The Evolving Landscape of Climate Risk Quantification for Energy Investors

The financial world is rapidly recalibrating its approach to climate change, moving beyond mere disclosure to sophisticated quantification of physical risks. For investors in the oil and gas sector, this evolution is particularly salient, given the industry’s extensive physical infrastructure and long-term asset lifecycles. New analytical solutions are emerging, designed to empower banks and asset managers to embed climate risk directly into portfolio analysis and capital allocation. This paradigm shift means evaluating not just the likelihood of climate events, but their precise financial impact and the measurable return on investment (ROI) for resilience strategies.

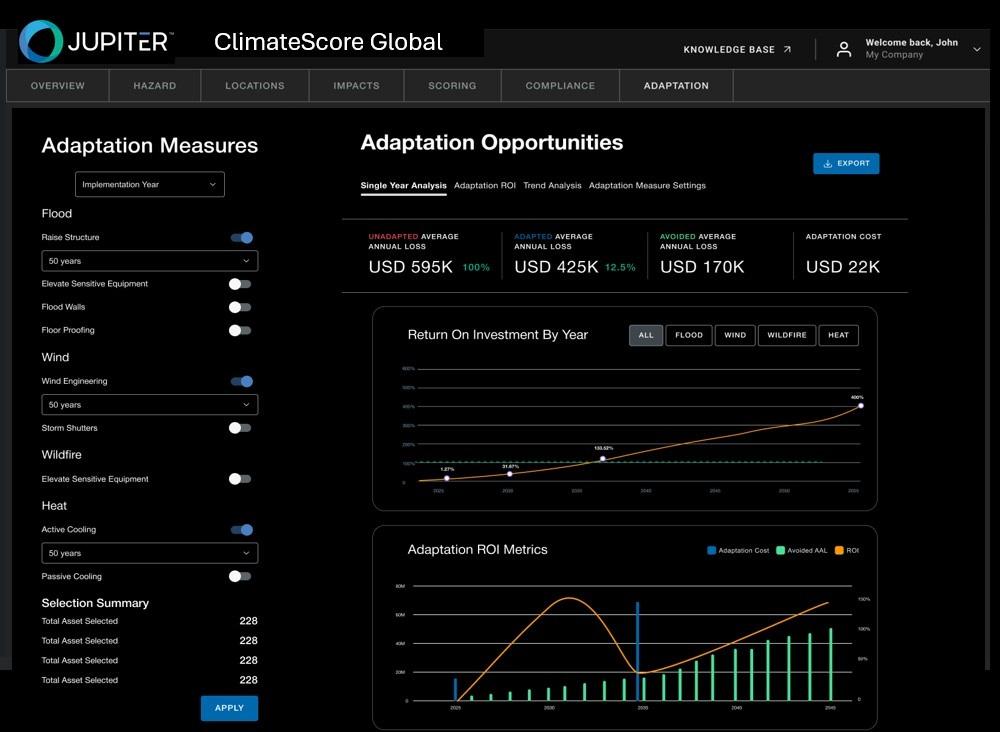

These cutting-edge tools offer capabilities such as an “Adaptation Hub,” enabling the quantification of avoided losses and the calculation of ROI across various adaptation strategies. This is critical for oil and gas firms assessing investments in hardening coastal refineries against storm surge, reinforcing pipelines in permafrost regions, or upgrading infrastructure to withstand extreme heat. Additionally, “Entity Modeling” provides granular climate risk insights across diverse investment vehicles, from individual securities to entire corporate portfolios, allowing investors to understand how specific assets within their energy holdings are exposed. Further innovations include “MetricEngine,” which arms quant teams with scenario-specific model outputs like custom return periods and loss distributions, and the “Subsidence Peril Metric,” which models structural risks from soil-moisture fluctuations, particularly relevant for onshore facilities built on clay-rich soils. These advancements transform climate risk from a qualitative concern into a quantifiable financial metric, demanding attention from any serious energy investor.

