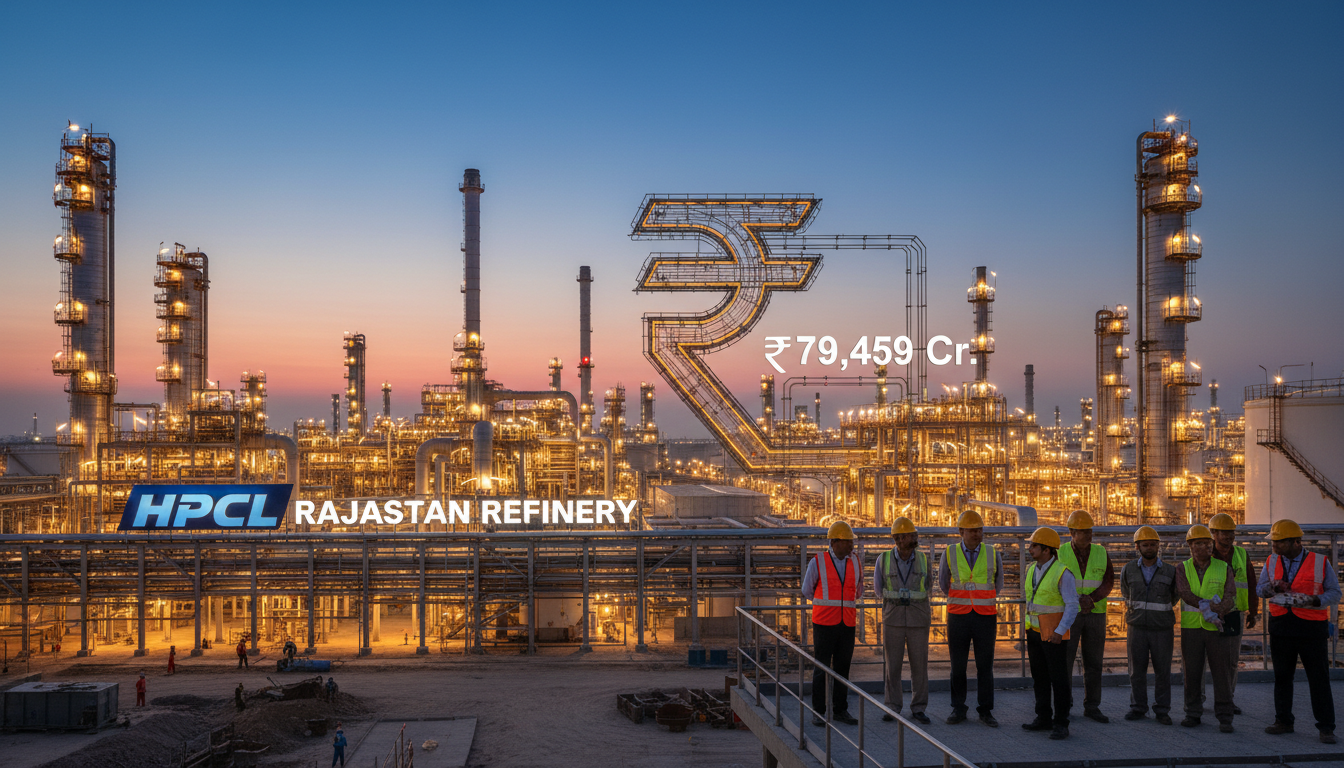

India’s energy sector is witnessing a monumental push towards self-reliance and expanded capacity, a strategic imperative underscored by the recent cabinet approval of a revised project cost for the HPCL Rajasthan Refinery Limited (HRRL) project. This significant development, now valued at an colossal ₹79,459 crore, represents a substantial increase from its initial ₹43,129 crore estimate. For investors tracking the subcontinent’s burgeoning energy landscape, this move by the Cabinet Committee on Economic Affairs, coupled with Hindustan Petroleum Corporation Limited’s (HPCL) increased equity commitment of ₹8,962 crore—bringing its total stake to ₹19,600 crore—signals a reinforced dedication to the ambitious 9 million metric tonnes per annum (MMTPA) greenfield refinery-cum-petrochemical complex. This project is not merely an infrastructure build-out; it is a critical pillar in India’s long-term energy security strategy and its aspiration to become a global refining and petrochemical powerhouse.

