GORDON FELLER, Contributing Editor

Guyana and Suriname are close to one another in many ways, and both have good oil and gas prospects, going forward. But they face quite different near-term scenarios.

OVERVIEW

Fig. 1. The Stabroek Block, operated by ExxonMobil, contains Guyana’s oil finds and field developments. Image: U.S. Energy Information Administration.

For small South American countries, an abundance of natural resources has the potential to bring a bigger impact on the average citizen’s income. Guyana’s GDP per capita is rapidly increasing, due to oil production that began in 2019. The total output is on a rapid growth trajectory, with current daily production by mid-2025 reaching approximately 660,000 bbl. This is up from 391,000 bpd in 2023. ExxonMobil says production capacity is expected to reach 1.3 MMbpd by 2027 and 1.7 MMbpd by 2030. This growth is largely driven by the Stabroek Block, where multiple projects are under development, Fig. 1. Growth is fueled by projects like Liza Destiny, Liza Unity, Prosperity, and Yellowtail, with more projects in development.

On the flip side, Guyana has a low population density, with 90% of its approximately 779,004 inhabitants living on the narrow coastal plain, which only represents 10% of the country’s area. Coastal flooding, due to heavy rainfall, is a serious risk, affecting much of Guyana’s population and economic activity. As sea level continues to rise, more pain and dislocation will be hitting the national economy.

Guyana’s neighbor faces similar challenges. World Bank studies have found that Suriname “is one of the most vulnerable countries in the world to the impact of flooding. The country is prone to periodic flooding, due to heavy rainfall, especially when combined with spring tides.” Approximately 87% of Suriname’s population lives along the 386-km coastal plain, whereas the number jumps to approximately 67% percent in the capital city of Paramaribo. As in Guyana, flooding affects most of the population and an estimated 90% of human activities. Flooding is exacerbated by poor drainage in the relatively highly populated urban areas on the coast, such as in Paramaribo.

The situation is not quite what it appears. According to Pat Jelinek, EY Americas Oil & Gas and Chemicals Leader, twelve months ago the Suriname-Guyana basin’s outlook for hydrocarbons seemed quite straightforward: “deploy one FPSO annually, exceed nameplate capacity, and repeat.”

Jelinek explains here in detail that, despite robust project momentum, there are non-hydrocarbon factors that today could significantly influence the region, even before Suriname’s first oil production:

Local-content and infrastructure bottlenecks. Guyana and Suriname mandate local sourcing for goods, services and talent; however, current capacity remains constrained. Shorebase availability in Georgetown and Paramaribo is limited, “and key infrastructure—fabrication yards, heavy-lift docks, and warehouses—lags behind demand. Early dockside access, bonded warehousing, and local training partnerships are critical to avoiding cost overruns and delays experienced during Brazil’s early pre-salt period.”

Fig. 2. The first FID offshore Suriname was approved last October for Block 58 (TotalEnergies), targeting first oil by 2028. Image: TotalEnergies.

Gas monetization and power reliability. Large associated gas reserves exceeding 25 Tcf in Guyana’s Stabroek Block “have drawn regulatory attention aimed at minimizing flaring and lowering domestic electricity costs.” The ongoing 300-MW gas-to-energy project marks the region’s initial effort toward gas monetization. However, “midstream infrastructure, grid upgrades, and potential LNG facilities remain at preliminary planning stages. With Suriname recently concluding elections, and Guyana’s polls upoming, both governments are encouraging operators to develop gas-rich border blocks collaboratively.” There may be significant upside from gas commercialization projects, but development plans must include gas handling and LNG infrastructure from inception, and investors “should weigh potential benefits from gas commercialization against increased capital expenditure risks, if gas projects trail oil developments”.

Border-zone security premiums. Territorial disputes, particularly in the Essequibo region, “have increased maritime insurance premiums by 7% to 10% for operations near contested areas, significantly impacting shallow-water drilling rigs, seismic vessels, and associated crews.” Ongoing regional tensions could also affect final investment decisions on Trinidad and Tobago gas projects, emphasizing geopolitical risks. Exploration and development budgets “should include contingencies and flexible strategies to mitigate disruptions.”

OPTIMISM REMAINS

Despite the size and scope of these problems, EY’s Jelinek observes that optimism still persists. One reason is that “the first FID offshore Suriname was recently approved (October 2024) for Block 58, targeting first oil by 2028—demonstrating the basin’s capacity to convert discoveries into viable projects (Fig. 2).” As Jelinek notes, “a major operator’s sixth FPSO in Guyana maintains projected costs at $12.7 billion, due to standardized designs, despite global inflation.” Guyana’s Natural Resource Fund (https://petroleum.gov.gy/taxonomy/term/250), now exceeding $3 billion, actively finances infrastructure, free tertiary education, and diversification initiatives focused on fertilizer and specialty chemical manufacturing.

