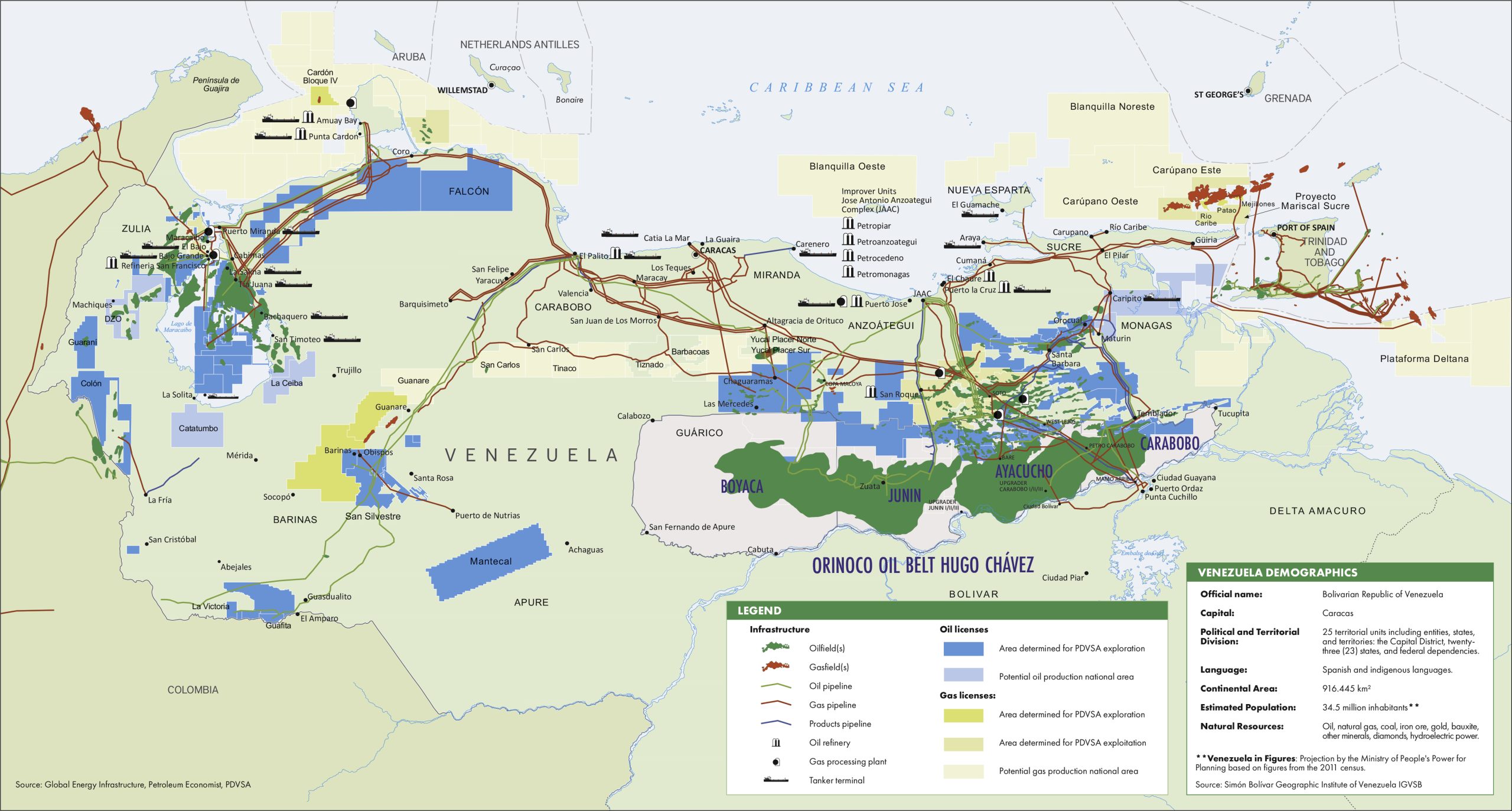

The move also signals a gradual easing of sanctions, paving the way for a resurgence of foreign investment. Major US oil companies, including Chevron Corp., ConocoPhillips, and Exxon Mobil Corp., are reportedly being encouraged to participate in rebuilding Venezuela’s dilapidated oil infrastructure. Years of corruption, underinvestment, and neglect have crippled the industry, driving production to less than 1 million barrels per day (MMbpd). While restoring the sector to its former glory would be a monumental undertaking, estimated to cost $10 billion annually over the next decade, the short to medium-term potential is significant. Secretary Wright estimated output could increase by several hundred thousand barrels a day relatively quickly, a volume that could materially impact global crude markets.

