The global energy landscape is perpetually navigating a complex web of geopolitical tensions and supply-demand dynamics. A recent pronouncement from India’s Oil Minister, Hardeep Puri, underscores this reality, revealing the nation’s proactive contingency plans should the vital Strait of Hormuz face disruption. This strategic foresight highlights the ever-present risks within key maritime chokepoints and prompts a deeper analysis of market resilience, India’s role as a refining powerhouse, and the broader implications for global energy investors.

India’s Strategic Resilience Amidst Geopolitical Volatility

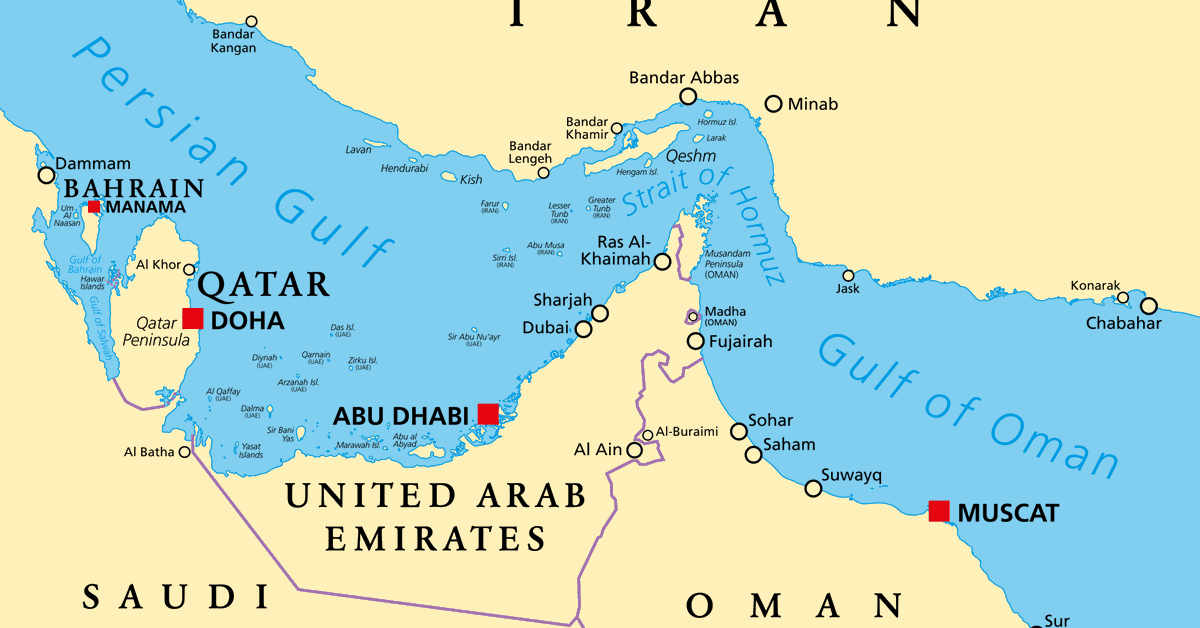

The Strait of Hormuz stands as an indispensable artery for global oil trade, facilitating the passage of approximately a quarter of the world’s crude shipments. For India, a rapidly growing energy consumer, this waterway is particularly critical, with 1.5 million barrels of its daily 5.5 million barrels of oil consumption transiting through the strait. The minister’s assurance that India possesses “enough stocks” of crude and refined products, alongside “diversified supplies” from alternate sources, provides a measure of confidence in the face of potential disruptions. This strategic diversification is not merely a reactive measure but a testament to long-term energy security planning, allowing the nation to pivot away from the Persian Gulf if necessary. While the immediate threat of a blockage remains speculative, these preparations serve as a potent reminder for investors to assess the supply chain vulnerabilities inherent in their portfolios and consider the resilience of nations with significant energy import needs.

