The Strategic Imperative of Offshore Asset Life Extension in the U.S. Gulf: A Deep Dive for Investors

For investors keenly observing the North American energy landscape, particularly the prolific U.S. Gulf of Mexico, the future of mature offshore assets presents a critical juncture. Operators are increasingly confronted with a strategic choice: either incur the substantial costs of decommissioning aging infrastructure or unlock significant long-term value by extending their operational lives. This decision transcends mere engineering; it represents a pivotal capital allocation strategy directly impacting future cash flows, asset valuations, and ultimately, shareholder returns in the deepwater arena. Many deepwater facilities, originally commissioned between the late 1990s and early 2000s, are now approaching the end of their initial 20-to-25-year permit periods. Understanding the stringent regulatory environment, particularly the Bureau of Safety and Environmental Enforcement (BSEE) mandates for proving an asset’s continued fitness-for-purpose, is paramount for investors looking to evaluate the true potential of these crucial energy producers.

The Multi-Billion Dollar Calculus: Decommissioning vs. Value Creation

The financial implications driving life extension decisions are stark and immediately impact an operator’s bottom line. Decommissioning a deepwater asset can easily run into the hundreds of millions of dollars, representing a direct hit to profitability and a permanent removal of valuable production capacity that is both costly and complex to replace. Conversely, extending an asset’s life transforms a sunk cost into an ongoing revenue stream. Consider a deepwater development with an initial price tag of $5 billion. Over its original permit period, this significant capital outlay is typically recovered. Every single barrel produced beyond that point carries a substantially higher margin, directly bolstering profitability and generating immense value from infrastructure that has already paid for itself. This powerful financial logic underscores the appeal of life extension, but it hinges entirely on an operator’s ability to definitively prove the integrity of the asset, especially its critical subsea pipeline and riser infrastructure, to meet rigorous safety and regulatory benchmarks. Failure to secure this proof in a timely manner carries significant commercial risk, potentially forcing premature decommissioning.

