The global oil market finds itself at a critical juncture, gripped by heightened geopolitical tensions in the Middle East that have directly impacted vital energy transit routes. Recent escalations, including reported disruptions to tanker traffic through the Strait of Hormuz and targeted strikes on regional energy infrastructure, have reignited fears of supply instability. While initial reactions saw a dramatic single-day price spike, our proprietary data indicates that the market has since settled into a significantly elevated pricing environment, reflecting a persistent geopolitical risk premium. As an investment analyst, understanding the nuances of these developments, combined with forward-looking market signals and investor sentiment, is paramount for navigating the volatile landscape ahead.

Geopolitical Premium Sustains Elevated Prices: A Current Market Snapshot

The immediate aftermath of the escalating conflict witnessed crude prices posting their most substantial daily gains in four years. However, the market has not merely retreated to pre-crisis levels; it has recalibrated to a new, higher baseline. As of today, Brent Crude trades at $93.83 per barrel, marking a +0.63% increase within its daily range of $93.52-$94.21. Similarly, WTI Crude stands at $90.43, up +0.85% for the day. These figures are significantly above the “briefly topping $80/bbl” reported during the initial surge, indicating a sustained and deepening geopolitical premium now baked into prices.

While the immediate market reaction was a sharp ascent, our 14-day Brent trend data reveals a more complex picture, showing a decline from $118.35 on March 31st to $94.86 on April 20th, a nearly 20% pullback. This suggests that while the current price of $93.83 is high, it represents a rebound from a recent dip, highlighting the extreme volatility and sensitivity of the market to both geopolitical events and broader supply-demand dynamics. Diesel futures, mirroring crude’s volatility, also saw substantial jumps, and natural gas markets tightened following reports of Qatar’s largest LNG export facility temporarily halting operations and a drone strike impacting Saudi Aramco’s Ras Tanura refinery, even as crude exports continued from the adjacent port. The “critical” threat level declared by maritime security agencies in the Persian Gulf continues to prompt many shipowners to reroute or delay transit through the Strait of Hormuz, a conduit for approximately 20% of global oil and LNG flows.

Navigating the Calendar: Upcoming Events and Forward Supply Signals

The trajectory of oil prices in the coming weeks will hinge not only on geopolitical de-escalation but also on a series of critical market events. Today, April 21st, the OPEC+ Joint Ministerial Monitoring Committee (JMMC) convenes. This meeting is particularly significant given the current supply anxieties. While OPEC+ previously reaffirmed plans to increase output by 206,000 barrels per day next month, the pressing question for investors is whether the current crisis will prompt a reassessment or if the group will maintain its course, relying on its limited spare capacity, largely concentrated in Saudi Arabia and the UAE, which analysts warn offers only restricted relief against persistent Hormuz disruptions.

Further insights into the physical market will emerge with the EIA Weekly Petroleum Status Reports scheduled for April 22nd and April 29th. These reports will be intensely scrutinized for any measurable impacts on U.S. crude inventories and refining activity, potentially providing early indicators of global supply-chain stress. The Baker Hughes Rig Count on April 24th and May 1st will offer a glimpse into North American production trends, a crucial non-OPEC supply source. Looking slightly further ahead, the EIA Short-Term Energy Outlook on May 2nd will provide updated forecasts that will undoubtedly incorporate the latest geopolitical developments, offering a revised baseline for analysts and investors forecasting end-of-year prices.

Addressing Investor Concerns: Price Trajectory and Portfolio Impact

Our proprietary reader intent data reveals a consistent theme among investors this week: a palpable anxiety about future oil price direction. Questions like “Is WTI going up or down?” and “What do you predict the price of oil per barrel will be by end of 2026?” underscore the urgent need for clarity in a highly uncertain environment. Investors are grappling with the implications of sustained high prices on global inflation, central bank policy, and the broader economic outlook, which could impact everything from consumer spending to corporate earnings across various sectors.

Current market forecasts are being rapidly re-evaluated. While analysts from Citigroup recently anticipated Brent to trade in the $80-$90/bbl range and Morgan Stanley raised its second-quarter forecast to $80/bbl, the current trading price of Brent at $93.83 already exceeds the upper bound of some of these near-term projections. Wood Mackenzie’s warning that crude could surpass $100/bbl if tanker traffic through Hormuz is not quickly restored now seems increasingly plausible. For investors holding positions in energy majors or considering new entries, the key will be to differentiate between short-term speculative spikes and a more fundamental shift in the supply-demand balance driven by prolonged disruption. The impact on specific companies, like the interest our readers show in the performance of firms such as Repsol, will ultimately be tied to their operational resilience and hedging strategies in this volatile environment.

