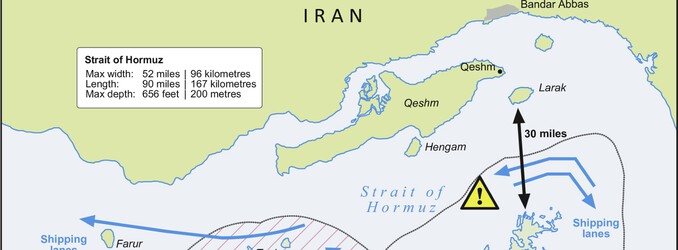

The global oil market is grappling with a rapidly escalating crisis in the Persian Gulf, as the conflict with Iran enters its second week. What began as a geopolitical shock impacting maritime transit has now morphed into a severe physical supply disruption, with potentially far-reaching consequences for energy investors. With the Strait of Hormuz effectively shut for over eight days since February 27, a staggering 17 million barrels per day (MMbpd) of crude oil and petroleum products have been removed from global availability. This evolving situation demands a keen eye from investors, as the implications extend beyond immediate price fluctuations to long-term supply dynamics and regional stability.

From Transit Woes to Production Paralysis

The initial phase of the crisis saw shipowners avoiding the critical Strait of Hormuz, turning the disruption primarily into a transportation challenge. However, the situation has quickly deteriorated, expanding into widespread production shut-ins across the Persian Gulf. As export routes remain largely constrained, storage capacity in producer nations is rapidly filling, forcing operators to curtail output. Iraq, a significant regional producer, has already idled approximately 2 MMbpd of its production, with output from its southern fields plummeting from around 3.3 MMbpd to a mere 1.3 MMbpd. Kuwait has also implemented production cuts due to similar storage limitations.

Analysts warn that the shift from a transportation bottleneck to a production crisis fundamentally alters the recovery timeline. Restarting oil field production on this scale is a massive technical undertaking, which could easily span weeks or even longer to fully restore output. Furthermore, the longer the conflict persists, the higher the risk of damage to downstream infrastructure and other critical oil facilities, which would further complicate and extend any recovery efforts, leaving investors to ponder the true cost of this protracted disruption.

Global Benchmarks vs. Regional Strain: A Divergent Market Signal

Despite the severe curtailment of 17 MMbpd from the Persian Gulf, global benchmark crude prices present a complex picture. As of today, Brent Crude trades at $92.89 per barrel, reflecting a slight decline of 0.38% within the day’s range of $92.57 to $94.21. Similarly, WTI Crude stands at $89.51 per barrel, down 0.18% from its daily high. Our proprietary analytics reveal an even more pronounced trend: Brent Crude has actually receded by over 7% since April 1st, when it traded at $101.16 per barrel. This seemingly counter-intuitive downward trajectory in global benchmarks, amidst such a profound supply shock, suggests either a market still processing the full extent of the crisis, an underlying belief in a relatively swift resolution, or perhaps other bearish macroeconomic factors tempering prices.

However, the impact is undeniably acute in specific regions. Asia, which historically receives approximately 80% of the 21 MMbpd of oil exports transiting the Strait of Hormuz, has become the epicenter of the supply crunch. Our data confirms that crude delivered to regional Asian buyers surged above $100 per barrel last week, with jet fuel and diesel prices also experiencing sharp increases. This stark divergence between global benchmark performance and localized regional price spikes highlights the uneven distribution of the crisis’s immediate effects, prompting governments like China and Thailand to restrict product exports, a measure that could spread if Persian Gulf supplies remain offline.

Navigating the Weeks Ahead: Key Data Points for Energy Investors

For investors seeking clarity amidst the volatility, the upcoming energy calendar holds critical data points that will shed further light on the market’s response to the Persian Gulf crisis. The release of the EIA Weekly Petroleum Status Report, scheduled for April 22nd, April 29th, and May 6th, will be paramount. These reports offer vital insights into U.S. crude oil and refined product inventories, providing an early indication of how global supply disruptions are translating into inventory draws outside of Asia.

Additionally, the API Weekly Crude Inventory reports on April 28th and May 5th will offer a preview of these trends. Looking slightly further ahead, the EIA Short-Term Energy Outlook on May 2nd will provide updated projections for global supply, demand, and prices, incorporating the latest geopolitical developments. While the Baker Hughes Rig Count on April 24th and May 1st offers a pulse on future drilling activity, the immediate focus for investors should remain squarely on inventory levels and revised supply forecasts, which will dictate market sentiment and price direction in the short to medium term.

Investor Focus: Pricing Geopolitical Risk and Future Price Trajectories

Our proprietary analytics, tracking the pulse of investor sentiment, reveal a palpable uncertainty regarding crude oil’s immediate trajectory. Questions about whether WTI is poised for an upward or downward movement dominate discussions, alongside more strategic inquiries into the potential price per barrel by the close of 2026. This reflects a market grappling with unprecedented geopolitical risk and the challenge of accurately pricing in such a significant, sustained supply shock.

The long-term implications of this crisis are substantial. The “massive technical exercise” required to restore 17 MMbpd of production, even after a resolution, suggests a prolonged period of tighter supply. This persistent supply constraint, coupled with the potential for further infrastructure damage, could fundamentally reset baseline expectations for crude oil prices through the end of 2026 and beyond. Investors are keenly watching for any signs of de-escalation or, conversely, an expansion of the conflict, as each scenario holds drastically different implications for portfolios heavily weighted in energy equities, futures, or related instruments. The ability to discern genuine market signals from speculative noise will be crucial in navigating these turbulent waters.