The global energy landscape is undergoing a profound transformation, with increasing emphasis on decarbonization and energy security. While oil and gas continue to dominate, a significant shift is emerging in the baseload power generation sector. The revival of nuclear power, particularly through advanced small modular reactors (SMRs), represents a potent force set to reshape long-term energy investment strategies. This shift is not merely theoretical; it is actively unfolding in places like Covert Township, Michigan, where the decommissioning of an aging plant has given way to a multi-billion dollar recommissioning and the ambitious development of next-generation nuclear technology, signaling a broader market re-evaluation.

The Dawn of a Nuclear Renaissance: SMRs and Legacy Plant Revival

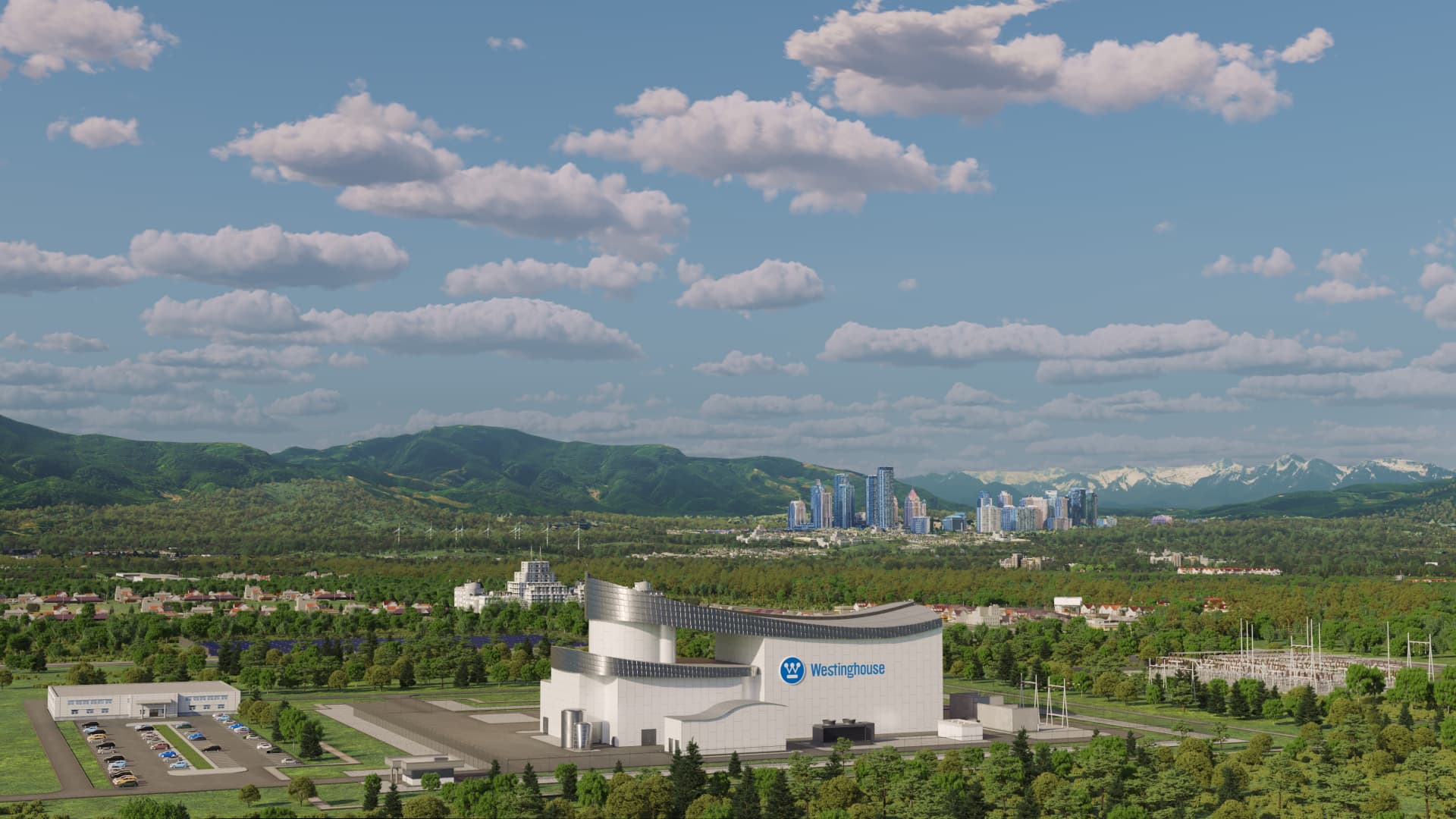

In a compelling testament to nuclear’s renewed appeal, the Palisades Nuclear Plant, operational since 1971, is making an unprecedented return to service. Decommissioned in 2022, this 800-megawatt facility in Van Buren County, Michigan, is being reactivated through an over $1 billion loan secured under the Biden administration’s Inflation Reduction Act, with the initial federal installment already provided this year. This significant investment underscores a strategic push to bolster reliable, carbon-free power generation. Beyond the recommissioning, the site is slated to become a cornerstone of America’s nuclear future, with Holtec Corporation constructing two SMR-300 units planned to be operational by the early 2030s. These SMRs, characterized by their factory-built design, smaller footprint (typically 300 megawatts or less), and potential for mass production and faster installation, represent a pivotal evolution in nuclear technology. This dual approach of reactivating a proven asset while pioneering new modular designs highlights a pragmatic and forward-looking energy strategy. The economic impact is substantial, promising 600 jobs for the legacy plant and an additional 300 for the SMRs, with salaries averaging $107,000, injecting year-round stability into a region traditionally reliant on seasonal tourism. This local embrace, fueled by existing nuclear expertise and a positive safety record, paves the way for broader national acceptance and deployment.

Navigating Volatility: Nuclear Stability Amidst Oil Market Swings

The strategic re-embrace of nuclear power arrives at a time when traditional energy markets continue to demonstrate significant volatility, reinforcing the appeal of stable, baseload alternatives. As of today, Brent Crude trades at $90.38 per barrel, marking a sharp -9.07% decline within a day range of $86.08 to $98.97. Similarly, WTI Crude stands at $82.59, down -9.41% on the day, traversing a range from $78.97 to $90.34. Gasoline prices have also seen a notable drop, currently at $2.93, a -5.18% decrease with a day range of $2.82 to $3.1. This immediate market snapshot is not an isolated incident; the 14-day Brent trend reveals a significant downturn, falling from $112.78 on March 30, 2026, to its current $90.38 – a substantial $22.4 or -19.9% reduction. Such pronounced swings in hydrocarbon prices underscore the inherent market risks for investors and the broader economy. In contrast, nuclear power offers a predictable and consistent energy source, largely insulated from geopolitical tensions and commodity price fluctuations once plants are operational. This stark contrast in market behavior makes the long-term investment into nuclear infrastructure, supported by initiatives like the Inflation Reduction Act, increasingly attractive for nations seeking energy independence and price stability, thereby subtly chipping away at the long-term demand growth for fossil fuels in power generation.

