The recent U.S. strike in the vicinity of Iran’s Kharg Island has significantly escalated geopolitical tensions in the Middle East, casting a renewed shadow of uncertainty over global oil supply stability. While initial reports indicate no direct damage to critical oil infrastructure on the island, the incident underscores the profound vulnerability of the region’s energy export capabilities. For investors navigating an already volatile energy market, this development amplifies the need for vigilance and a nuanced understanding of potential supply disruptions that could ripple through global crude flows and impact oil prices.

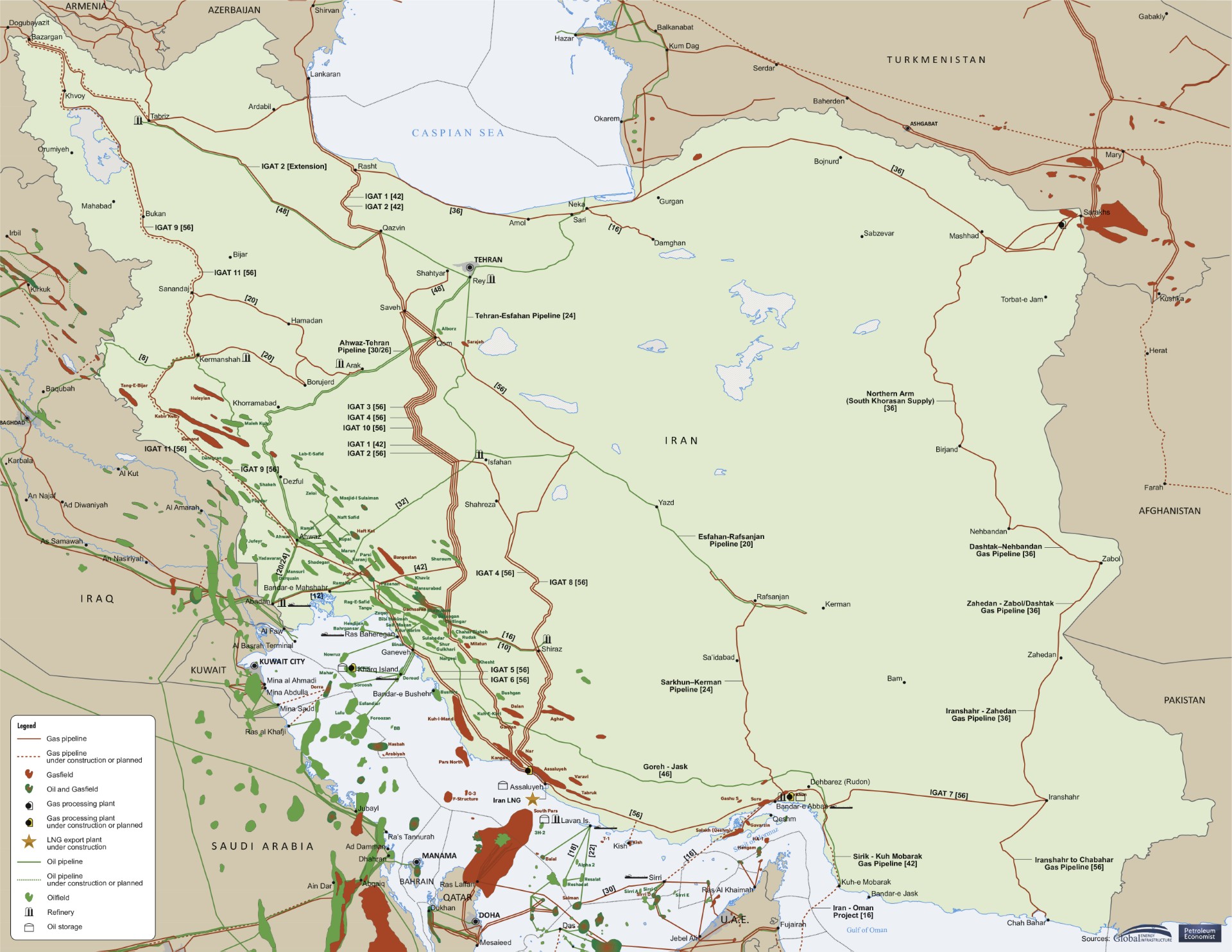

Kharg Island: A Critical Bottleneck for Iranian Exports

Kharg Island stands as Iran’s primary crude export terminal, handling approximately 90% of the nation’s crude shipments, with a substantial majority destined for China. The strategic importance of this facility cannot be overstated; its disruption could swiftly force Iran to curtail production and place a significant portion of its exports at risk, as highlighted by leading market analysts. Although monitoring firms like TankerTrackers.com reported normal loading operations hours after the strike, and Iranian media affirmed continued exports, the mere proximity of military action to such a vital node serves as a stark reminder of potential supply chain fragilities. This event occurs against a backdrop of existing pressures on global energy markets, particularly concerning the Strait of Hormuz, a crucial choke point that typically funnels roughly one-fifth of the world’s oil and natural gas exports. The threat of retaliation from Iran against U.S.-linked energy facilities across the region further broadens the spectrum of potential targets, including critical infrastructure such as Saudi Arabia’s Ras Tanura export terminal, the Abqaiq processing hub, and the Fujairah oil hub in the United Arab Emirates. Each of these represents a linchpin in the global energy matrix, and any compromise could trigger widespread market repercussions.

Market Reaction and Investor Concerns Amidst Volatility

The immediate market response to such geopolitical tremors is always a key indicator of investor sentiment and perceived risk. As of today, Brent crude trades at $92.90, reflecting a modest downturn of 0.36% within a daily range of $92.57 to $94.21. Similarly, WTI crude is priced at $89.24, down 0.48%, fluctuating between $88.76 and $90.71. This seemingly muted reaction, considering the gravity of the situation, suggests that some level of geopolitical risk premium may already be baked into current prices, or that traders are awaiting more definitive signs of direct supply disruption. However, looking at the broader picture, our proprietary data shows Brent crude has trended downward from $101.16 on April 1st to $94.09 on April 21st, a decline of over 7%. This preceding bearish momentum might be tempering the upward pressure that would typically follow a significant supply risk event. Our reader intent data also reveals a clear focus on price direction, with common queries like “Is WTI going up or down?” and “What do you predict the price of oil per barrel will be by end of 2026?” These questions underscore investor anxiety regarding both short-term market volatility and the longer-term trajectory of crude prices, directly influenced by such unpredictable geopolitical developments. The current market action reflects a complex interplay between underlying supply/demand fundamentals and an ever-present geopolitical risk premium.

