Germany has taken a significant step in fortifying its energy independence with the commercial launch of Deutsche Energy Terminal GmbH’s (DET) second liquefied natural gas (LNG) terminal in Wilhelmshaven. This new facility, Wilhelmshaven 02, represents a crucial addition to Europe’s energy infrastructure, bolstering natural gas supply ahead of the upcoming heating season. For investors, this development signals ongoing strategic shifts in global energy flows and highlights the resilience and innovation within the sector, even as broader market dynamics present a complex picture for crude and refined products.

Germany’s Latest LNG Boost: A Strategic Move for European Energy Security

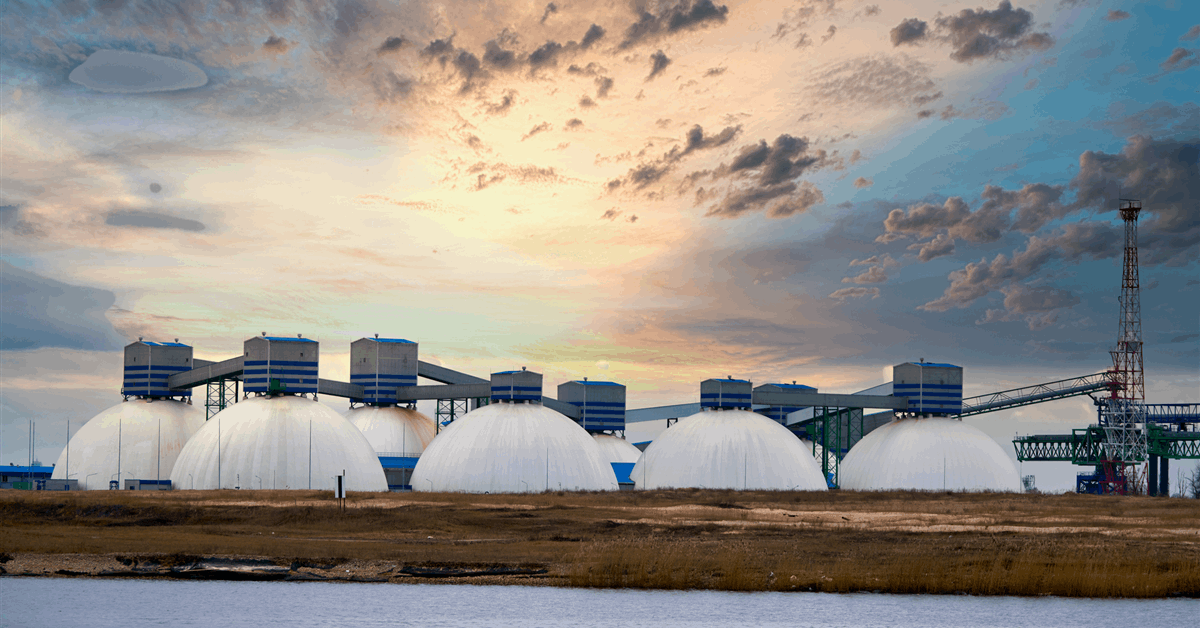

The Wilhelmshaven 02 terminal, featuring the floating storage and regasification unit (FSRU) Excelsior, is now fully operational, significantly enhancing Germany’s capacity to import and regasify LNG. The Excelsior, chartered by DET for five years, is a substantial asset, measuring 909 feet long with a storage capacity of 4.9 million cubic feet and a regasification throughput of up to 500 million standard cubic feet per day. This expansion directly addresses Germany’s need to diversify its energy sources, particularly in the wake of geopolitical shifts impacting traditional gas supplies.

The strategic importance of this terminal is underscored by its impressive capacity and market uptake. In 2025, the Excelsior is projected to feed up to 1.9 billion cubic meters of natural gas into the German grid, an amount sufficient to heat approximately 1.5 million four-person households. Looking further ahead, its regasification and grid feed-in capacity are expected to nearly double in the subsequent two years, reaching up to 4.6 billion cubic meters annually, capable of supplying 3.7 million four-person households. Crucially, DET has confirmed that the regasification capacity for the remainder of 2026 and all of 2026 has already been fully allocated to traders, indicating strong demand and the immediate utility of this new infrastructure. Investors should note the innovative technologies integrated into the Wilhelmshaven 02 project, such as ECOnnect’s flexible pipeline system, which minimizes environmental impact, and Europe’s first ultrasonic process for cleaning the FSRU’s seawater pipeline system, highlighting a commitment to efficiency and sustainability in energy infrastructure development. Onsite terminal operations are managed by Gasfin Services GmbH, with commercial management and technical operations led by the Lithuanian LNG company KN Energies, further solidifying the operational expertise behind this vital project.

