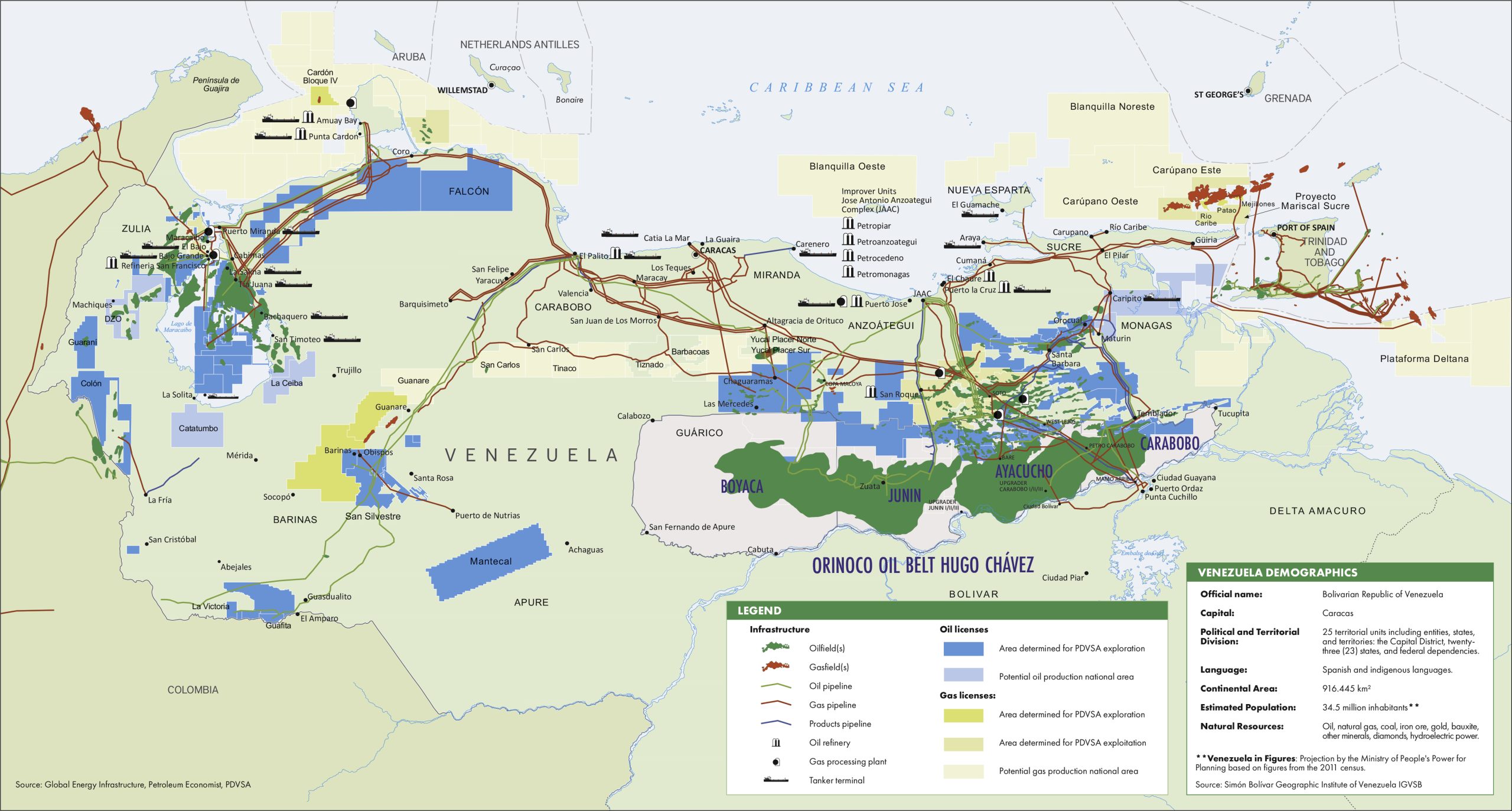

The prospect of reviving Venezuela’s vast oil sector is once again dominating discussions among global energy executives and policymakers. With the recent political shift in Caracas, the U.S. administration is making a concerted push to bring American oil companies back into the fold, hoping to unlock a significant new source of crude for the global market. This week, U.S. Energy Secretary Chris Wright is slated to engage with industry leaders, including those from Chevron Corp. and ConocoPhillips, at the Goldman Sachs Energy, Clean Tech & Utilities Conference in Miami. While Venezuela boasts the world’s largest proven oil reserves, the path to revitalization is anything but straightforward, presenting a complex risk-reward matrix for investors closely monitoring the energy landscape.

