The intricate dance of global geopolitics often casts long shadows over seemingly unrelated sectors, and the energy market is no exception. While daily oil price movements are frequently dictated by immediate supply-demand dynamics, underlying diplomatic tensions and shifts in international relations can profoundly influence investor sentiment and long-term capital flows. A prime example emerged in May 2025, when a high-stakes meeting between the US President and South African President Cyril Ramaphosa, ostensibly focused on trade, exposed deep political fissures. For energy investors, understanding how such diplomatic friction, even when not directly about oil and gas, can impact broader investment climates, particularly in critical emerging markets like Africa, is crucial for strategic positioning.

Geopolitical Crosscurrents and African Investment Perception

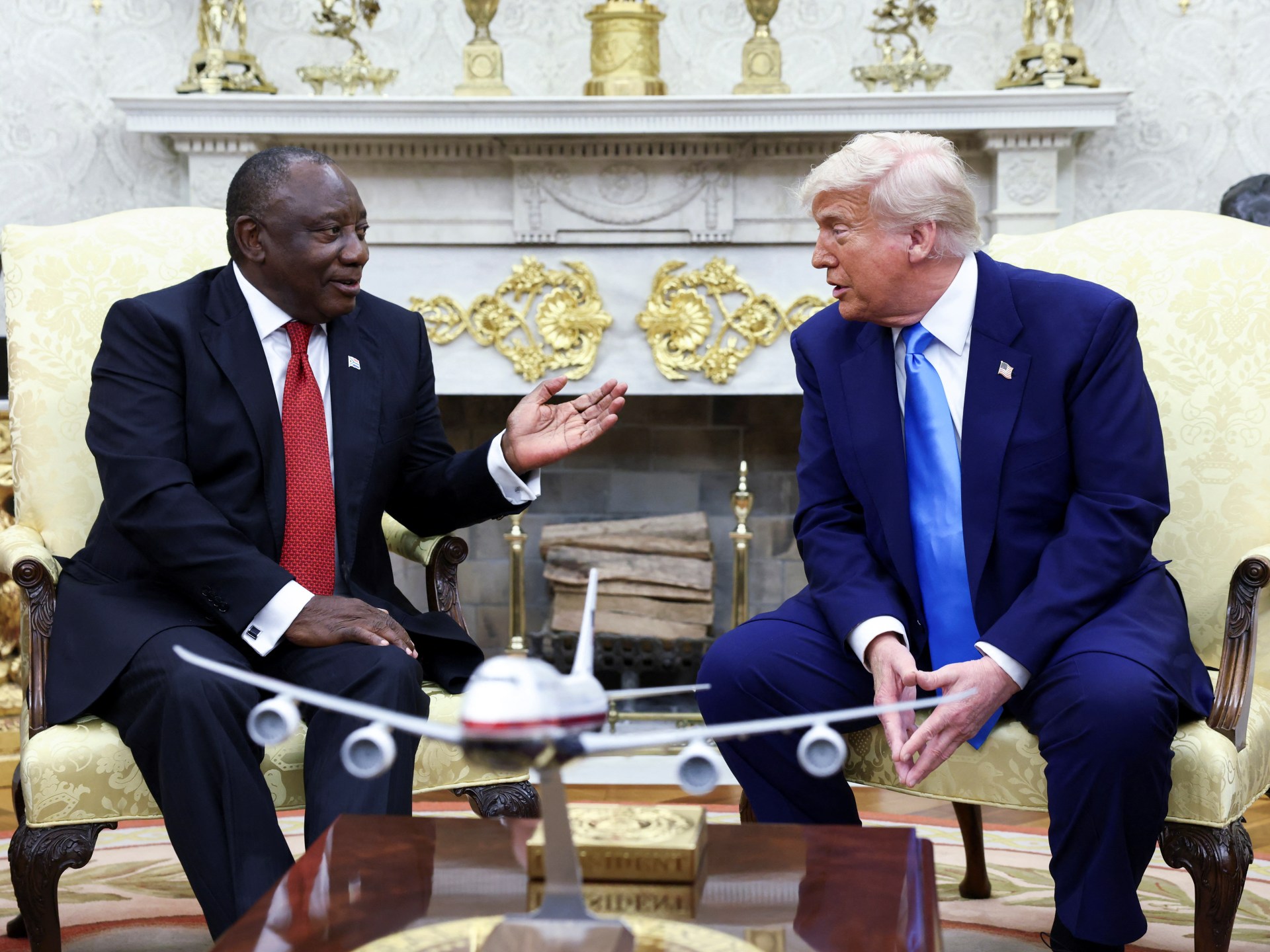

The May 21, 2025, encounter between the US President and South Africa’s Cyril Ramaphosa was a diplomatic tightrope walk. President Ramaphosa arrived in Washington with a clear mandate: to bolster trade and investment ties, emphasizing a history of cooperation. However, the meeting took an unexpected turn as the US President redirected the conversation, presenting printouts and a video to highlight allegations of “white genocide” in South Africa. This move, described by South African media as an “ambush,” forced Ramaphosa and his delegation to defend the nation’s integrity against assertions that white farmers were being specifically targeted.

