Petrobras Retail Push: Price Control Mandate

Petrobras, Brazil’s state-controlled oil giant, stands at a pivotal juncture, contemplating a strategic re-entry into the retail fuel distribution sector. This potential pivot, driven by explicit government pressure to temper consumer pump prices, marks a significant departure from its recent privatization efforts and signals a renewed emphasis on social mandates over pure market-driven efficiency. For investors, this move introduces a complex layer of political risk and raises questions about future profitability, valuation, and the company’s long-term strategic direction. As Brazil grapples with the disparity between wholesale and retail fuel costs, Petrobras finds itself once again at the forefront of a politically charged economic debate, with its board set to discuss amending its strategic plan this week.

The Price Disconnect: Government Pressure Meets Market Reality

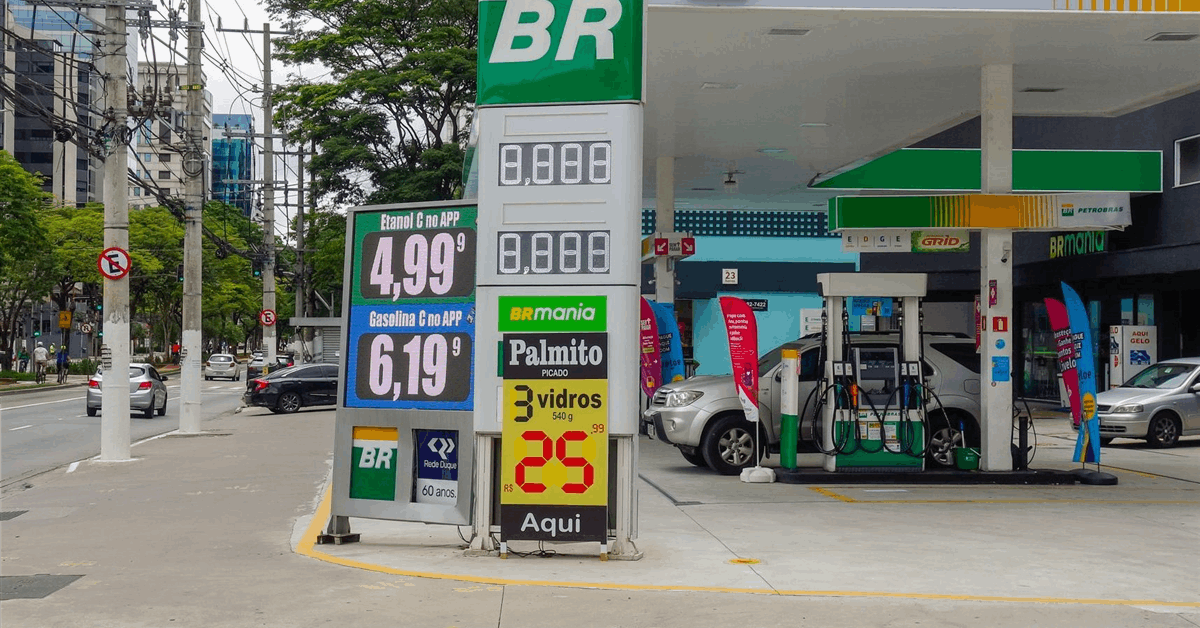

The impetus behind Petrobras’s potential retail resurgence stems directly from top-level government dissatisfaction with current fuel pricing dynamics. President Luiz Inacio Lula da Silva has vocally criticized the failure of wholesale price cuts by Petrobras to translate into lower prices at the pump for consumers. This sentiment is echoed by Petrobras CEO Magda Chambriard, who has also expressed concern over filling stations not passing on savings. As of today, Brent crude trades at $94.59, reflecting a slight daily dip of 0.36%. This is part of a broader trend, with Brent having shed nearly 8.8% over the past fortnight, dropping from $102.22 on March 25th to $93.22 on April 14th. Despite this significant retreat in global crude benchmarks, Brazil’s domestic pump prices have seemingly remained stubbornly high, exacerbating the government’s frustration. The attorney general’s office has even requested an investigation into potential anti-competitive practices within the distribution and retail sectors, underscoring the severity of the perceived problem. Lula’s argument is clear: privatization created inefficiencies, exemplified by the stark difference between the 37 reais Petrobras charges for a 13-kilogram gas cylinder and the 140 reais it reaches a consumer’s home for. This perceived market failure is the core justification for a state-led intervention.