Geopolitical Shifts and Market Dynamics

The U.S. government’s proactive stance on Venezuela’s energy future marks a pivotal moment, signaling a potential seismic shift in global oil supply. President Trump’s administration is clearly banking on U.S. companies to repair and expand infrastructure that has suffered from years of underinvestment and neglect. This renewed focus comes at a time when global oil markets are navigating a period of volatility. As of today, Brent crude trades at $90.59, registering a modest daily gain of 0.18%, yet notably down from its recent highs. For context, Brent has seen a significant decline of nearly 20% in the last two weeks alone, falling from $118.35 on March 31st to $94.86 just yesterday, before dipping further. Similarly, WTI crude stands at $87.39. This softening market environment could make the prospect of substantial new supply from Venezuela, should it materialize, a key factor for investors assessing future price trajectories. While the long-term potential is immense, with estimates suggesting Venezuela could eventually add millions of barrels per day to global output, the immediate market impact will depend heavily on the pace and scale of investment.

The Steep Climb to Rejuvenation: Investor Concerns and Capital Needs

Despite the allure of Venezuela’s colossal reserves, oil companies are approaching the situation with understandable caution. Industry experts estimate that rebuilding the nation’s ravaged energy infrastructure will demand an staggering $10 billion annually for the next decade, totaling $100 billion. This colossal capital outlay requires more than just political will from Washington; it demands a robust, stable operating environment. Investors are keenly aware of the inherent risks, frequently asking about the future direction of prices, with questions such as “is WTI going up or down?” and “what do you predict the price of oil per barrel will be by end of 2026?” These long-term price outlooks are directly impacted by the potential for new supply from regions like Venezuela. Companies, including those like Repsol, which some of our readers inquire about, need concrete assurances: a stable government, unwavering rule of law, and a long-term commitment from the U.S. government that transcends any single administration. Without these foundational elements, the significant upfront investment needed for a multi-year redevelopment project remains a highly speculative venture.

Navigating Upcoming Events and Future Outlook

The discussions taking place this week are merely the beginning of a long journey, and investors will need to closely monitor a series of upcoming events that will influence the broader oil market and the feasibility of Venezuelan projects. The OPEC+ Joint Ministerial Monitoring Committee (JMMC) Meeting, scheduled for today, April 21st, is critical. Any signals regarding current production quotas or future supply management could impact the market’s receptiveness to additional Venezuelan crude. Later this week, on April 22nd and April 29th, the EIA Weekly Petroleum Status Reports will provide fresh insights into U.S. crude inventories and demand, offering short-term market direction. The Baker Hughes Rig Count reports on April 24th and May 1st will indicate North American drilling activity, another key supply indicator. Perhaps most importantly for forward-looking analysis, the EIA Short-Term Energy Outlook on May 2nd will offer official projections that could factor in the evolving Venezuelan situation, shaping investor expectations for the remainder of 2026 and beyond. These data points, combined with ongoing geopolitical developments, will paint a clearer picture of the investment climate.

Strategic Stakes for Oil Majors

The potential reopening of Venezuela’s oil sector holds immense strategic implications for global supermajors. Chevron Corp. stands in a unique position, being the only major international oil company that maintained operations in Venezuela through the turbulent years. This gives them a significant head start should conditions stabilize. However, the re-entry of other players like ConocoPhillips, which previously had substantial assets in the country, would intensify the competitive landscape. For these companies, the decision to commit billions to Venezuela isn’t just about potential returns; it’s about portfolio diversification, long-term reserve replacement, and strategic positioning in an energy-hungry world. While the short-term market remains fixated on daily price fluctuations – such as WTI’s current level of $87.39 – the long-term vision for these energy giants involves securing future production in regions with proven, vast resources. The discussions in Miami this week will provide crucial early signals on how aggressively these companies, under the careful watch of their shareholders, are willing to pursue Venezuela’s challenging but undeniably rich opportunities.