Ramaphosa, supported by his diverse delegation which included prominent figures like agriculture minister John Steenhuisen and businessman Johann Rupert, firmly countered these claims, asserting that while criminality was a serious national issue, it affected all South Africans regardless of race. Steenhuisen further clarified that the majority of commercial and smallholder farmers in South Africa intended to remain and contribute to the country’s economic fabric. For energy investors, this diplomatic episode, while not directly involving energy policy, is a critical signal. Such high-profile political disputes, regardless of their ultimate resolution, inject a layer of perceived political risk into the investment landscape. South Africa, a significant African economy, serves as a gateway for broader continental investment. A cloud of uncertainty over its stability and governance can deter foreign direct investment across various sectors, including the crucial infrastructure and energy projects that underpin long-term demand growth in the region.

Market Realities Amidst Geopolitical Nuance

Against this backdrop of evolving geopolitical dynamics, global energy markets continue to react to immediate supply and demand fundamentals. As of today, April 15, 2026, Brent crude trades at $96.04 per barrel, reflecting a 1.32% gain on the day, with its US counterpart, WTI crude, similarly buoyant at $92.40, up 1.23%. Gasoline prices also show a modest uptick, standing at $2.98 per gallon. This current upward momentum, however, follows a notable correction over the past two weeks, where Brent shed approximately $9 per barrel, moving from $102.22 on March 25th to $93.22 by April 14th.

While these daily and short-term price movements are heavily influenced by inventory data, production quotas, and immediate demand indicators, the underlying geopolitical climate plays a more subtle, yet profound, role in shaping investor sentiment and risk premiums. The friction between a major global power and a key African economy, as witnessed in the SA-US meeting, contributes to a broader perception of risk in emerging markets. For energy investors, this means carefully calibrating the potential for sustained economic growth and stability in regions vital for future energy demand. If diplomatic tensions translate into reduced FDI or slower economic development in countries like South Africa, it could eventually temper long-term demand growth projections, even if current market prices are driven by other factors. The market’s resilience in the face of various geopolitical headwinds underscores the robust underlying demand, but investors must remain cognizant of how these broader risk factors can influence future trajectories.

Navigating Forward: Upcoming Catalysts and African Energy Prospects

Looking ahead, the next two weeks present several critical data points and decisions that will significantly influence global energy markets, and by extension, the investment climate for African energy. Key among these are the Baker Hughes Rig Count reports scheduled for April 17th and April 24th, providing vital insights into North American production activity. More importantly for global supply, the OPEC+ Joint Ministerial Monitoring Committee (JMMC) meets on April 18th, followed by the full OPEC+ Ministerial Meeting on April 20th.

Decisions emanating from these OPEC+ gatherings regarding production levels will be paramount for price stability and supply management. Simultaneously, the API Weekly Crude Inventory (April 21st, April 28th) and the EIA Weekly Petroleum Status Report (April 22nd, April 29th) will offer crucial snapshots of US supply and demand dynamics. While South Africa is not an OPEC+ member, the outcomes of these meetings directly impact the global oil price environment, which in turn affects the economic viability of new projects and the fiscal health of major African oil-producing nations. The lingering uncertainty from diplomatic spats, such as the SA-US friction, further complicates long-term investment calculations for companies eyeing African exploration, infrastructure development, or renewable energy projects. These broader geopolitical factors create a risk overlay that investors must integrate into their forward-looking models, even as they anticipate the immediate impact of these upcoming market-specific events.

Addressing Investor Concerns: Risk, Return, and African Exposure

Our proprietary analytics reveal a keen investor interest this week in fundamental Brent price forecasts for the next quarter, alongside broader questions about global demand drivers, including the operational status of Chinese ‘tea-pot’ refineries and Asian LNG spot prices. These questions highlight a desire for clarity amidst a complex array of market signals. The diplomatic friction witnessed in the SA-US meeting, while not directly tied to oil production, significantly impacts the perception of risk and return for investments across the African continent, a region critical for long-term global energy demand growth.

Investors are seeking to understand how perceived political instability or uncertainty in major economies like South Africa could influence overall foreign direct investment into Africa. A slowdown in industrialization or infrastructure development due to heightened risk perception would inevitably temper future energy demand growth across the continent. Moreover, for those considering the consensus 2026 Brent forecast, geopolitical stability in emerging markets is a non-trivial input. While the immediate focus might be on OPEC+ quotas or inventory draws, the underlying health and predictability of the political and economic environment in key demand centers are crucial for sustaining long-term investment. The SA-US dynamic underscores the need for thorough due diligence and a nuanced understanding of political risk when allocating capital to African energy assets, whether in upstream exploration, downstream refining, or the burgeoning renewables sector. Investors are balancing the attractive growth potential of emerging markets with the inherent volatility and policy uncertainties that can arise from such high-level diplomatic tensions.