Market Realities: Integrating Climate Risk Amidst Crude Price Volatility

While the long-term imperative of climate risk assessment gains traction, investors in the oil and gas sector must continuously navigate immediate market dynamics. As of today, Brent Crude trades at $94.85, showing a negligible decrease of 0.08% within a day range of $94.42-$94.91. WTI Crude follows a similar trajectory at $91.19, down 0.11% within its daily range of $90.52-$91.5. This current stability, however, comes after a significant 12.4% drop over the past 14 days, with Brent falling from $108.01 on March 26th to $94.58 on April 15th. Such volatility underscores the multifaceted pressures on crude prices, driven by geopolitical shifts, demand signals, and supply adjustments.

In this environment, where short-term price swings can dominate headlines, the integration of sophisticated climate risk quantification tools becomes even more crucial for long-term investors. While traders focus on daily price movements and inventory reports, asset managers must look beyond. How resilient are an energy company’s assets to future climate impacts at $90 oil versus $100 oil? The “Subsidence Peril Metric,” for instance, directly addresses structural integrity risks that could impact operational continuity, regardless of the prevailing crude price. These new tools provide a framework for assessing physical asset exposure and the financial implications of climate change, offering a necessary counterpoint to the often-fickle immediate market sentiment and ensuring a more holistic understanding of asset value.

Proactive Strategies: Climate Resilience and Forward Price Forecasts

Our proprietary reader intent data reveals a consistent investor focus on future price trajectories, with many actively seeking to “build a base-case Brent price forecast for next quarter” and understand the “consensus 2026 Brent forecast.” These forecasts are traditionally built upon supply-demand fundamentals, geopolitical stability, and economic growth projections. However, the emergence of robust climate risk quantification introduces a critical new layer to this analysis. For oil and gas assets, particularly long-lived infrastructure like pipelines, refineries, and offshore platforms, understanding their physical vulnerability to climate events directly impacts their long-term operational viability and, by extension, their underlying value in any future price scenario.

Consider the implications of the “Adaptation Hub”: by quantifying avoided losses and calculating the ROI on resilience investments, investors can now directly factor these into their valuation models. A company that invests proactively in climate adaptation for its assets might command a premium, or at least mitigate downside risk, compared to a competitor with similar production capacity but higher climate exposure. This means that a truly comprehensive base-case Brent forecast for the next quarter or for 2026 must implicitly or explicitly account for the potential for climate-induced disruptions to supply chains, operational uptime, and even regional demand. These new tools provide the precision and defensibility investment committees, regulators, and boards now require, moving climate risk from a qualitative ESG checkbox to a quantifiable input in financial modeling.

Navigating Upcoming Events: Climate Risk in the Supply-Side Narrative

The coming weeks present several pivotal events for the energy market, which, while focused on immediate supply and inventory, also carry long-term implications for climate resilience. The Baker Hughes Rig Count reports on April 17th and April 24th will provide fresh insights into upstream activity. Crucially, the OPEC+ JMMC meeting on April 18th, followed by the Full Ministerial Meeting on April 20th, will set the tone for global crude supply in the near term. Additionally, the API Weekly Crude Inventory reports on April 21st and 28th, along with the EIA Weekly Petroleum Status Reports on April 22nd and 29th, will offer granular views on U.S. supply-demand balances.

While these events primarily dictate short-term market movements, the underlying physical risks quantified by new climate tools are deeply intertwined with the long-term stability and resilience of the global energy supply. For instance, decisions made by OPEC+ impact the investment landscape for future production, but the ultimate deliverability of that production hinges on the resilience of infrastructure against escalating climate threats. If a major producing region becomes increasingly susceptible to extreme weather events — a risk that “Entity Modeling” can quantify for specific companies operating there — then even favorable OPEC+ decisions or high rig counts might face physical limitations. Investors are increasingly evaluating how climate change might disrupt supply chains, impact operational integrity, and influence capital expenditure decisions for new projects, making these climate risk tools an indispensable part of comprehensive energy investment analysis, even amidst the immediate concerns of crude inventories and cartel policies.