Market Volatility and the Venezuelan Supply Horizon

The potential re-entry of Venezuelan crude into global markets arrives at a dynamic period for oil prices. As of today, Brent crude trades at $90.57, reflecting a modest daily gain of 0.15%, yet within a day range of $93.87-$95.69, indicating underlying volatility. WTI crude, similarly, is at $87.38, down 0.05%, with a daily range of $85.50-$87.63. These figures underscore a market grappling with supply concerns and demand fluctuations. Our proprietary market trend data reveals a more significant shift over the past two weeks, with Brent crude declining from $118.35 on March 31st to $94.86 by April 20th – a substantial drop of 19.8% or $23.49 per barrel. This recent downward pressure suggests that while the market is still robust, it is highly sensitive to changes in supply expectations and macroeconomic indicators.

In this context, even an increase of “several hundred thousand barrels a day” from Venezuela could exert additional downward pressure, especially if the broader demand outlook weakens. The initial commitment of 50 million barrels, valued at approximately $2.8 billion at the time of the announcement in January, would fetch a considerably higher sum in today’s market given Brent’s current trading levels. This provides a compelling financial incentive for the US and Venezuela to accelerate production. However, the long-term investment required to fully rejuvenate the industry – $10 billion per year over a decade – highlights that any substantial, sustained supply increase will be a gradual process, not an immediate flood of new barrels. Investors should temper expectations for rapid, transformative supply boosts and instead focus on the incremental steps and the capital commitments from IOCs.

Upcoming Events and the Future of Oil Supply

The reintroduction of Venezuelan crude will undoubtedly be a key discussion point in upcoming energy events, influencing supply-demand forecasts and investment decisions. Our internal calendar highlights several critical dates for investors to monitor. On April 21st, the OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting will take place. This gathering is crucial as the cartel assesses market conditions and potential production adjustments. Any discussion of increased non-OPEC+ supply, such as from Venezuela, could influence their output strategy, potentially leading to a more cautious approach from the group.

Further insights into global supply and demand dynamics will come from the EIA Weekly Petroleum Status Reports, scheduled for April 22nd and April 29th, and the API Weekly Crude Inventory reports on April 28th and May 5th. These reports provide granular data on US crude inventories, refining activity, and product demand, offering a real-time pulse of the market’s health. Significant builds or draws could indicate how well the market is absorbing existing supply and its readiness for potential Venezuelan additions. Finally, the EIA Short-Term Energy Outlook (STEO) on May 2nd will offer a more comprehensive forecast, likely incorporating initial assessments of the Venezuelan situation and its projected impact on global balances through the end of 2026 and into 2027. Investors should scrutinize these reports for any revisions to supply forecasts or demand projections that account for a potentially revitalized Venezuelan oil sector.

Addressing Investor Concerns: Price Trajectories and Company Upside

Investor sentiment, as reflected in our reader intent data, frequently queries the immediate trajectory of WTI and the long-term oil price outlook. Many are asking “what do you predict the price of oil per barrel will be by end of 2026?” The re-emergence of Venezuelan supply adds another layer of complexity to these forecasts. While the potential for several hundred thousand additional barrels per day from Venezuela could theoretically weigh on prices, the actual impact will depend on the pace of restoration, global demand growth, and OPEC+’s response. Given the significant investment required, a rapid increase is unlikely. Therefore, the market’s focus should be on the gradual, long-term implications rather than immediate price collapses.

Beyond price, investors are also keenly interested in company-specific performance, with questions like “How well do you think Repsol will end in April 2026” highlighting the focus on international oil company (IOC) exposure. For investors eyeing the Venezuelan opportunity, the involvement of US majors like Chevron, ConocoPhillips, and Exxon Mobil presents a clear, albeit risky, upside. These companies possess the technical expertise, capital, and operational experience to rehabilitate Venezuela’s infrastructure. However, the challenges are immense: political stability, legal frameworks, and the sheer scale of investment required. Successful re-engagement could unlock significant long-term value for these firms, offering access to some of the world’s largest crude reserves at potentially attractive entry points. Investors should meticulously evaluate the risk-reward profile of companies with direct or indirect exposure to Venezuela, focusing on those with a proven track record in challenging operating environments and a clear strategy for phased investment and production ramp-up.