The economic landscape often presents intriguing paradoxes, and for energy investors, discerning genuine signals from market noise is paramount. A burgeoning localized boom in San Francisco’s advertising market, driven by the relentless expansion of AI companies, offers a fascinating micro-level indicator of intense economic activity and rising inflationary pressures. While seemingly distant from the global oil and gas complex, this phenomenon highlights fierce competition for resources and capital, a dynamic that ultimately informs broader commodity demand and pricing. The question for astute investors is whether this localized surge represents an early warning of broader economic expansion that will eventually underpin energy demand, or if it remains an isolated pocket of prosperity against a more cautious global backdrop.

San Francisco’s Advertising Frenzy: A Microcosm of Macro Trends

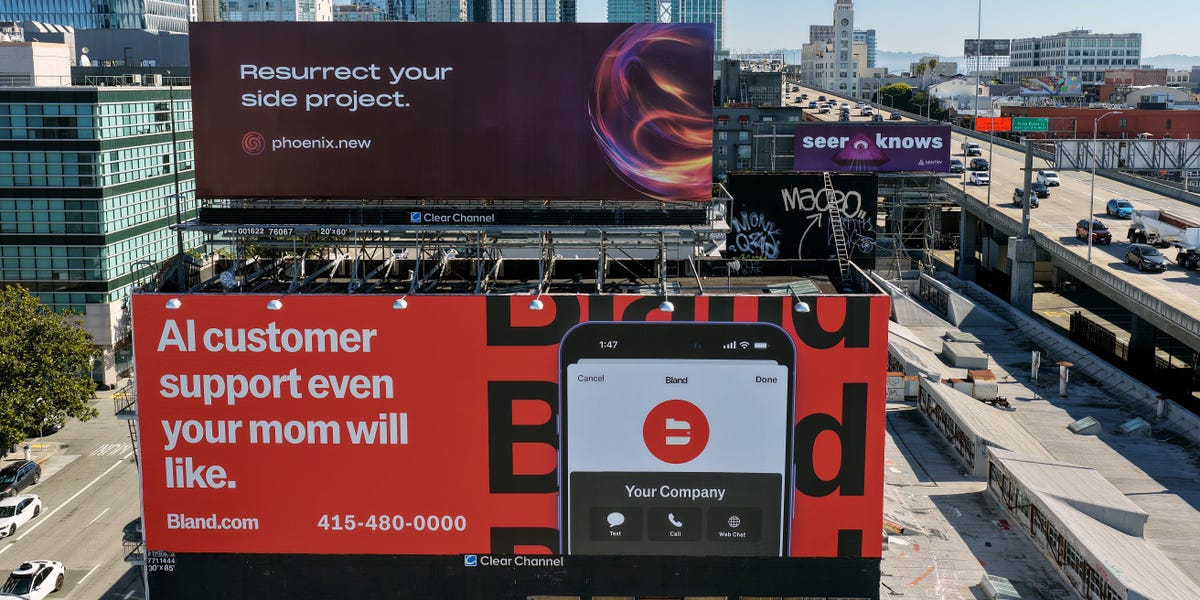

The current scramble for billboard space in San Francisco is more than just a quirky anecdote; it’s a potent signal of robust economic health within the tech sector and emerging inflationary pressures. New AI companies, fresh from successful funding rounds, are facing significant hurdles to secure prime advertising locations. Waiting lists extend six to nine months for general billboard space, with premium spots around tech hubs like Y Combinator’s Dogpatch outpost or Jackson Square already completely sold out for all of 2026, with no clear future availability. This hyper-competitive environment mirrors a broader shift where enterprise startups are adopting consumer marketing playbooks, aggressively vying for visibility.

This surge in demand has translated directly into price hikes. Industry observers note that rates are projected to increase by as much as 40% in some locations next year. This is a dramatic reversal from just two years ago, when billboard companies frequently offered steep discounts on unsold inventory. Now, space is snapped up within 24 hours when it rarely becomes available, leading to what some describe as “hoarding” as companies lock down advertising real estate for as long as possible. The primary driver, according to those on the ground, is the “insane competition” among AI companies, alongside major events like the World Cup and Super Bowl, collectively creating an unprecedented scarcity. Clear Channel Outdoor has even cited San Francisco as a key contributor to its U.S. revenue growth, underscoring the significance of this localized boom. For energy investors, this micro-level inflation in advertising costs and fierce competition for physical assets serves as a potential bellwether for broader economic overheating and resource scarcity, which historically translates into higher energy demand and prices down the line.