Forward Outlook: Key Data Points and Upcoming Events

In the wake of heightened Middle East tensions, investors must keenly focus on upcoming data releases for signals that could either confirm or alleviate supply concerns. The EIA Weekly Petroleum Status Report, scheduled for release on April 22nd and again on April 29th, will be a critical barometer for U.S. crude inventories, refinery activity, and product supplied, offering insights into domestic demand trends. Any unexpected drawdowns could be amplified by the prevailing geopolitical risk. Furthermore, the Baker Hughes Rig Count, due on April 24th and May 1st, will provide an indication of North American production activity, which could partially offset potential disruptions from other regions. A particularly significant forward-looking event is the EIA Short-Term Energy Outlook, slated for May 2nd. This report will offer updated forecasts for global oil supply and demand, potentially incorporating the latest geopolitical developments into its projections, thereby influencing market sentiment for the coming months. These events, coupled with API Weekly Crude Inventory reports on April 28th and May 5th, will be scrutinized for any signs of direct impact on global supply chains or a shift in the delicate balance between supply and demand. Persistent slowdowns in shipping activity through the Strait of Hormuz, which have been observed since the conflict began, will be reflected in these inventory figures and could trigger more pronounced market reactions if prolonged.

Investment Implications and Risk Mitigation Strategies

The current geopolitical landscape demands that investors in the oil and gas sector adopt a proactive and informed approach to risk management. The incident near Kharg Island serves as a potent reminder that while direct infrastructure damage was avoided this time, the threat of escalation targeting critical energy assets remains tangible. Portfolio diversification, particularly across different energy sub-sectors and geographies, can help mitigate exposure to region-specific risks. Monitoring real-time vessel tracking data and official statements from involved parties will be crucial for assessing the immediate impact of any future incidents. Furthermore, investors should consider the potential for a sustained geopolitical risk premium in crude prices, which could support higher valuations even in the absence of immediate supply disruptions. Companies with robust operational resilience, diversified supply chains, and strong hedging strategies will be better positioned to navigate this period of heightened uncertainty. While the market has not yet fully priced in a catastrophic supply disruption, the possibility of unforeseen escalation targeting key export hubs like Kharg Island or the broader Strait of Hormuz demands a continuous reassessment of risk and reward in energy investments.