Navigating Volatility: Crude and Product Markets React to Shifting Fundamentals

While Germany bolsters its natural gas security, the broader crude and refined product markets are experiencing significant volatility. As of today, Brent Crude trades at $90.38 per barrel, marking a substantial 9.07% decline within the day, having ranged between $86.08 and $98.97. Similarly, WTI Crude has seen a sharp drop, trading at $82.59 per barrel, down 9.41% from its daily high, fluctuating between $78.97 and $90.34. This pronounced downturn is also reflected in the gasoline market, where prices stand at $2.93 per gallon, a 5.18% decrease, moving within a daily range of $2.82 to $3.10.

This recent market action represents a notable shift from earlier trends. Over the past 14 days, Brent crude has seen a steady decline, falling from $112.78 on March 30th to $91.87 just yesterday, before today’s further depreciation. This $20.91, or 18.5%, reduction in Brent’s price highlights a period of intense selling pressure and re-evaluation of market fundamentals. Investors are keenly watching these price movements, questioning the factors driving such sharp daily corrections. Potential drivers could include evolving geopolitical sentiments, shifting demand forecasts, or even speculative positioning. The substantial daily price declines across crude and gasoline suggest a market grappling with new information or sentiment, underscoring the dynamic and often unpredictable nature of energy commodity trading.

Forward Gaze: Key Events Shaping the Energy Investment Landscape

For discerning investors, understanding the forward calendar is as crucial as analyzing current market data. The coming weeks are packed with events that could significantly influence crude oil and natural gas prices, demanding close attention to strategic positioning. This weekend, the focus will be squarely on the OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting on April 18th, followed by the full OPEC+ Ministerial Meeting on April 19th. These gatherings are pivotal, as any decisions regarding production quotas will directly impact global crude supply and, consequently, price stability. Investors are particularly interested in whether the alliance will maintain, adjust, or potentially increase current production levels given recent market volatility.

Beyond OPEC+, key weekly data releases will provide fresh insights into market balances. The API Weekly Crude Inventory report on April 21st and 28th, alongside the EIA Weekly Petroleum Status Report on April 22nd and 29th, will offer critical snapshots of U.S. crude, gasoline, and distillate stocks, directly impacting supply-demand perceptions. Furthermore, the Baker Hughes Rig Count, scheduled for April 24th and May 1st, will serve as an important indicator of future drilling activity and potential production trends in North America. Each of these events presents an opportunity for market re-pricing and offers investors actionable intelligence to refine their strategies in the dynamic oil and gas sector.

Investor Focus: Addressing Core Concerns in a Dynamic Market

Our proprietary reader intent data reveals a clear focus among investors on understanding future price trajectories and the underlying market mechanics. A recurring question this week, for example, is “what do you predict the price of oil per barrel will be by end of 2026?” This reflects a deep-seated desire for clarity amidst the current volatility, especially after today’s significant price drops. Predicting precise oil prices remains challenging, influenced by a confluence of geopolitical stability, global economic growth, and the ongoing energy transition. However, developments like Germany’s new LNG terminal, while impacting gas markets directly, also indirectly alleviate pressure on oil by enhancing overall energy security.

Another prominent query centers on “What are OPEC+ current production quotas?” This highlights the market’s reliance on the cartel’s decisions as a primary lever for supply management. The upcoming OPEC+ meetings are therefore under intense scrutiny for any signals regarding these quotas. For companies like Repsol, which some readers are asking about their performance in April 2026, their trajectory will depend not only on broader crude and natural gas prices but also on their diversified portfolios, including investments in renewables and LNG infrastructure. As the global energy landscape continues its rapid evolution, investors are prioritizing detailed analysis of supply-side developments, demand forecasts, and strategic corporate initiatives to navigate the complexities and identify compelling opportunities.