The global oil market is once again navigating treacherous waters, with West Texas Intermediate (WTI) crude recently breaching significant price levels on the back of escalating geopolitical tensions. While the initial surge was stark, prompting immediate investor concern regarding supply disruptions, the market’s trajectory remains complex, influenced by a delicate balance of heightened risk premiums, strategic responses, and underlying demand fundamentals. Understanding these dynamics is crucial for investors positioning their portfolios in the current volatile energy landscape.

Geopolitical Premiums Drive Market Volatility

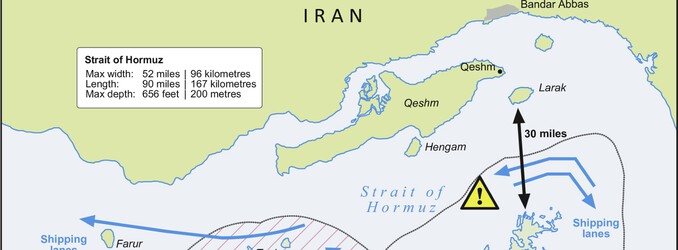

The primary catalyst for recent price movements has been the increasingly precarious situation in the Middle East, particularly concerning the Strait of Hormuz. This critical maritime chokepoint, through which an estimated 20% of the world’s daily oil supply typically transits, has seen a dramatic reduction in shipping activity. Proprietary vessel tracking data indicates that traffic through the strait has plunged by over 95%, reflecting a severe reluctance among tanker owners to navigate the route despite indications of available insurance coverage. This virtual halt underscores the market’s deep apprehension about the potential for sustained disruption to Persian Gulf oil exports.

The immediate consequence for energy markets was a sharp upward repricing of crude. WTI crude, for instance, saw a substantial jump, settling near $81/bbl at its peak, marking its highest level in over 20 months. While the initial move saw Brent also closing above $85/bbl, the subsequent market response has been mixed. “If we see even one more successful strike on an oil tanker or infrastructure, or sustained disruption, prices can spike sharply again,” noted a senior market analyst, echoing the pervasive fear of a widening conflict that could further tighten global supply. This sentiment embeds a significant geopolitical risk premium into current crude valuations.

Current Market Snapshot and Divergent Trends

As of today, Brent crude trades at $93.04 per barrel, reflecting a slight dip of 0.21% within a daily range of $92.57 to $94.21. Similarly, WTI crude is priced at $89.43 per barrel, down 0.27% for the day, having traded between $88.76 and $90.71. These figures represent a modest cooling from recent highs, yet remain elevated, signifying the persistent underlying tension. Interestingly, our proprietary 14-day trend analysis reveals that Brent crude has actually shed approximately 7% of its value over the past two weeks, declining from $101.16 on April 1st to $94.09 by April 21st. This broader trend suggests that while intraday and immediate-term reactions to geopolitical events can be sharp, the market may also be factoring in potential de-escalation or strategic interventions over a slightly longer horizon.

The initial rally saw WTI gaining faster than Brent, a phenomenon attributed to traders seeking barrels perceived as less exposed to the immediate shipping bottlenecks in the Gulf. However, the ripple effects of the Middle East conflict are now broadly impacting fuel markets globally. Freight rates have surged, and gasoline prices have also felt the pinch, with our data showing gasoline at $3.11 today, down 0.64% but still elevated. Major importing nations are already responding: China has directed its refiners to halt diesel and gasoline exports to secure domestic supply, while Japanese refiners are pressing their government for potential strategic reserve releases. Kuwait, a key regional producer, has also cut refinery processing rates as regional supply chains tighten. These actions underscore the market’s fragility and the global interconnectedness of energy supply.

Navigating Investor Concerns and Upcoming Catalysts

Our proprietary reader intent data reveals a prevalent question among investors this week: “is wti going up or down?” This reflects the deep uncertainty surrounding crude oil’s short-term trajectory. While the geopolitical risk premium suggests upward pressure, potential counter-measures introduce downside risk. The previous administration’s consideration of releasing crude from the U.S. Strategic Petroleum Reserve (SPR) and even Treasury purchases of oil futures illustrate the political will to address sharp price rallies. Such interventions, if implemented, could quickly cap further upside. Investors are also keenly asking about the “price of oil per barrel by end of 2026,” highlighting a longer-term concern about market stability amidst ongoing global shifts and potential for prolonged conflict.

Forward-looking analysis is therefore paramount. The coming weeks are packed with key data releases that will offer further clarity on market fundamentals. Investors should closely monitor the upcoming EIA Weekly Petroleum Status Reports on April 22nd, April 29th, and May 6th, which provide crucial insights into U.S. crude oil and product inventories, refinery activity, and demand. Similarly, the API Weekly Crude Inventory reports on April 28th and May 5th will offer a preliminary look at U.S. stock changes. Furthermore, the Baker Hughes Rig Count on April 24th and May 1st will indicate trends in U.S. drilling activity, a key determinant of future supply. These data points, combined with the EIA Short-Term Energy Outlook on May 2nd, will be instrumental in shaping market expectations and could trigger significant price movements, helping investors refine their outlook beyond the immediate geopolitical headlines.

Strategic Implications for Energy Portfolios

For investors, the current environment demands a nuanced approach. The elevated risk premium embedded in crude prices suggests that producers with resilient supply chains and diversified operations may offer some insulation against regional disruptions. However, the potential for government intervention, such as SPR releases, could cap upside, making sustained, parabolic rallies less likely. The widening impact on global fuel markets, evidenced by rising freight costs and national strategic responses, also hints at potential shifts in refining margins and regional fuel dynamics.

Investors should carefully evaluate their exposure, considering not just crude oil futures but also the performance of integrated energy majors, refiners, and shipping companies, all of whom are directly impacted by these macro forces. While the immediate focus is on the Strait of Hormuz, the broader implications for energy security and global trade routes will likely persist, influencing investment decisions well beyond the current news cycle. Vigilance and adaptability will be key to navigating this complex and potentially rewarding period in the oil and gas sector.