Market Volatility and the Price Paradox

The specter of a Hormuz closure, with its potential to severely constrain global crude flows, naturally raises concerns about price spikes. However, the current market snapshot presents a fascinating paradox. As of today, Brent crude trades at $90.38, marking a significant 9.07% decline within the day, with prices ranging from $86.08 to $98.97. Similarly, WTI crude has fallen to $82.59, down 9.41%, trading between $78.97 and $90.34. This sharp daily downturn follows a broader trend over the past two weeks, where Brent has shed $20.91, dropping from $112.78 on March 30th to $91.87 on April 17th, representing an 18.5% decrease. This current market weakness, likely driven by broader demand concerns or profit-taking, starkly contrasts with the potential for an immediate and dramatic price surge if the Strait of Hormuz were indeed blocked. While India’s minister acknowledged that “prices are a concern” in such a scenario, the market’s present trajectory indicates that other fundamental forces are currently dictating short-term price action. For investors, this highlights the multifaceted nature of crude pricing, where geopolitical risks, while potent, can sometimes be overshadowed by prevailing supply-demand sentiment, creating a complex risk-reward profile.

India’s Refined Product Calculus and Global Implications

Beyond crude imports, India also plays a significant role in the global refined products market. The nation is a net exporter of petroleum products, with its refiners, including industry giants like Reliance Industries Ltd. and Nayara Energy, shipping an average of 1.3 million barrels per day so far this year. These exports reach diverse markets, from the United Arab Emirates and Singapore to the United States and Australia, underscoring India’s strategic importance in the downstream sector. Reliance and Nayara alone account for a dominant 82% of these shipments. Should a Hormuz disruption necessitate maintaining domestic stockpiles, India’s readiness to reduce these product exports would have a tangible ripple effect across international markets. Such a move would effectively create a secondary supply shock, reducing the availability of gasoline, diesel, and other essential fuels in importing nations. Investors should recognize that a disruption in the Strait would not only impact crude prices but also trigger a cascading effect on refined product markets globally, potentially bolstering margins for refiners in other regions and increasing costs for end-users worldwide.

Navigating Future Headwinds: OPEC+ and Investor Outlook

The ongoing market volatility, coupled with the ever-present geopolitical risks, places a heightened focus on upcoming energy events and the prevailing questions on investors’ minds. As the market grapples with a significant recent price decline, all eyes will be on the OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting on April 18th, followed by the Full Ministerial Meeting on April 19th. These gatherings are crucial for investors seeking clarity on the group’s production strategy. Will the recent 18.5% drop in Brent prices over the last 14 days prompt discussions about maintaining current quotas or even considering further cuts to stabilize the market? The decisions made at these meetings will directly influence global supply dynamics and, consequently, crude prices, especially when viewed through the lens of potential chokepoint disruptions.

Further informing market sentiment will be the weekly API and EIA crude inventory reports on April 21st/22nd and April 28th/29th, offering critical insights into U.S. supply and demand balances. Similarly, the Baker Hughes Rig Count on April 24th and May 1st will provide a forward-looking indicator of future production activity. These data points will be meticulously analyzed for signs of market tightness or surplus, influencing both short-term trading strategies and longer-term investment theses.

Amidst this backdrop, investors are actively seeking answers to pressing questions. Many are asking about the trajectory of crude prices, with a common query being: “What do you predict the price of oil per barrel will be by end of 2026?” This long-term outlook is fundamentally impacted by geopolitical flashpoints like the Strait of Hormuz and the collective response of major producers. Another frequent question, “What are OPEC+ current production quotas?”, underscores the critical role the alliance plays in managing global supply and mitigating volatility. India’s proactive measures, while commendable for domestic security, do not insulate the global market from the price implications of a Hormuz blockage or the subsequent ripple effects on OPEC+ policy. Investors must integrate geopolitical scenarios, upcoming policy decisions, and fundamental market data to construct a robust investment strategy in this dynamic and often unpredictable energy environment.