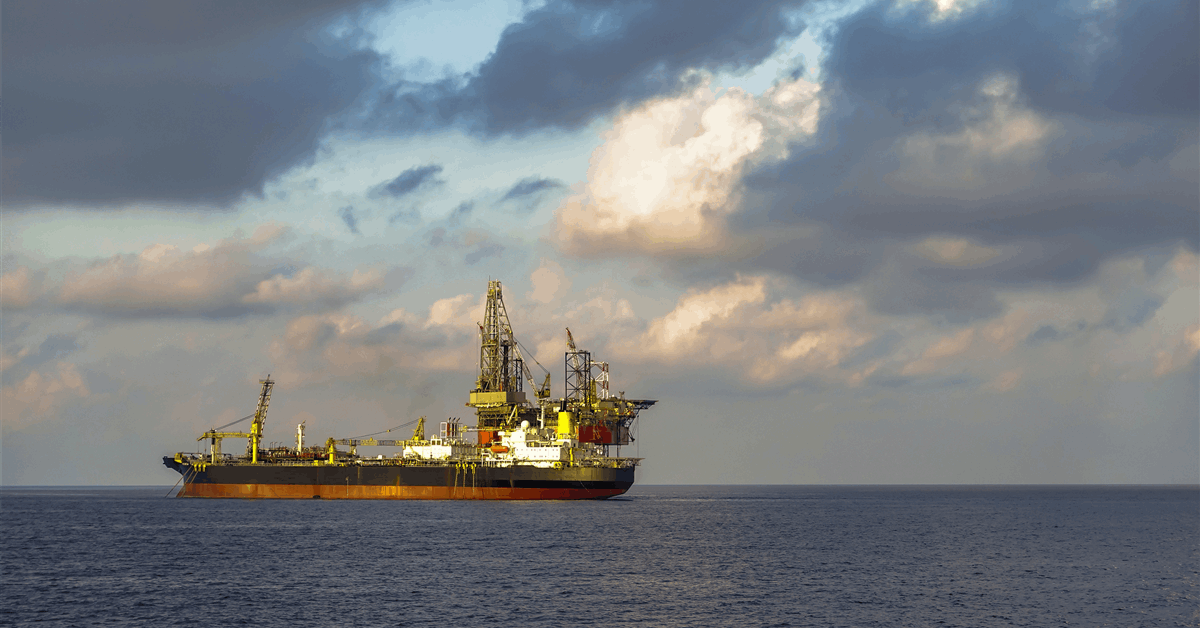

Barossa FPSO Commissioning: Output Imminent

The arrival and ongoing commissioning of the BW Opal floating production, storage, and offloading (FPSO) vessel at Australia’s Barossa gas field marks a pivotal moment for Santos Ltd. and its joint venture partners. This critical milestone sets the stage for first gas from the Barossa liquefied natural gas (LNG) project in the third quarter of 2025, a timeline that underscores robust project execution and positions Barossa as a significant contributor to the global LNG supply landscape. For investors, this development signals the imminent realization of a major growth catalyst, promising substantial long-term cash flows in a market hungry for reliable energy supplies.

Barossa’s Imminent Output: A De-Risked Growth Story

The Barossa LNG project, with its production centerpiece now on site and hooked up, is progressing firmly towards its Q3 2025 first gas target. Santos, alongside partners SK E&S and JERA Co. Inc., has invested a substantial $3.95 billion (AUD6.07 billion at current rates) to date, a figure that remains within original cost guidance despite the complexities of a project initiated with regulatory acceptance back in 2018. This “on-time, on-budget” achievement is a testament to strong project management and de-risks the investment thesis considerably. Santos’s Managing Director and CEO, Kevin Gallagher, has highlighted Barossa as a world-class asset, projecting a 30 percent increase in company-wide production over the next eighteen months when combined with the Pikka phase one project in Alaska. This anticipated ramp-up is crucial for delivering stable cash flows and underpinning compelling shareholder returns moving forward.

Strategic Production Boost Amidst Dynamic Energy Markets

The projected 30% increase in Santos’s production profile, driven by Barossa and Pikka, comes at a strategic time for global energy markets. As of today, Brent Crude trades at $94.94, exhibiting a slight daily uptick of 0.16% within a $91-$96.89 range. However, this follows a notable 14-day downtrend, seeing prices fall approximately $9, or 8.8%, from $102.22 on March 25 to $93.22 on April 14. This broader commodity price volatility underscores the value of long-term, contracted LNG projects like Barossa, which often secure pricing structures less susceptible to immediate oil price fluctuations. Our proprietary reader intent data reveals a keen investor focus on understanding the underlying dynamics, with frequent queries such as “What’s driving Asian LNG spot prices this week?” and “How are Chinese tea-pot refineries running this quarter?” These questions directly highlight the demand-side considerations, particularly from Asian markets, that Barossa is poised to capitalize on, providing a crucial supply source to a region with robust and growing energy needs.

Darwin LNG: A Critical Enabler and Economic Catalyst

Beyond the Barossa FPSO itself, the Darwin LNG life extension (DLE) project plays an indispensable role in the overall success of the Barossa development. With 90 percent of the work now complete, the DLE project is also on track for completion by the start of Q3 2025, perfectly aligning with Barossa’s first gas timeline. This associated infrastructure represents an additional AUD1 billion investment and has already generated significant local economic benefits. The DLE project has created 300 construction and maintenance jobs in Darwin, and ongoing operations are expected to generate approximately AUD100 million per year in supply and service opportunities for Northern Territory businesses. Furthermore, the Darwin LNG joint venture’s AUD3 million initiative with KAEFER Integrated Services to develop a skilled Aboriginal workforce, providing 20 trade and traineeship opportunities, underscores a commitment to sustainable local engagement and long-term community benefits, a factor increasingly valued by ESG-conscious investors.

Navigating the Macro Environment: What’s Ahead for Energy Investors?

As Barossa moves closer to production, investors are naturally scrutinizing the broader energy market for signals impacting future commodity prices and investment sentiment. Our proprietary data indicates that inquiries regarding long-term price outlooks, such as “Build a base-case Brent price forecast for next quarter” and “What is the consensus 2026 Brent forecast?”, are prominent among our readership. These forward-looking analyses will be heavily influenced by upcoming calendar events. The next 14 days include critical OPEC+ meetings, with the Joint Ministerial Monitoring Committee (JMMC) scheduled for April 18 and the Full Ministerial Meeting on April 20. Outcomes from these discussions will be pivotal in shaping market expectations regarding crude supply and, by extension, the broader energy complex. Additionally, the recurring API Weekly Crude Inventory (April 21, April 28) and EIA Weekly Petroleum Status Reports (April 22, April 29) will provide ongoing insights into global supply-demand balances. While Barossa is an LNG project, a stable and predictable oil market environment, influenced by these key events, generally fosters a more favorable climate for long-term capital allocation across the entire energy sector, reinforcing the attractiveness of Santos’s de-risked growth trajectory.