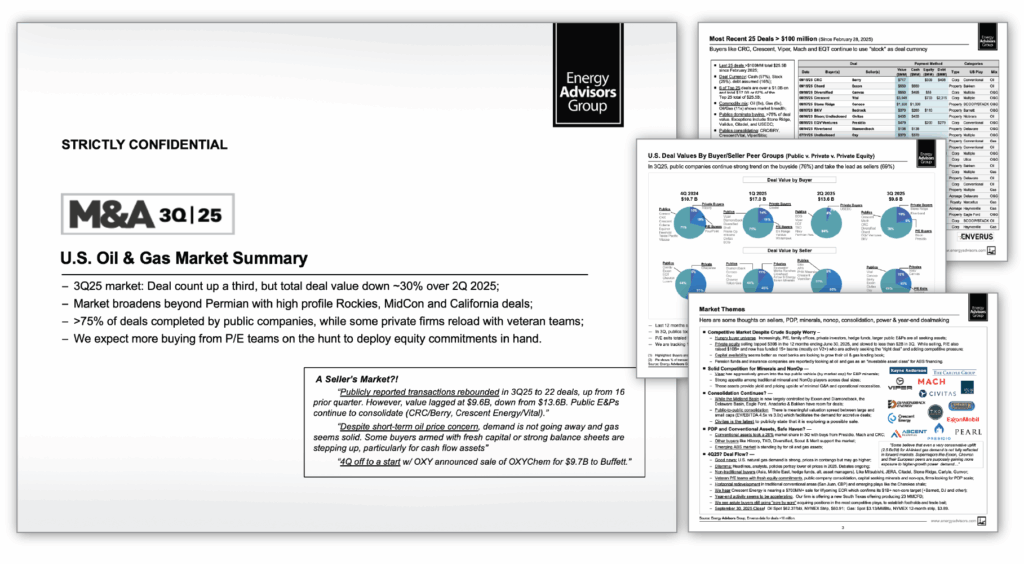

The third quarter of the past year presented a nuanced picture for oil and gas mergers and acquisitions, characterized by a notable increase in transaction volume but a significant contraction in total deal value. Our analysis, leveraging proprietary market intelligence and transaction data, reveals that while publicly reported deals exceeding $10 million rebounded to 22 in 3Q from 16 in the preceding quarter, their combined value plummeted by 30% to $9.6 billion, down from $13.6 billion. This divergence signals a more fragmented M&A landscape, driven by strategic consolidation among public E&Ps and a shifting focus towards assets offering more predictable cash flows, even as the broader energy market grapples with persistent volatility. Investors are keenly observing these trends, seeking clarity on where capital is being deployed and what it means for future returns.

The Evolving M&A Landscape: More Deals, Lower Aggregate Value

The data from 3Q underscores a clear trend: the market saw more participants engaging in M&A, yet the size of these individual transactions was, on average, smaller. While 22 deals surpassed the $10 million threshold, pushing deal count above the previous quarter’s 16, the aggregate value of $9.6 billion fell considerably short of the average quarterly value of $17.1 billion observed since 2020 (excluding the impact of three mega-mergers). This suggests a more active but less concentrated deal environment, reflecting a strategic response by companies to optimize portfolios and achieve incremental growth rather than pursuing transformative, multi-billion-dollar acquisitions. The increased volume in a lower-value environment indicates a market that is consolidating in pieces, with buyers targeting specific assets that align with their operational strengths and long-term strategic objectives.

Public E&Ps Drive Consolidation Amidst Heightened Market Volatility

Publicly traded exploration and production (E&P) companies continued to be the dominant force on the buyside in 3Q, accounting for more than 75% of total M&A activity. Firms like Crescent Energy, Mach Natural Resources, California Resources, Diversified, Chord, and BKV were active, demonstrating a clear appetite for expansion and efficiency. This aggressive posture from public entities stands in stark contrast to the noticeable cooling of private equity selling activity, which dropped to less than $2 billion in 3Q after divesting over $30 billion in the preceding 12 months. The drive for consolidation by public E&Ps can be directly linked to the prevailing market sentiment and the need for scale and cost synergies in a volatile pricing environment. As of today, April 19, 2026, Brent Crude is trading at $90.38, a significant -9.07% drop just today, and a stark -19.9% decline from $112.78 merely two weeks ago. This rapid price erosion, with WTI Crude also down to $82.59, underscores the persistent pricing uncertainty that continues to shape strategic decisions for E&P firms, driving them towards accretive, all-stock deals seen in 3Q to mitigate risk and enhance shareholder value.

The Lure of Predictable Cash Flow: Natural Gas and PDP Assets

A significant trend emerging from 3Q M&A data is the increasing momentum for natural gas and proved developed producing (PDP) assets, which collectively accounted for 26% of the total deal value. This strategic pivot reflects a broader shift in investor priorities. Companies like Diversified, with its $500 million Anadarko bolt-on, and Mach Natural Resources, with $1.3 billion in deals entering San Juan gas and legacy Permian oil, exemplify this focus. These assets are highly valued for their predictable cash flow generation, offering a natural hedge against inflation and providing a degree of pricing upside with less volatility compared to pure exploration plays. This appeals directly to a more diverse buyer profile now entering the market, including hedge funds, asset managers, and international investors, all seeking stable returns. Our proprietary reader intent data shows that investors are increasingly asking about long-term oil price predictions for 2026 and beyond, highlighting a collective desire for stability. The focus on gas and PDP assets is a direct response to this sentiment, offering a pathway to consistent returns in a period defined by fluctuating energy prices.

Navigating the Road Ahead: Key Events and Investor Outlook

Looking ahead, we anticipate healthy deal flow to continue through the fourth quarter and into the near future, driven by robust natural gas fundamentals and sustained appetite for PDP, minerals/NonOp, and power-linked assets. The competitive landscape is intensifying, with private equity funds having raised over $10 billion in new capital and actively funding veteran teams on the hunt for attractive assets. For investors, the immediate future is heavily influenced by critical upcoming events. We note the OPEC+ Joint Ministerial Monitoring Committee (JMMC) Meeting scheduled for April 19, followed by the full OPEC+ Ministerial Meeting on April 20. These gatherings are paramount, especially given the frequent reader inquiries regarding current OPEC+ production quotas and their potential impact on global supply. The outcome of these discussions could significantly influence crude price stability, directly affecting M&A valuations. Further insights into U.S. supply-demand dynamics will come from the API and EIA Weekly Petroleum Status Reports on April 21/22 and April 28/29, alongside the Baker Hughes Rig Count reports on April 24 and May 1, providing crucial indicators of drilling activity and future production trends that will shape the investment thesis for the coming months.