The geopolitical landscape across the Persian Gulf has escalated dramatically, with Iran issuing stark warnings that oil and gas infrastructure throughout the region could become legitimate targets. This declaration, following a reported strike on Iran’s critical South Pars gas field, immediately raises the specter of severe supply disruptions and heightened volatility in global energy markets. While the risk profile has undoubtedly intensified, our proprietary market data reveals a fascinating divergence: crude prices, after an initial surge, have since retreated, suggesting investors are grappling with the true probability and impact of these escalating threats on the world’s most vital energy artery.

Escalation and the Market’s Measured Response

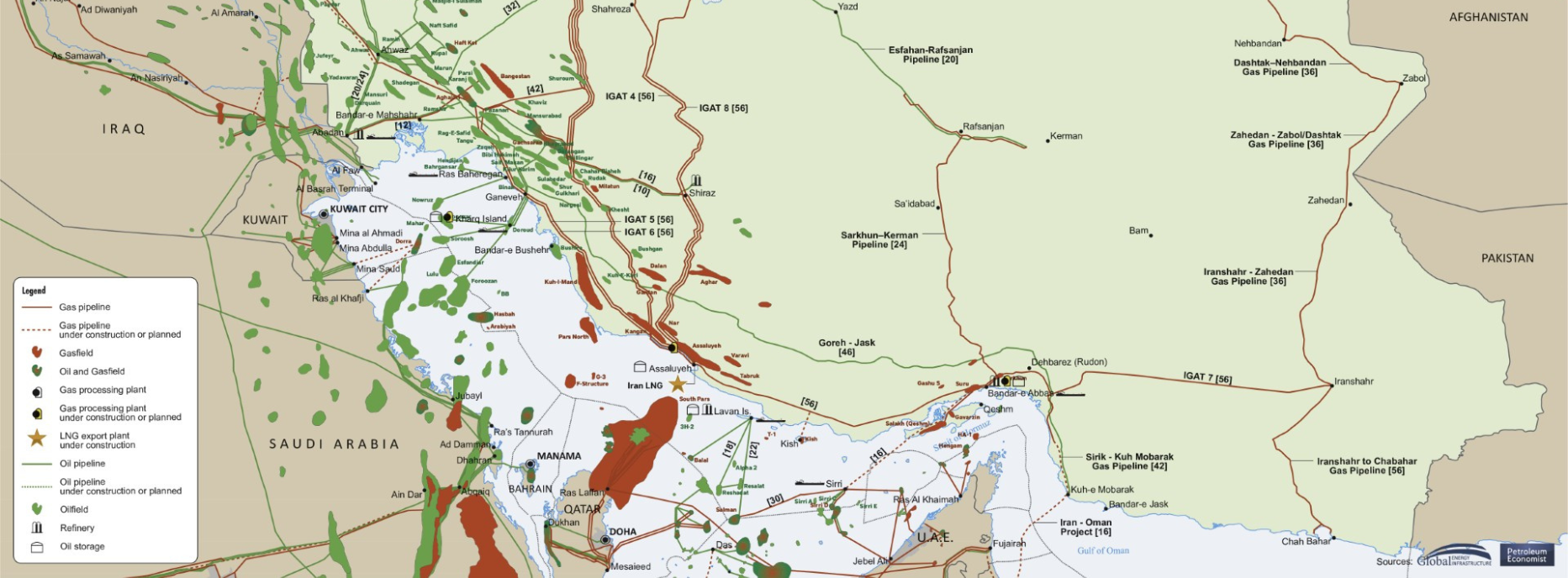

Iran’s explicit warning places critical hydrocarbon assets in Qatar, Saudi Arabia, and the United Arab Emirates under increased threat. The strike on the South Pars field, a colossal natural gas development shared with Qatar and a cornerstone of global LNG supply, signals a concerning shift in the conflict’s scope. Until recently, major energy infrastructure had largely been spared direct damage. Now, key facilities such as Saudi Arabia’s Abqaiq processing facility, the UAE’s Fujairah export hub, and Qatar’s extensive LNG infrastructure are on high alert, representing critical nodes in the global energy supply chain. Any sustained damage to these could trigger significant production losses and further tighten already constrained markets.