The Escalating Bill and HPCL’s Deepened Commitment

The nearly 84% surge in the HRRL project’s cost, from ₹43,129 crore to ₹79,459 crore, demands close scrutiny from HPCL shareholders and prospective investors. This substantial revision, with HPCL’s total equity investment now reaching ₹19,600 crore in the joint venture with the Government of Rajasthan (74% HPCL, 26% Rajasthan Government), highlights the increasing capital intensity of large-scale, complex energy projects. Such cost escalations, while common in megaprojects, naturally raise questions regarding the impact on HPCL’s future balance sheet, debt leverage, and the timeline for achieving attractive returns on invested capital. Our proprietary reader intent data shows investors are keenly focused on the financial implications of such large CAPEX initiatives, often asking about their potential impact on company valuations and dividend policies. While the project promises long-term strategic advantages, the upfront financial commitment is considerable, necessitating careful monitoring of project execution and market conditions leading up to its scheduled commercial operations in July 2026.

Strategic Imperatives: Fueling India’s Energy Independence

Beyond the raw numbers, the HRRL project embodies India’s strategic vision for energy self-sufficiency and industrial growth. This greenfield refinery-cum-petrochemical complex in Rajasthan’s Balotra district is not just about refining crude; it’s designed as a high-complexity facility with over 26% petrochemical integration. This integration is crucial, enabling the production of high-value petrochemicals alongside traditional fuels. The refinery is projected to produce approximately 1 MMTPA of petrol and 4 MMTPA of diesel, meeting critical transportation demands. Crucially, the project is designed to utilize locally available Mangala crude, enhancing domestic supply chain resilience and reducing reliance on imported feedstocks. This dual focus on refining and petrochemicals positions HRRL as a cornerstone of India’s drive to reduce import dependence across vital industrial sectors, aligning with broader governmental objectives for energy security and industrial development within the region.

The Petrochemical Power Play Amidst Evolving Market Dynamics

The HRRL project’s significant petrochemical production capacity of 2.4 MMTPA is a key differentiator, focusing on products vital for modern economies. This includes 1 MMTPA of polypropylene, 0.5 MMTPA of linear low-density polyethylene (LLDPE), 0.5 MMTPA of high-density polyethylene (HDPE), and around 0.4 MMTPA of benzene, toluene, and butadiene. These products are indispensable across sectors ranging from packaging and textiles to pharmaceuticals and paints, positioning India to significantly reduce its reliance on petrochemical imports. Our proprietary market data indicates that while Brent crude currently trades at $93.85, showing a modest daily gain of 0.65%, and WTI crude at $89.99, up 0.36%, the broader market has seen a notable shift. Over the past two weeks, Brent has trended downward by 7%, falling from $101.16 to $94.09. This price trajectory, which some investors are closely watching and asking about, directly influences refining margins and the profitability of crude processing operations. However, the high degree of petrochemical integration in the HRRL project provides a strategic hedge, allowing the facility to capture value from a diversified product slate, potentially mitigating some of the volatility inherent in pure fuel refining. As investors contemplate the future price of oil by the end of 2026, projects like HRRL underscore the long-term demand for refined products and petrochemicals, irrespective of short-term crude price fluctuations.

Forward Catalysts and Risks on the Horizon

With commercial operations slated to commence on July 1, 2026, the HRRL project’s timeline creates several forward-looking catalysts and potential risks for investors. Leading up to this crucial date, market participants will be closely monitoring macroeconomic indicators and sector-specific reports. Upcoming energy events, such as the EIA Weekly Petroleum Status Reports (scheduled for April 24th, April 29th, and May 6th) and the Baker Hughes Rig Counts (on April 26th and May 1st), will provide critical insights into supply-demand dynamics and refining utilization rates in the broader market. Furthermore, the EIA Short-Term Energy Outlook on May 2nd will offer updated forecasts on crude prices and product demand, influencing the revenue potential for HRRL upon its commissioning. Any further delays in project completion or significant shifts in global petrochemical demand could impact initial profitability projections. However, the project’s alignment with India’s long-term growth trajectory, its role in generating substantial employment during construction (approximately 25,000 workers), and its strategic importance in establishing India as a refining and petrochemical hub, present a compelling investment thesis for those with a long-term outlook on the subcontinent’s energy future.