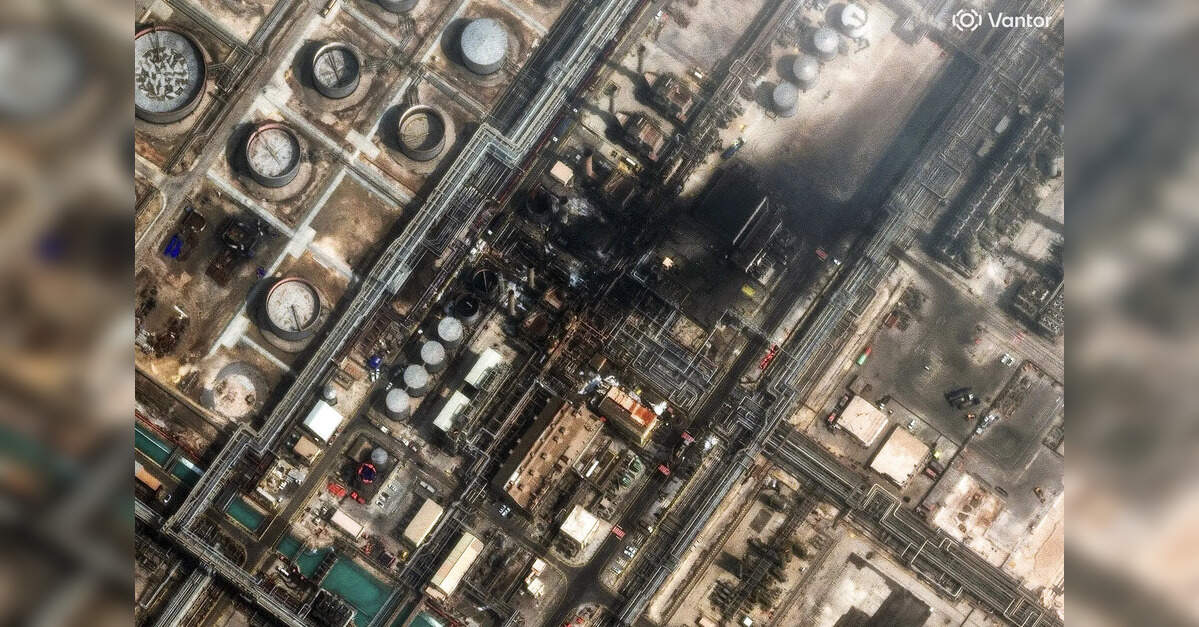

The early March incidents at Saudi Aramco’s vital Ras Tanura oil export terminal served as a stark reminder of the persistent geopolitical risks threatening global energy supplies. While the direct impacts of unidentified projectiles striking one of the world’s largest crude shipment hubs might have initially sent jitters through the market, the subsequent weeks have painted a more complex picture. For investors navigating the volatile oil and gas landscape, these events underscore the critical need to distinguish between immediate shocks and the broader, often counter-intuitive, market trends. Our analysis delves into the market’s response, investor concerns, and the crucial upcoming events that will shape the trajectory of crude prices, all against the backdrop of enduring regional tensions.

The Disconnect: Geopolitical Risk vs. Current Price Action

The early March strikes on Ras Tanura, including a reported drone attack that temporarily shut down the complex, highlighted the vulnerability of critical infrastructure near the Strait of Hormuz. Such incidents typically trigger an immediate spike in crude prices, reflecting a geopolitical risk premium. However, the market’s reaction in the weeks following these events tells a compelling story of other dominant forces at play. As of today, Brent crude trades at $90.38, while WTI crude stands at $82.59. This current pricing represents a significant retreat from recent highs. In fact, our proprietary 14-day Brent trend data reveals a substantial decline from $112.78 on March 30 to the current $90.38 on April 17, representing a nearly 20% drop. This apparent disconnect suggests that while the Ras Tanura incidents were grave, their immediate impact on prices was either short-lived or overshadowed by other prevailing market anxieties, perhaps concerning global economic growth, demand outlooks, or ample existing supply. This complex interplay of geopolitical tension and broader macroeconomic sentiment is a key challenge for investors attempting to accurately price risk.

Investor Ponderings: Pricing Uncertainty into the Future

In a market where geopolitical events can spark rapid shifts, investors are consistently grappling with fundamental questions that drive their strategies. A core inquiry we observe from our reader intent data is “is WTI going up or down?” alongside broader predictions like “what do you predict the price of oil per barrel will be by end of 2026?”. The early March Ras Tanura attacks, though now weeks in the past, serve as a potent illustration of the unpredictable variables that complicate these forecasts. While the market has since corrected downwards, these incidents are a constant reminder that the underlying security of supply from the Middle East remains a critical, often unquantifiable, risk factor. The strategic importance of Saudi Aramco’s facilities and their proximity to vital shipping lanes means that any renewed escalation of regional hostilities, particularly those tied to the intensifying tensions between Israel and Iran, could quickly re-inject a significant risk premium into crude prices, forcing investors to reassess their short-term and long-term outlooks.

Upcoming Catalysts and Their Interplay with Geopolitics

The coming weeks are packed with scheduled events that will interact with the lingering geopolitical backdrop, offering crucial signals for oil and gas investors. A primary focus will be the OPEC+ Joint Ministerial Monitoring Committee (JMMC) Meeting on April 20, followed closely by the full OPEC+ Ministerial Meeting on April 25. While the Ras Tanura incidents didn’t lead to an immediate supply disruption, the memory of such vulnerabilities could subtly influence the bloc’s discussions around production quotas. Will OPEC+ maintain its cautious approach, or could perceived geopolitical instability lead to considerations for adjusting output to either stabilize markets or capitalize on potential tightness? Simultaneously, the market will absorb critical supply and demand indicators from the U.S. with the API Weekly Crude Inventory reports on April 21 and April 28, and the EIA Weekly Petroleum Status Reports on April 22 and April 29. These inventory figures will provide insight into the robustness of demand and the adequacy of existing supply, potentially amplifying or dampening any renewed geopolitical concerns. Furthermore, the Baker Hughes Rig Count reports on April 24 and May 1 will offer a forward-looking perspective on future drilling activity and supply potential. Investors must monitor these events closely, as their outcomes, when filtered through the lens of ongoing regional tensions, will dictate near-term price volatility.

Strategic Implications for Oil & Gas Portfolios

The recent history, from the early March attacks on Ras Tanura to the subsequent market price correction, underscores the dynamic and often paradoxical nature of oil and gas investing. While a direct threat to a major export facility might intuitively suggest higher prices, the market’s broader narrative, heavily influenced by macroeconomics and supply/demand fundamentals, can diverge significantly. For investors, this demands a highly nuanced approach. It is crucial to monitor not only the immediate geopolitical headlines but also the underlying economic currents and the strategic decisions made by key players like OPEC+. The persistent vulnerability of energy infrastructure in the Middle East, coupled with escalating regional tensions, means that the potential for rapid and dramatic shifts in crude prices remains ever-present. Investors should build resilience into their portfolios, understanding that while current pricing may reflect a discount to geopolitical risk, the landscape can change instantaneously. Staying informed about upcoming data releases and strategic meetings, such as the imminent OPEC+ gatherings, is paramount for navigating the inherent volatility and identifying both risks and opportunities in this complex market.