Investor Horizon: Connecting Near-Term Oil Dynamics to Long-Term Nuclear Shifts

Investors are keenly observing the interplay between immediate market forces and long-term energy transitions. A frequent question from our readers concerns the future trajectory of oil prices, with many asking, “what do you predict the price of oil per barrel will be by end of 2026?” and “What are OPEC+ current production quotas?” These questions highlight a focus on the immediate supply-demand fundamentals that dictate hydrocarbon profitability. To that end, the upcoming OPEC+ Ministerial Meeting on April 19th will be critical, as any decisions on production quotas will directly influence global oil supply and, consequently, prices. Furthermore, the API Weekly Crude Inventory reports on April 21st and 28th, alongside the EIA Weekly Petroleum Status Reports on April 22nd and 29th, will provide crucial near-term insights into U.S. supply levels and demand indicators. The Baker Hughes Rig Count on April 24th and May 1st will offer an early glimpse into future domestic production capacity. While these events drive short-term trading strategies in oil and gas, they exist in parallel with the foundational shifts brought about by nuclear investments. The development of SMRs, though operational in the early 2030s, represents a strategic hedge against future fossil fuel price volatility and carbon regulations. For investors, understanding the near-term volatility of crude, driven by OPEC+ actions and inventory data, alongside the steady, long-term build-out of nuclear baseload capacity, is crucial for crafting a resilient energy portfolio that accounts for both immediate returns and future market reconfigurations.

The Evolving Energy Investment Thesis

The re-emergence of nuclear power, particularly through the lens of SMR development and the recommissioning of existing assets, necessitates a re-evaluation of the long-term energy investment thesis. Government incentives, exemplified by the substantial loan for the Palisades plant, are catalyzing this sector, making it a compelling area for capital deployment. Companies involved in advanced nuclear technologies, engineering, and construction are poised for significant growth. While the capital intensity and regulatory complexities of nuclear projects remain high, the long-term stability of output, minimal operational emissions, and enhanced energy security offer a powerful counter-narrative to the intermittency of renewables and the price volatility of fossil fuels. For traditional oil and gas investors, this signifies a gradual but inevitable shift in baseload power demand away from hydrocarbons. Smart investors are already considering how this nuclear revival impacts long-term oil and gas demand projections, particularly for power generation, and exploring diversification into companies involved in the nuclear supply chain, from uranium mining to reactor technology development and waste management. The narrative is no longer solely about oil and gas production growth; it is increasingly about securing diverse, stable, and clean energy sources, with nuclear power emerging as a critical component of that future investment landscape.