Current Energy Market Dynamics: A Divergent Narrative

Despite the strong inflationary signals emanating from specific economic sectors like tech advertising, the broader energy market is currently displaying a distinctly different sentiment. As of today, April 19, 2026, Brent Crude trades at $90.38 per barrel, marking a significant 9.07% decline within the day, with its trading range stretching from $86.08 to $98.97. Similarly, WTI Crude is priced at $82.59, down 9.41% for the day, having seen a range of $78.97 to $90.34. Gasoline prices are also experiencing downward pressure, currently at $2.93, a 5.18% drop for the day. This daily volatility follows a more sustained bearish trend, with Brent crude having fallen by $22.4, or 19.9%, from $112.78 on March 30 to its current $90.38.

This divergence between localized economic exuberance and a softening global energy complex presents a critical analytical challenge. The steep decline in crude prices suggests broader market concerns about demand, potential oversupply, or macroeconomic headwinds that are not yet reflected in the hyper-competitive San Francisco tech market. Investors are keenly asking what the price of oil per barrel will be by the end of 2026, and the current market action provides a stark contrast to the inflationary signals observed elsewhere. While the AI boom is undoubtedly driving capital and activity in select pockets, the energy sector’s current trajectory suggests either a delay in the broader economic impact reaching global commodity markets, or that other, more powerful deflationary or demand-dampening forces are at play. Understanding this disconnect is crucial for positioning portfolios effectively in the coming months.

Upcoming Catalysts and Investor Outlook

The immediate future holds several pivotal events that could significantly influence the prevailing bearish sentiment in the energy markets and perhaps bridge the gap between localized economic strength and global commodity prices. This week, the focus shifts to OPEC+, with the Joint Ministerial Monitoring Committee (JMMC) Meeting scheduled for today, April 19, followed by the full OPEC+ Ministerial Meeting tomorrow, April 20. Investors, particularly those asking about OPEC+’s current production quotas, will be closely watching for any signals regarding supply policy. Given the recent price decline, any indication of continued production cuts or even deeper reductions could provide a much-needed floor for prices, potentially reversing the recent downward trend. Conversely, a decision to ease cuts could exacerbate the current price weakness.

Beyond OPEC+, the market will process critical inventory data. The API Weekly Crude Inventory report on April 21, followed by the authoritative EIA Weekly Petroleum Status Report on April 22, will offer crucial insights into U.S. supply and demand dynamics. These reports will be repeated on April 28 and April 29, respectively, providing continuous updates. Any significant build in inventories could reinforce bearish sentiment, while unexpected drawdowns might signal stronger underlying demand than currently perceived, perhaps even reflecting broader economic activity like that seen in San Francisco. Furthermore, the Baker Hughes Rig Count on April 24 and May 1 will provide a gauge of future production capacity, offering another piece of the puzzle for investors trying to predict oil prices by the end of 2026. These events, particularly the OPEC+ deliberations and inventory figures, will be instrumental in shaping market expectations and could either confirm the current bearish trajectory or introduce bullish catalysts that start to align global energy prices with the localized inflationary pressures observed in booming tech hubs.

Inflationary Signals and Energy Sector Resilience

The localized inflationary pressures evident in the San Francisco advertising market, driven by the tech sector’s robust growth, serve as a reminder that economic activity can be highly uneven. While oil prices have recently faced headwinds, the underlying demand for energy is inherently linked to overall economic expansion. If the concentrated growth in the AI sector begins to diffuse into broader economic activity, creating more widespread demand for goods, services, and infrastructure, the current divergence between micro-level inflation and macro-level energy price weakness may begin to close. Rising input costs, whether for advertising or other essential services, can eventually translate into higher operational expenditures for all industries, including the energy sector. This could impact capital expenditure decisions and ultimately the cost of bringing new supply online.

For oil and gas companies, sustained inflationary pressures, even if initially localized, can present a dual challenge and opportunity. While rising costs for equipment, labor, and services could squeeze margins, a broadening inflationary environment typically corresponds with increased energy demand as industrial activity picks up and consumer spending rises. Companies like Repsol, which some of our readers are tracking closely for April 2026 performance, operate within this complex interplay of global supply dynamics, regional demand signals, and overarching macroeconomic trends. The ability of energy producers to manage rising costs while capitalizing on eventual demand growth will be key. Investors should monitor these localized economic hotspots as potential leading indicators, understanding that persistent economic vigor in key sectors will, in time, likely translate into renewed upward pressure on global energy prices, even if current market sentiment suggests otherwise.