Fig. 3. Guyana’s oil production from several FPSOs averaged 625,000 bpd. Image: U.S. EIA.

Even optimistic timelines must account for the three big impediments on Jelinek’s list: “local-content limitations, gas monetization complexities, and geopolitical uncertainties”. Although Guyana’s exceptional GDP growth—highest globally for three consecutive years—is projected to moderate in 2025, stabilized oil production and Suriname’s economic recovery through promising hydrocarbon activity underpin regional stability. Investors adopting cautious strategies ahead of Guyana’s elections can effectively leverage the substantial opportunities available.

With a population of only ~623,000, Suriname is small, but it’s natural-resource rich, and upper-middle income. The economy is driven by its abundant natural resources, with mining accounting for nearly half of public sector revenue and gold representing more than three-quarters of total exports. This makes Suriname extremely vulnerable to external shocks.

INFRASTRUCTURE CHANGES

To better understand the changes now underway, we consulted with Luiz Hayum, WoodMac’s Principal Analyst in Upstream Research. He summarizes WoodMac’s assessment of the current situation in the following paragraphs.

Fig. 4. The Liza Destiny FPSO is the first of various floating vessels operating offshore Guyana. Image: SBM.

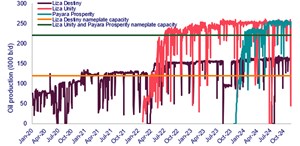

Production. Guyana’s 2024 oil production rate averaged 625,000 bpd, Fig. 3. ExxonMobil’s three operational FPSOs have consistently produced above nameplate capacity, sustaining a combined output close to 650,000 bpd. FPSO 1 (Liza field, Destiny FPSO, Fig. 4) and FPSO 2 (Liza field, Unity FPSO, Fig. 5) had extended production stoppages to connect to the gas-to-energy gas pipeline.

In 2025, additional topsides debottlenecking can increase production at FPSO 2 and FPSO 3 (Payara field, Prosperity FPSO, Fig. 6) from last year’s 250,000 bopd to 270,000 bopd, each, compared to a 220,000 bopd nameplate capacity. In April 2025, production for both FPSOs already surpassed 260,000 bopd.

WoodMac anticipates FPSO 4 (Yellowtail field, One Guyana FPSO) starting up in the second half of the year, with 2025 production averaging 740,000 bopd, Fig. 7. Guyana will surpass Colombia, becoming the fifth-largest producer in Latin America behind only Brazil, Mexico, Venezuela and Argentina.

Fig. 5. The Liza Unity FPSO has been online since February 2022. Image: SBM.

Exploration: Five operators are gearing up for exploration and appraisal campaigns in 2025— ExxonMobil, Petronas, Chevron, Shell and TotalEnergies. WoodMac hasn’t seen that many active operators in Guyana and Suriname since 2022. In the past five years, Suriname’s effective licensing policy of new acreage since 2020 will pay dividends. In 2025, for the first time since the Liza discovery, WoodMac expects to see more exploration and appraisal wells drilled in Suriname than in Guyana.

Activity in 2025 will be in stark contrast with a quiet 2024, when only ExxonMobil and Petronas spudded exploration wells. Petronas’ Fusaea in Suriname was the single, large oil discovery.

FID. WoodMac expects one more final investment decision in ExxonMobil’s Stabroek Block. The 150,000-bpd Hammerhead heavy oil project is in the advanced planning stage. However, as happened before, the high-GOR, light oil Longtail project could pass over it. In any case, ne 6 (Whiptail), sanctioned in 2024, was the last cluster of low-GOR, medium-light oil discoveries awaiting development. Moving forward, the supermajor will have to target either smaller, heavier oil or gasier opportunities.

The non-standard project designs required—when compared to FPSOs 1 to 6—can increase cost and lead times for decision-making and from FID to first oil. A heated deepwater market, with a tight supply chain, adds to the challenge. Hammerhead’s first oil is not anticipated before 2029, with a lead time approaching five years from FID to the first oil, an increase from the usual 3.5 years.

Fig. 6. The Prosperity FPSO is the third production vessel offshore Guyana and arrived at Payara field in April 2023. Image: ExxonMobil.

Gas. Reaching fiscal and commercial agreements in 2025 will be critical for Petronas and the Surinamese government to advance on gas and LNG projects in the region. Petronas aims to produce Suriname’s first gas in 2031; reaching a final agreement on gas fiscal terms for Block 52 is critical to maintaining the timeline. In Guyana, the project viability and role taken by the government and the upstream partners in a non-associated gas project in the Stabroek Block will be tested, with an initial alignment about gas terms also expected for this year.

During 2024, four appraisal wells confirmed gas potential in Guyana and Suriname, two exploration wells resulted in gas and condensate discoveries, and the Lau Lau discovery was successfully tested. In 2025, WoodMac expects gas appraisal work to continue, with at least two wells and well tests.

