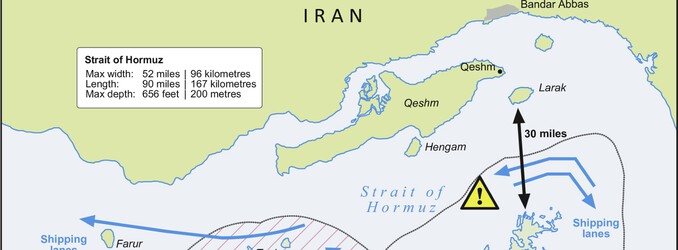

The strategic Strait of Hormuz, a critical chokepoint for approximately 20% of global oil and LNG flows, finds itself once again at the epicenter of geopolitical tensions. U.S. officials have signaled an intensified military campaign aimed at securing access to this vital waterway, directly targeting Iranian military assets. Treasury Secretary Scott Bessent’s statements underscore Washington’s resolve to weaken Iran’s capacity to disrupt shipping, a move President Donald Trump has supported with warnings of further action if transit is not restored. While the stated goal is long-term stability, the immediate implications for global energy markets are complex, requiring investors to carefully weigh geopolitical risks against prevailing market fundamentals.

Hormuz: Geopolitical Flashpoint Meets Market Reality

The escalating rhetoric and military posturing around the Strait of Hormuz certainly create a significant risk premium for global oil supply. However, a closer look at our proprietary market data reveals a nuanced picture that challenges the immediate “rising prices” narrative one might expect. As of today, Brent Crude trades at $92.29, marking a 1.02% decrease on the day, while WTI Crude mirrors this trend at $88.60, down 1.19%. This short-term pullback is not an isolated event; our 14-day Brent trend data shows a consistent decline, falling from $101.16 on April 1st to $94.09 by April 21st, representing a 7% drop over the past two weeks. This suggests that despite the intensifying military campaign and ongoing hostilities that have constrained tanker movements, the market is not currently pricing in a catastrophic, prolonged closure of the strait. Investors appear to be either discounting the immediate risk of severe disruption or are weighing other demand-side concerns that are currently offsetting geopolitical fears.

Strategic Imperatives: Securing Supply Routes for Long-Term Stability

The U.S. administration frames its actions as essential for securing longer-term stability in global energy markets. With Secretary Bessent emphasizing operations targeting Iranian assets near the waterway, the objective is clearly to neutralize Iran’s ability to threaten key infrastructure and shipping routes. The importance of this mission cannot be overstated. For Gulf producers, the Strait of Hormuz offers few viable alternatives, making any sustained disruption to tanker traffic a direct threat to their export capacity. Such a scenario would inevitably force production adjustments and accelerate inventory draws globally, amplifying price impacts significantly. While the current market reaction might seem subdued, the underlying risk of such a chokepoint being severely constrained means that a geopolitical risk premium remains embedded in crude benchmarks. The long-term stability sought by Washington is precisely what prevents wild price swings and ensures continuous, albeit sometimes fraught, global supply.

Navigating the Near-Term: Upcoming Data and Forward-Looking Analysis

For discerning investors, the intersection of geopolitical events and fundamental market data is paramount. Over the next two weeks, a series of key energy events will provide critical insights into supply-demand balances, potentially influencing market direction amidst the Hormuz tensions. Tomorrow, April 22nd, the EIA Weekly Petroleum Status Report will offer a fresh look at U.S. crude and product inventories. Any unexpected draws could quickly reintroduce upward price pressure, especially if the Hormuz situation remains volatile. This will be followed by the Baker Hughes Rig Count on April 24th, giving an indication of U.S. drilling activity, and another EIA report on April 29th. Looking further ahead, the EIA Short-Term Energy Outlook on May 2nd will provide updated forecasts that could significantly shift sentiment. These data points, combined with ongoing developments in the Strait, will be crucial in determining whether the recent price decline is merely a temporary correction or a sign of deeper market apprehension regarding demand. Investors should closely monitor these releases for early signals on how global supply and inventory levels are responding to the current environment.

Investor Sentiment: Decoding Price Signals and Data Reliability

Our proprietary reader intent data reveals that a primary concern for investors this week centers on price direction, with questions like “is WTI going up or down?” dominating our AI assistant’s queries. This reflects the market’s current uncertainty, particularly given the divergence between escalating geopolitical headlines and the recent downward trend in crude prices. While the immediate focus is on the Hormuz situation, our analysis suggests that short-term price movements, such as Brent’s decline from $101.16 to $92.29, are being influenced by a confluence of factors including profit-taking, broader macroeconomic headwinds, and a market consensus that a full, prolonged closure of the Strait is a tail-risk, not a baseline scenario. For those looking at the longer term, questions like “what do you predict the price of oil per barrel will be by end of 2026?” underscore the desire for clarity amidst volatility. Predicting exact future prices is challenging, but the structural tightness in global supply, coupled with potential demand recovery, could still push crude benchmarks higher over time, contingent on the resolution of geopolitical flashpoints and the absence of significant demand destruction. Investors are also keenly interested in the reliability of market information, asking about the data sources underpinning our analysis. We emphasize that our insights are drawn from real-time, first-party data pipelines, providing a unique and authoritative perspective on market movements and evolving investor sentiment.