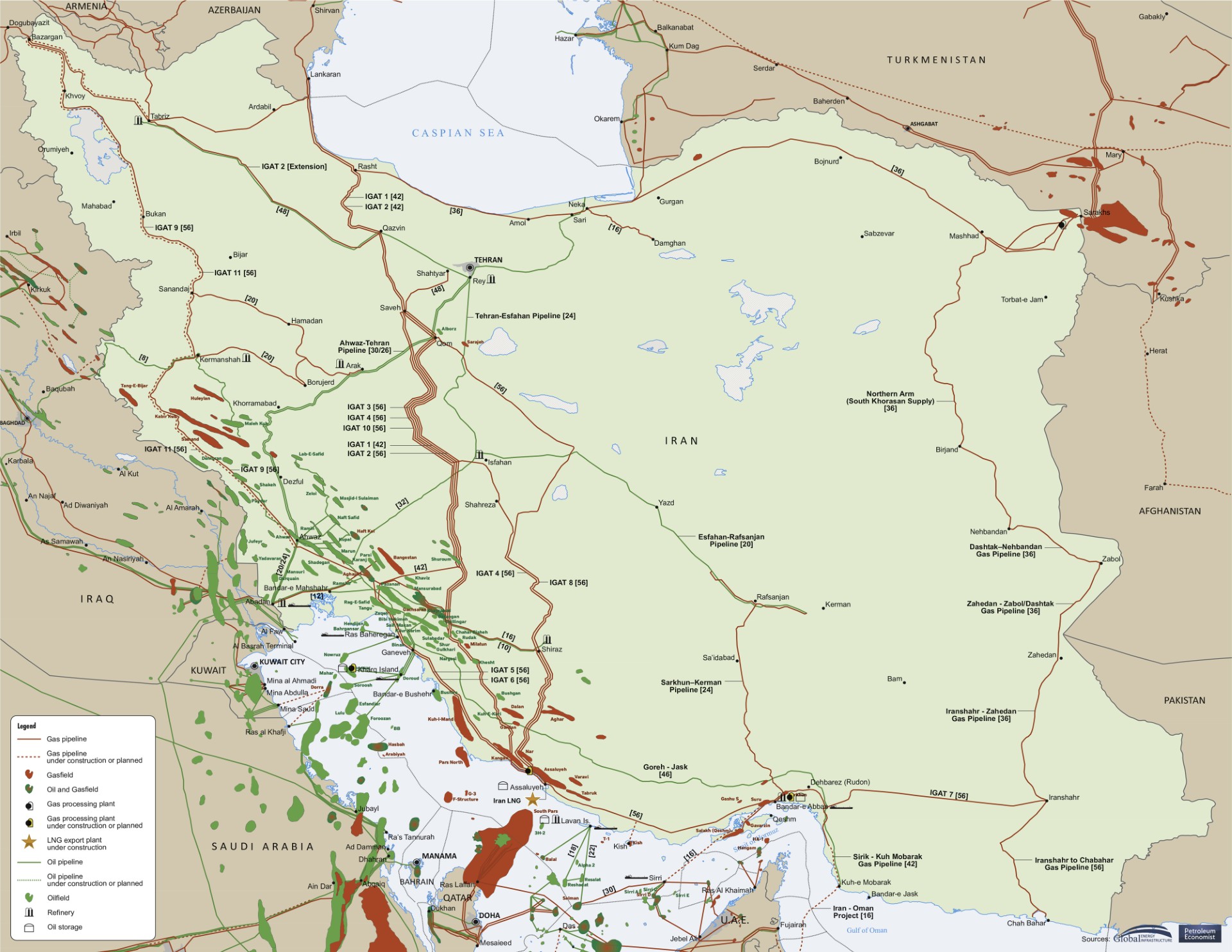

The Enduring Shadow of Hormuz: Supply Vulnerability and Global Implications

The Strait of Hormuz remains the world’s most critical oil chokepoint, and its vulnerability has been starkly highlighted. With roughly 20% of global oil flows and a similar share of liquefied natural gas exports transiting this narrow channel, any prolonged disruption carries immense global consequences. JPMorgan’s estimate that a 25-day disruption could force producing nations to curb output as storage fills underscores the severe implications for physical supply. While global supplies were considered relatively well-balanced prior to the current hostilities, the sudden imposition of a “geopolitical premium” and the threat of physical supply constraints fundamentally alter that equilibrium.

Beyond the immediate price shock, a sustained surge in crude prices would inevitably exacerbate inflationary pressures worldwide, complicating the delicate balancing act faced by central banks striving to manage economic growth alongside price stability. Even Iran, despite producing approximately 3.3 million barrels per day (about 3% of global supply), wields outsized influence due to its strategic position along Hormuz. The market is now pricing in a tangible disruption risk, and the future trajectory of tanker flows through the Strait, alongside the status of regional energy infrastructure, will be the ultimate determinants of whether the current price elevation is a temporary spike or the precursor to a more enduring global supply shock.