The global energy market is once again holding its breath as Qatar, a titan in liquefied natural gas (LNG) exports, navigates the treacherous waters of geopolitical conflict. Reports indicate a potential resumption of LNG shipments from the critical Ras Laffan complex, following an unprecedented force majeure declaration that sent ripples of concern through global supply chains. While this development offers a glimmer of hope for buyers, a closer look reveals a nuanced situation fraught with ongoing risks, particularly concerning the vital Strait of Hormuz. For energy investors, understanding the implications of this tentative return, coupled with broader market dynamics and upcoming data releases, is paramount to strategic positioning.

Qatar’s Tentative Return and the Hormuz Bottleneck

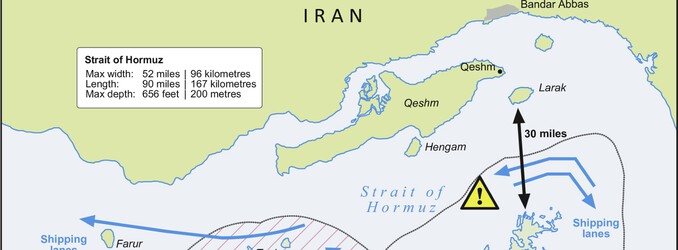

After a period of significant uncertainty and a declaration of force majeure, there are signs that Qatar is beginning to restore its LNG export operations. Shipping data suggests a cargo was loaded from the Ras Laffan complex, with the vessel signaling Bangladesh as its likely destination and an estimated arrival around March 14. This initial step is a cautiously positive development following the recent halt in production triggered by escalating regional hostilities. However, the journey for this, and indeed any future cargo, remains precarious. The critical Strait of Hormuz, a chokepoint accounting for approximately one-fifth of global LNG supplies, continues to be a high-risk navigation zone for commercial shipping. The very real possibility of the loaded tanker being used as floating storage until safe passage is assured underscores the fragility of the situation. While production may be restarting, the logistics of delivery are still very much at the mercy of geopolitical tensions, making any full return to normalcy dependent on de-escalation in the region.

Market Response: Crude Stability Amidst LNG Uncertainty

Despite the significant supply uncertainty surrounding Qatari LNG, crude oil markets have shown a degree of resilience, albeit with a slight downturn today. As of today, Brent crude trades at $92.77 per barrel, reflecting a modest decrease of 0.5% within a day range of $92.57 to $94.21. Similarly, WTI crude stands at $89.24, down 0.48%, fluctuating between $88.76 and $90.71. Gasoline prices also mirrored this trend, settling at $3.1, a 0.96% dip for the day. This immediate market reaction suggests that while the Qatari situation is a concern, other factors might be currently tempering broader energy price spikes. Looking at the broader trend, Brent crude has seen a more significant decline, falling from $101.16 on April 1st to $94.09 by April 21st, representing a 7% contraction over two weeks. This indicates that the market has either priced in some of the geopolitical risk or is currently more influenced by broader demand concerns or inventory levels. Investors are clearly weighing the immediate regional disruptions against global economic signals and the potential for a more stable supply picture in other regions, preventing a more dramatic bullish response to the Qatari news.

Forward Outlook: Key Dates for Energy Investors

The evolving situation in the Middle East, particularly the ongoing challenges in the Strait of Hormuz, demands a vigilant eye on both geopolitical developments and critical market data. For investors looking to anticipate future price movements and supply stability, several upcoming events on the energy calendar will be particularly insightful. This week, the EIA Weekly Petroleum Status Report on April 22nd will provide crucial insights into U.S. crude oil, gasoline, and distillate inventories, offering a snapshot of domestic supply-demand balances. The Baker Hughes Rig Count on April 24th will shed light on North American drilling activity, a key indicator for future production capacity. As we move into the next week, the API Weekly Crude Inventory on April 28th and another EIA Weekly Petroleum Status Report on April 29th will continue to shape perceptions of market tightness or surplus. Looking further ahead, the EIA Short-Term Energy Outlook on May 2nd will be a critical release, offering updated forecasts for global oil and natural gas markets, likely incorporating the recent geopolitical events and their potential long-term impact on supply and prices. These data points, combined with any progress or setbacks regarding safe passage through the Strait of Hormuz, will be instrumental in forming investment strategies in the coming weeks.

Addressing Investor Concerns: Navigating Volatility and Long-Term Value

Our proprietary reader intent data reveals a diverse set of concerns among investors this week, all pointing to a heightened focus on market direction and strategic positioning. Many are directly asking about the immediate trajectory of benchmarks, with clear interest in whether “WTI is going up or down.” This reflects the anxiety surrounding short-term volatility driven by events like the Qatari LNG disruption. Beyond the daily swings, there’s a strong appetite for a clearer long-term perspective, as evidenced by questions asking for “predictions for the price of oil per barrel by end of 2026.” This indicates that while immediate geopolitical risks are being monitored, investors are also evaluating the fundamental shifts that could impact their portfolios over a longer horizon. Furthermore, inquiries about specific companies, such as “how well do you think Repsol will end in April 2026,” highlight a focus on how individual energy players are positioned to absorb market shocks, manage diversified portfolios, and capitalize on evolving energy landscapes. For investors, the challenge is to synthesize the immediate news from Qatar and the Middle East with these broader market fundamentals and long-term outlooks, seeking opportunities in companies with robust operational resilience and strategic agility in a volatile global energy market.