The global energy landscape continues its multifaceted transformation, offering both compelling opportunities and complex challenges for oil and gas investors. A recent agreement between Japan’s power giant JERA Co. Inc. and lifestyle retailer Ryohin Keikaku Co. Ltd., operator of the Muji brand, to establish Muji Energy LLC, serves as a poignant illustration of this shift. While seemingly a niche renewable venture, this partnership, alongside JERA’s broader decarbonization initiatives in carbon capture and ammonia co-firing, provides critical signals for investors navigating the evolving energy sector. It highlights how major energy players are adopting diversified strategies to meet net-zero targets, impacting the long-term outlook for traditional fossil fuel demand and infrastructure.

Muji Energy: A Blueprint for Corporate Green Transformation

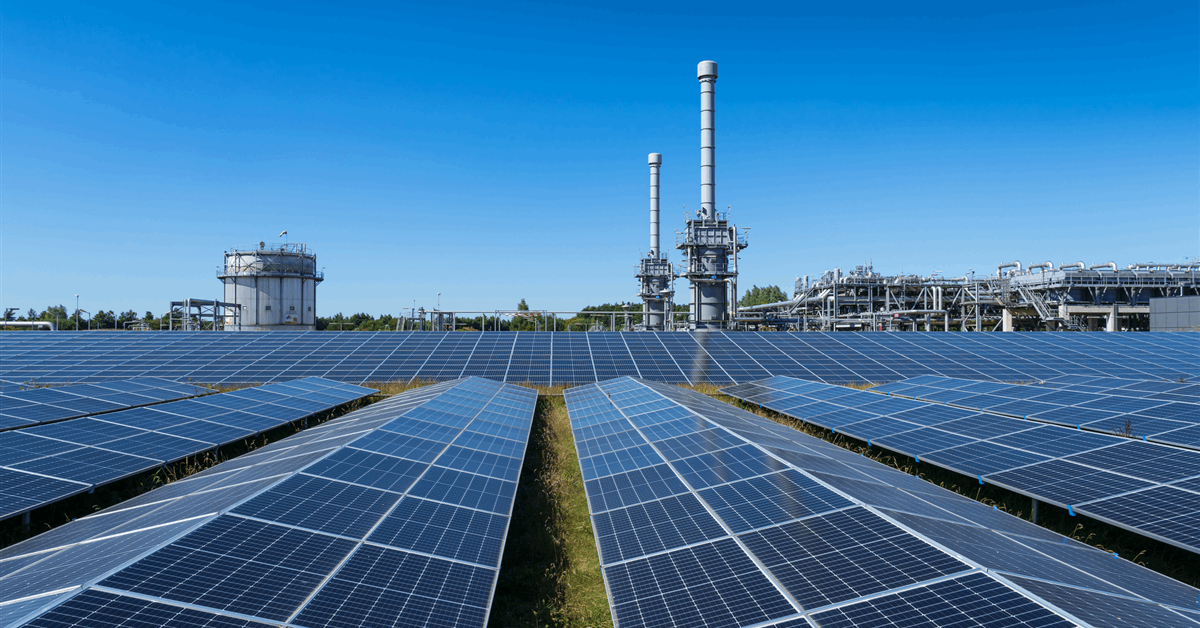

The formation of Muji Energy LLC, a special purpose company dedicated to developing and operating solar power generation facilities, marks a significant step in corporate green transformation. This joint investment with Ryohin Keikaku is not merely symbolic; it aims for tangible results. Muji Energy plans to develop approximately 13 megawatts (MW) of power generation capacity within its first year. This capacity is projected to cover 20 percent of Ryohin Keikaku’s annual electricity consumption and reduce its CO2 emissions by an estimated 8,000 tons per year. Furthermore, the accompanying virtual power purchase agreement (V-PPA) with JERA subsidiary JERA Cross Co. Inc. will supply renewable energy to the Japan Electric Power Exchange (JEPX), demonstrating a commitment beyond internal consumption.

