As Super Typhoon Sinlaku barrels through the Pacific, investors are keenly watching its trajectory and potential implications for regional stability and, by extension, global energy supply chains. While the immediate impact on major oil production hubs may seem distant, such extreme weather events serve as a stark reminder of the inherent vulnerabilities in global logistics and infrastructure. For astute oil and gas investors, understanding these risks and their interplay with broader market fundamentals and upcoming catalysts is crucial for navigating what promises to be a volatile period.

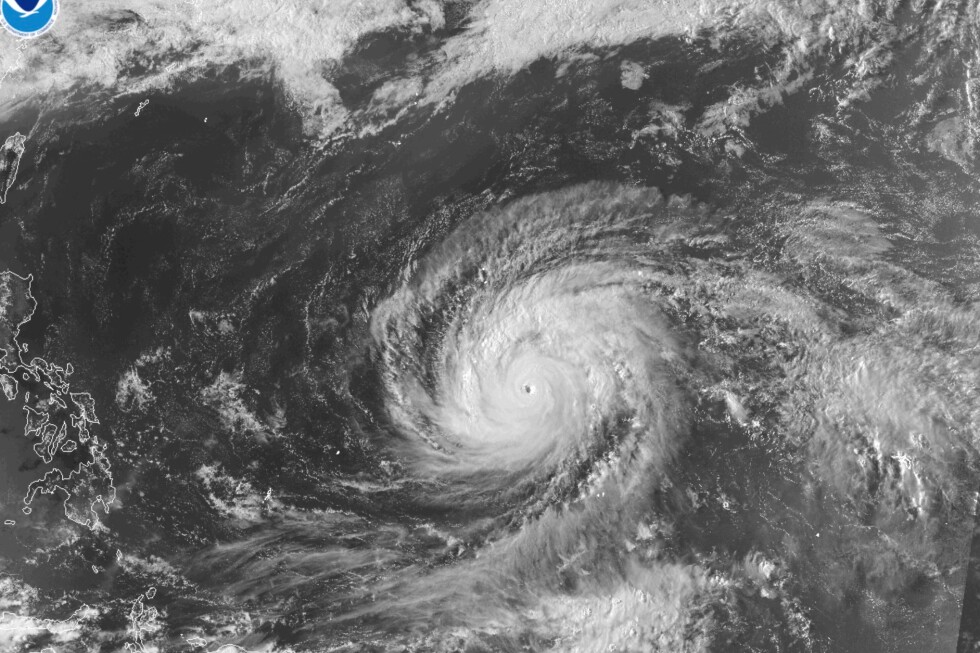

Typhoon Sinlaku’s Direct Path and Infrastructure Risk

Super Typhoon Sinlaku, currently the most powerful storm globally this year, is on a direct collision course with the remote U.S. islands in the Northern Mariana archipelago. Forecasts indicate that Sinlaku is expected to make landfall on Tuesday, bringing with it destructive winds, widespread heavy rainfall, and the potential for severe flooding. On Monday, the Joint Typhoon Warning Center reported sustained winds of an astonishing 173 mph (278 kph) as the typhoon neared the islands of Rota, Tinian, and Saipan. Although a slight weakening is anticipated over the coming days, Sinlaku is projected to cross near these islands as a formidable Category 4 or 5 typhoon.

Guam, a strategically vital U.S. territory hosting significant military installations, is also under a tropical storm warning, with damaging winds expected to commence Monday. The U.S. Coast Guard has already issued flood and high wind warnings. The memory of Typhoon Mawar in 2023, which caused extensive power outages for days in Guam, underscores the vulnerability of the region’s infrastructure to such powerful storms. President Donald Trump’s pre-emptive approval of emergency disaster declarations for both Guam and the Northern Mariana Islands highlights the gravity of the situation and the anticipated need for significant relief efforts. While these islands are not direct oil production or refining centers, the disruption to shipping, communication, and military operations in such a critical Pacific location can create ripple effects for broader logistics and supply chain confidence, a factor often underestimated in initial market reactions.

Market Response Amidst Broader Volatility

The specter of Super Typhoon Sinlaku emerges at a time when crude markets are already experiencing significant movement. As of today, Brent crude trades at $95.32, marking a robust 5.47% increase, with a daily range fluctuating between $92.77 and $97.81. Similarly, WTI crude has seen a substantial gain of 5.62% to $87.23, trading within a daily range of $85.45 to $89.6. Gasoline prices have also climbed, reaching $3.04, up 3.75%. This upward momentum today contrasts sharply with the recent 14-day trend for Brent, which saw prices decline by nearly 20%, from $112.78 on March 30th to $90.38 on April 17th.

While the immediate price surge today cannot be solely attributed to Sinlaku, the typhoon adds a layer of supply chain uncertainty to an already taut market. Any disruption, even localized, can contribute to bullish sentiment, especially when overall inventory levels remain a concern. Investors are keenly aware that major weather events, particularly in key shipping lanes or strategic regions, have the potential to impact vessel movements, insurance premiums, and overall freight costs, directly influencing the delivered price of crude and refined products. Today’s price action reflects a market sensitive to potential disruptions, regardless of their direct connection to a barrel of oil in the ground.

Investor Focus: Navigating Price Outlook Beyond Weather Events

Our proprietary reader intent data reveals a consistent theme among investors this week: a burning desire for clarity on future oil prices. Questions like “is wti going up or down” and “what do you predict the price of oil per barrel will be by end of 2026?” dominate inquiries. This underscores that while immediate events like Sinlaku create short-term ripples, the overarching concern for investors remains the medium to long-term price trajectory, driven by fundamental supply and demand dynamics, rather than isolated weather phenomena.

While a super typhoon can certainly cause immediate, albeit localized, disruptions, its sustained impact on global crude prices is typically dwarfed by broader macroeconomic trends, geopolitical developments, and the decisions of major oil producers. Therefore, investors must look beyond the transient headlines of weather events and focus on the fundamental catalysts that will truly shape the market’s direction. The recent volatility, with Brent shedding nearly $22 in just over two weeks before today’s rebound, illustrates the market’s sensitivity to a confluence of factors, making a holistic view indispensable for informed investment decisions.

Upcoming Catalysts Shaping the Energy Landscape

Looking ahead, the next two weeks are packed with critical energy events that will undoubtedly exert more enduring influence on crude prices than even the most powerful Pacific typhoon. The OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting on Monday, April 20th, and the subsequent full OPEC+ Ministerial Meeting on Saturday, April 25th, are paramount. These gatherings will provide crucial insights into the cartel’s production policy, which remains a primary determinant of global crude supply. Any indication of further cuts or an unexpected increase in output will send significant signals through the market, potentially overriding other concerns.

Furthermore, weekly inventory data will continue to be a key indicator for demand health and supply-demand balances. The API Weekly Crude Inventory reports on Tuesday, April 21st, and Tuesday, April 28th, followed by the official EIA Weekly Petroleum Status Reports on Wednesday, April 22nd, and Wednesday, April 29th, will offer granular detail on U.S. crude, gasoline, and distillate stockpiles. These reports are often immediate price movers, reflecting the current state of consumption and production. Finally, the Baker Hughes Rig Count on Friday, April 24th, and Friday, May 1st, will provide an essential gauge of future drilling activity and potential U.S. supply growth. These regularly scheduled events, rather than the unpredictable path of a typhoon, will be the true drivers determining whether WTI and Brent trend up or down in the coming months.