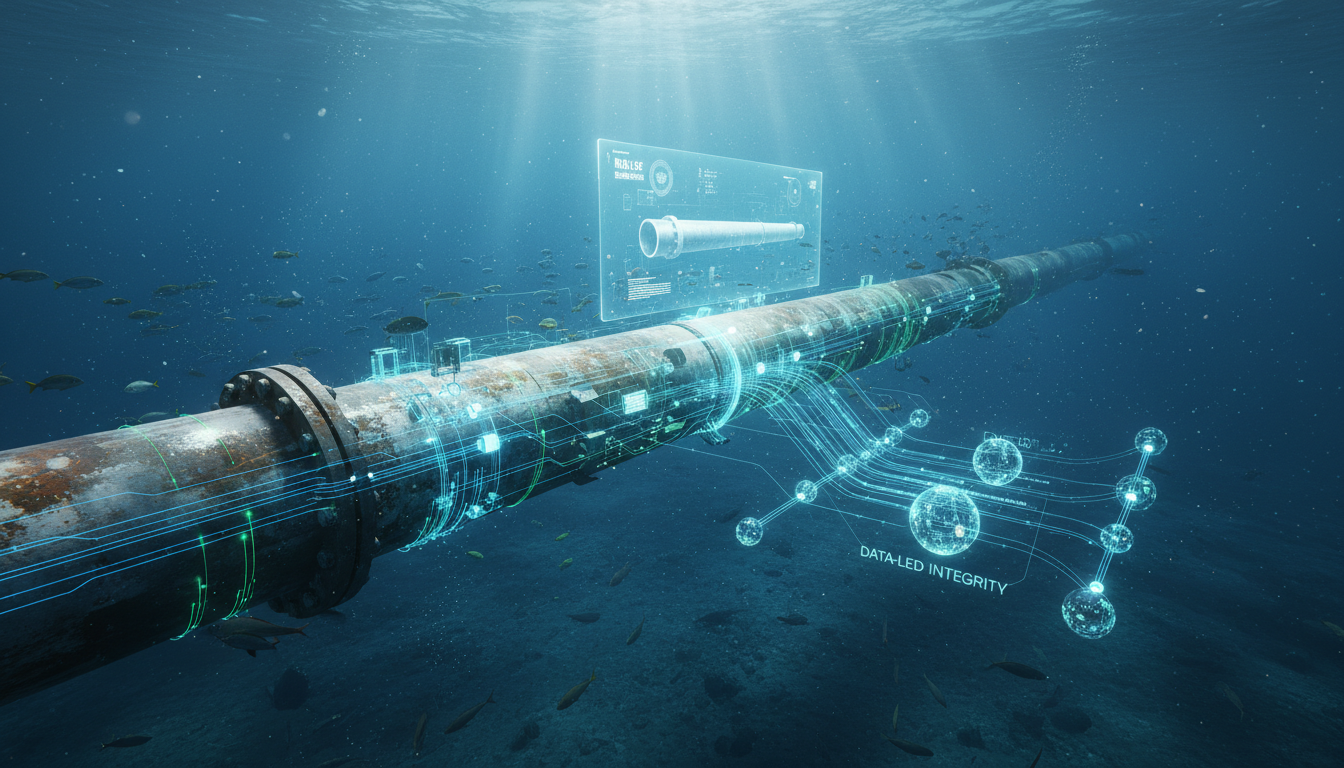

Navigating Regulatory Rigor and Data-Driven Integrity Management

The decision to pursue life extension is not simply a technical assessment; it is a strategic business imperative intricately linked to production economics, the physical condition of the assets, regulatory mandates, and the operator’s inherent risk appetite. For many mature U.S. Gulf assets, the commercial argument for extension is robust. These facilities, optimized over decades with established production infrastructure and experienced teams, offer an efficient and stable base for continued output. The BSEE requires comprehensive evidence of an asset’s continued fitness-for-purpose, demanding robust integrity management programs. This is where advanced data analytics and monitoring technologies become critical. Operators who proactively invest in real-time structural health monitoring, corrosion detection, and predictive maintenance protocols for their subsea pipelines and risers are best positioned to demonstrate compliance. Our proprietary data pipelines, tracking operational efficiency and integrity management investments across the sector, indicate a growing trend among leading operators to leverage digital twins and AI-powered inspection tools to provide the granular, verifiable data necessary to satisfy BSEE requirements and secure these valuable extensions. This proactive, data-centric approach minimizes regulatory risk and safeguards future production.

Market Dynamics and Investor Sentiment: Gauging Offshore Value in a Volatile World

The current market environment provides a critical backdrop for these strategic life extension decisions. As of today, Brent crude trades at $99.13, reflecting a modest 0.22% decline on the day, having ranged between $97.55 and $101.32. WTI Crude currently stands at $94.4, experiencing a 1.51% decline, with a daily range of $92.68-$97.85. This recent softening contrasts with the broader trend over the past two weeks, where Brent has fallen by $9.49, or 8.7%, from $109.27 on April 7th. Our proprietary reader intent data reveals a keen focus on price drivers, with investors frequently asking, “What would push Brent below $80? What would push it above $120?” These questions underscore the market’s sensitivity to supply stability and geopolitical factors. In such a volatile pricing landscape, the predictable, lower-cost production from extended deepwater assets becomes increasingly attractive. These proven facilities offer a reliable base load of supply, mitigating some of the exploration risk associated with new projects and providing a stable return stream that is highly valued during periods of price uncertainty. Furthermore, while investors are also exploring “What’s the impact of EV adoption on long-term oil demand projections?”, the consensus remains that conventional oil and gas will continue to play a critical role for decades, making sustained production from existing infrastructure economically prudent.

Upcoming Events and the Long-Term Outlook for Deepwater Investment

The strategic value of offshore asset life extension is continuously shaped by broader market intelligence. The coming weeks will offer fresh insights that influence investment decisions. Key events on the calendar include the API Weekly Crude Inventory reports on April 28th and May 5th, followed by the EIA Weekly Petroleum Status Reports on April 29th and May 6th. These provide crucial snapshots of U.S. supply and demand dynamics. Additionally, the Baker Hughes Rig Count on May 1st and May 8th will indicate drilling activity, while the EIA Short-Term Energy Outlook on May 2nd will offer a macro perspective on future price and demand projections. Strong demand signals from EIA reports or stable rig counts could further reinforce the investment case for extending existing, low-cost deepwater production, rather than diverting capital to higher-capex new developments. Investors recognize that maintaining and optimizing existing infrastructure is often the most capital-efficient path to sustained output. Therefore, the ability of operators to demonstrate rigorous asset integrity and secure life extensions is not just a regulatory compliance matter; it’s a strategic pillar for long-term value creation in the U.S. Gulf, ensuring stable returns and positioning companies favorably amidst evolving market conditions.