Ryohin Keikaku’s ambitious target of a 50 percent reduction in total Scope 1 and 2 greenhouse gas emissions by fiscal 2030, compared to fiscal 2021, underscores the increasing pressure on corporations to decarbonize their operations. JERA Cross, as a “one-stop partner” for corporate green transformation, exemplifies a growing segment of the energy market focused on providing strategic and technical expertise for renewable energy integration and energy management. For investors, this trend highlights the expanding demand for renewable energy solutions and the companies that facilitate their deployment, creating new avenues for growth that are intrinsically linked to corporate ESG mandates and sustainability goals.

JERA’s Dual-Track Decarbonization: Beyond Renewables

JERA’s strategy extends far beyond direct renewable energy generation like the Muji Energy venture. The company’s comprehensive “Zero CO2 Emissions 2050” initiative encompasses a dual-track approach that includes both expanding renewable energy and developing “zero-emissions” thermal power. This becomes evident in their concurrent efforts in carbon capture, utilization, and storage (CCUS) and ammonia co-firing technologies.

A memorandum of understanding with Kawasaki Heavy Industries Ltd. (KHI) for a joint study on building a CCUS value chain at the Yokosuka Thermal Power Station by 2030 is particularly noteworthy. This pilot-scale testing of KHI’s carbon capture equipment at a coal-fired thermal power plant on Tokyo Bay represents a pioneering effort in a critical industrial region. Simultaneously, JERA has already achieved a significant milestone with the world’s first demonstration testing of 20 percent substitution of fuel ammonia at a large-scale commercial coal-fired thermal power plant in Hekinan City. These initiatives reveal a pragmatic approach to decarbonization that acknowledges the enduring role of thermal power in energy security, while aggressively pursuing technologies to mitigate its emissions. For oil and gas investors, JERA’s strategy signals continued investment in advanced thermal power solutions and highlights the potential for companies specializing in CCUS technology, hydrogen production, and ammonia supply chains as crucial enablers of this transition.

Navigating Volatility: Market Signals Amidst Transition

While the long-term energy transition narrative gains momentum, the immediate dynamics of the oil and gas markets continue to demand investor attention. As of today, Brent crude trades at $90.38 per barrel, marking a significant single-day decline of 9.07%, with prices ranging from $86.08 to $98.97. Similarly, WTI crude is at $82.59, down 9.41%. This substantial single-day drop contributes to a broader trend; Brent has fallen from $112.78 on March 30th to $91.87 just yesterday, representing an 18.5% decrease over the past two weeks.

This market volatility is a constant for oil and gas investors. While companies like JERA are making strides in renewables and decarbonization, the profitability and capital allocation decisions of many energy firms remain heavily influenced by crude prices. A sharp decline in oil prices can impact investment appetite for new projects, whether conventional or transitional, by affecting cash flows and perceived returns. Investors are keenly observing how this volatility affects the balance sheets of exploration and production companies, the viability of marginal projects, and the overall economic backdrop against which the energy transition unfolds. The significant drop in gasoline prices to $2.93, down 5.18%, further underscores the current shift in energy commodity valuations.

Forward Look: Upcoming Events and Investor Concerns

The near-term trajectory of oil prices remains a dominant concern for investors, a sentiment echoed by frequent questions we see from our readers, such as “what do you predict the price of oil per barrel will be by end of 2026?” and queries about “OPEC+ current production quotas.” With Brent prices showing significant weakness, declining nearly 18.5% over the past two weeks, all eyes will be on the upcoming OPEC+ Joint Ministerial Monitoring Committee (JMMC) and full Ministerial meetings scheduled for April 18th and 19th.

These crucial meetings have the potential to significantly influence global supply dynamics. Any decisions regarding production levels will directly impact market sentiment and price stability, which in turn affects the financial calculus for both traditional oil and gas projects and the broader energy transition. Beyond OPEC+, investors will also be closely monitoring the API Weekly Crude Inventory reports on April 21st and 28th, the EIA Weekly Petroleum Status Reports on April 22nd and 29th, and the Baker Hughes Rig Count on April 24th and May 1st. These recurring data points offer granular insights into immediate supply and demand balances within the U.S. market, providing critical context for broader investment strategies. Understanding how these near-term market catalysts interact with long-term decarbonization trends, like JERA’s diversified approach, is essential for informed decision-making in the complex and evolving energy sector.