However, despite this heightened rhetoric and the expansion of the conflict’s geographic reach, the market’s reaction suggests a nuanced interpretation of the immediate threat. As of today, Brent Crude trades at $92.95 per barrel, reflecting a modest daily dip of 0.31%, with WTI Crude similarly at $89.45, down 0.25%. This contrasts sharply with the initial surge observed at the outset of the conflict. Our 14-day trend data further illustrates this: Brent has actually declined by 7% over the last two weeks, falling from $101.16 on April 1st to $94.09 on April 21st. This tells a compelling story of market participants initially pricing in a significant risk premium, only to pare back those gains as the conflict, while escalating in rhetoric, has not yet delivered widespread, sustained damage to major export infrastructure. The market appears to be in a holding pattern, carefully weighing the probability of direct attacks against existing supply resilience.

Strait of Hormuz Strain and Investor Outlook

Beyond the direct threat to facilities, the operational environment for energy flows through the Strait of Hormuz remains severely strained. This narrow waterway, through which approximately one-fifth of global oil and gas supply transits, has experienced significant disruptions, leading to production shut-ins across several Gulf producers. While Iranian state-linked vessels have continued to navigate the Strait under constrained conditions, and crude loadings at Kharg Island, Iran’s primary export hub, appear relatively steady, the underlying risk to shipping and insurance premiums persists.

Our reader intent data indicates that investors are keenly focused on the immediate future, with questions like “is WTI going up or down” dominating short-term queries, alongside longer-term predictions such as “what do you predict the price of oil per barrel will be by end of 2026?” For the near term, the current pricing of WTI at $89.45 reflects a market that is not yet fully convinced of an imminent, cataclysmic supply disruption. However, the foundational geopolitical risk means any actual incident could trigger a swift and aggressive price re-rating. For the end of 2026, the outlook remains highly dependent on both the trajectory of this regional conflict and the global supply-demand balance. Should significant infrastructure attacks materialize, a return to triple-digit crude prices is certainly plausible. Conversely, if the conflict remains contained to rhetoric and limited skirmishes, and global demand growth underwhelms, prices could face downward pressure from non-OPEC+ supply.

Navigating the Near-Term Data Landscape

For investors seeking to understand the immediate market dynamics and potential triggers, the next few weeks are packed with crucial data releases. The EIA Weekly Petroleum Status Report, scheduled for Wednesday, April 22nd, and again on April 29th and May 6th, will offer essential insights into U.S. crude oil, gasoline, and distillate inventories, providing a critical barometer of domestic supply and demand. These reports, alongside the API Weekly Crude Inventory data on April 28th and May 5th, will help investors gauge the tightness of the world’s largest consumer market. Any unexpected draws could amplify supply concerns stemming from the Gulf.

Beyond inventory data, the Baker Hughes Rig Count, due on Friday, April 24th and again on May 1st, will illuminate the ongoing production trends in North America, a key factor in global supply resilience. Perhaps the most significant forward-looking event, however, will be the EIA Short-Term Energy Outlook release on Saturday, May 2nd. This comprehensive report will provide updated projections for global oil supply, demand, and prices, offering an official assessment of how current geopolitical tensions are expected to impact the market over the coming months and year. Investors should pay close attention to any revisions in production forecasts for the Middle East, as well as demand projections, which could either exacerbate or mitigate the perceived supply risk from the Gulf.

Investment Implications and Dynamic Risk Assessment

The current environment demands a highly dynamic and granular approach to risk assessment for oil and gas investors. The market’s current pricing suggests a degree of complacency or a belief that the probability of direct, sustained attacks on core Gulf infrastructure remains low. However, the rhetoric from Iran clearly indicates a willingness to escalate. This creates an asymmetric risk profile: while prices have softened, the potential for a sudden, sharp upward correction in response to an actual event remains significant. Investors should consider the implications for companies with direct exposure to the Gulf region, particularly those operating critical infrastructure or involved in shipping through the Strait of Hormuz.

Portfolio strategies should account for this ongoing geopolitical premium, which may not always manifest in immediate price spikes but rather in increased volatility and the need for greater hedging. Companies with diversified asset bases outside the immediate conflict zone, or those focused on demand-side resilience (e.g., refining margins or downstream products), might offer relative stability. Ultimately, the focus has shifted from short-term price volatility to the longer-term risk of structural supply disruption. Investors must remain vigilant, monitoring not only the geopolitical headlines but also the real-time proprietary data flows to anticipate shifts in market sentiment and the potential for rapid re-pricing of global energy assets.