Strategic Implications and Valuation Headwinds for Petrobras

Petrobras’s board of directors is scheduled to convene this week to discuss amending the company’s 2026-2030 strategic plan to include a retail presence. This proposal aims to position Petrobras as a “diversified and integrated energy company,” a significant shift from the previous administration’s drive towards divestment and market liberalization, which saw the privatization of Vibra Energia SA (formerly BR Distribuidora) four years ago. The potential re-entry could take several forms: attempting to fully re-nationalize Vibra, acquiring a stake in the convenience-store operator and distributor, or building out new retail infrastructure. Each option carries substantial capital expenditure implications, regulatory hurdles, and varying degrees of market disruption. Notably, Petrobras already notified Vibra last year that it was not interested in renewing their brand licensing agreement under current terms beyond its mid-2029 expiration. For investors, this strategic pivot introduces considerable uncertainty. While an integrated model might offer theoretical synergies, a return to retail, particularly under a mandate to control consumer prices, traditionally compresses margins and exposes the company to direct political interference. The focus shifts from maximizing shareholder value to fulfilling a social function, which historically has led to underperformance relative to purely commercial energy peers.

Forward Outlook: Navigating Global Markets and Domestic Mandates

The timing of Petrobras’s retail considerations is particularly salient given the current global energy landscape and upcoming market events. Looking ahead, the global crude market remains dynamic, with critical catalysts on the horizon. Investors will closely monitor the upcoming OPEC+ meetings, with the Joint Ministerial Monitoring Committee (JMMC) scheduled for April 18th and the Full Ministerial Meeting on April 20th. Any decisions regarding production quotas could significantly impact Brent’s trajectory. If OPEC+ opts for tighter supply, pushing crude prices higher, Petrobras’s re-entry into retail would immediately face heightened scrutiny regarding its ability to shield consumers from rising costs. This scenario could force the company into a difficult position, potentially necessitating subsidies or mandated losses in the retail segment to align with government price control objectives. Conversely, if global crude prices decline, the pressure to control retail prices might ease slightly, but the underlying strategic mandate for state intervention would remain. Furthermore, the weekly API and EIA inventory reports on April 21st/22nd and April 28th/29th will offer fresh insights into supply-demand balances, further informing the crude price outlook that Petrobras’s retail operations would be directly exposed to.

Investor Concerns: The Price Control Paradox and Future Forecasts

Our proprietary reader intent data reveals a consistent focus this week on forecasting Brent prices for the next quarter and the broader 2026 consensus. This underlying concern about commodity price stability is directly challenged by Petrobras’s potential strategic shift. For investors, the looming prospect of a price control mandate creates a paradox: a move intended to stabilize consumer prices in Brazil could inherently destabilize investor confidence in Petrobras’s market-driven profitability and long-term valuation. The primary concern is the erosion of free cash flow and dividend prospects if retail operations are compelled to absorb losses or operate at suppressed margins to meet government objectives. The risk premium associated with Petrobras as a state-controlled entity, already a factor, would likely expand further. Investors assess companies based on their ability to generate sustainable, predictable earnings, and direct government intervention in pricing undermines this fundamental principle. This strategic re-orientation could redefine Petrobras’s investment profile, shifting it further from a pure-play energy producer towards a utility-like entity with greater social obligations, demanding a re-evaluation of its earnings potential and discount rates in the face of political risk.