Analysts who pay close attention to these two countries, and to the larger region, are mindful of the fact that Guyana saw exceptional growth over the past two years, which was almost entirely driven by the booming oil sector. It’s positioned as one of the fastest-growing economies globally. According to data compiled by Lucas Marsden-Smedley Rodriguez, an associate director at FTI Consulting, “the country’s oil reserves are now the highest per capita in the world.” He notes that this continues to affect the country’s diversification efforts, “particularly into non-oil sectors—its future economic trajectory will depend heavily” on its ability to manage the windfall from oil while minimizing the risks of over-dependence on a single commodity.

Fig. 7. Sometime during second-half 2025, the One Guyana FPSO will go onstream at Yellowtail field. Image: SBM.

Rodriguez notes that Guyana’s Ministry of Natural Resources is now partnered with S&P Global to develop a gas monetization strategy for the country, set for completion this year. This, along with the Wales Development Zone, should drive industrial growth. The Wales Development Zone, where the gas-to-shore pipeline comes ashore, is meant to be the center of a whole new industrial strategy—power plants, downstream processing, etc.

The government is actively introducing new governance measures, including an Expert Advisory Team and Independent Petroleum Commission. As Rodriguez notes, “stricter local content regulations will require oil and gas companies to prioritize local suppliers, with penalties for non-compliance.”

The Ministry of Legal Affairs drafted a National Oil Incident and Emergency Response Bill, and on May 17, 2025, the National Assembly passed the “Oil Pollution Prevention, Preparedness, Response and Responsibility Bill 2025” (https://www.mola.gov.gy/post/oil-spill-bill-passed-in-the-national-assembly). It will address oil spills and environmental damage. It also contains new environmental regulations to ensure sustainable industry practices.

Fig. 8. This map clearly shows the land disputed by Venezuela and Guyana. Image: Bloomberg.

Stand-off with Venezuela. Guyana is in a strong position with active production, U.S. support, and a strong legal framework. And, as Rodriguez notes, an updated “Local Content Act” will “expand sector coverage and tighten enforcement, aiming to channel up to $350 million annually to local firms.” However, Rodriguez and other analysts worry that the growing Essequibo territorial dispute with Venezuela is intensifying, Fig. 8. Here is his summary of that situation: Guyana is strengthening its legal position. Venezuela elected officials and Neil Villamizar as governor in May, although the global community does not recognize their authority. Venezuela is also escalating its militarized stance. Washington and Beijing are both closely monitoring the situation.

Trump administration policies toward Venezuela are characterized by a complex list of factors, as itemized by Rodriguez: a split between hawks and pure deal-making engagement; the scaling back of foreign policy initiatives (FCPA, USAID etc.) coupled with sovereignty threats to Mexico, Panama, Greenland and Canada, as well Venezuela’s own economic woes after the Chevron license.” These open up a possible scenario in which Venezuela feels emboldened to take military action to control the oil-rich region. In sum, Rodriguez says he “still views this as unlikely, but it is one to monitor.”

Meanwhile, the situation in Suriname is still pre-production. The country lacks formal legislation but is building capacity through Staatsolie-led programs to prepare for major investments like Block 58. While its economy is not growing at the same pace as Guyana’s, Suriname has made significant progress in stabilizing its finances. The country’s successful completion of sovereign debt restructuring in January 2025, along with its accession to the World Bank’s International Development Association (IDA), is a clear signal of its commitment to financial stability. Suriname’s partnership with international institutions like the IMF and World Bank is crucial in providing the necessary funding and expertise.

Noting some real progress, Rodriguez points to the fact that Suriname “finalized a debt restructuring deal linked to future oil revenues, reducing debt-to-GDP, and cutting inflation to single digits, strengthening fiscal resilience. The government is restructuring state-owned companies, advancing anti-money laundering efforts, and amending sovereign fund laws to safeguard oil revenues, while introducing tax incentives under the Petroleum Act to boost the sector. May elections “marked a significant change to the electoral system,” moving away from a list system to “one man, one vote.”

The March 2025 election of Albert Ramdin, Suriname’s foreign minister, as the first Caribbean OAS Secretary General is, for Rodriguez, marking “a step toward greater regional visibility.” But it also highlights the OAS’s declining influence amidst rising bilateral power plays and great-power rivalry.

There are concerns about Staatsolie’s status as the country’s regulator for the oil and gas sector. Rodriguez is watching, since “there have been long-standing discussions about spinning off the regulatory role—but this is now a matter of some urgency—especially as Staatsolie moves to a JV with Total on oil and gas blocks.” To address this, Suriname President Chan Santokhi established a 30-member Strategic Group to create a sustainable oil revenue framework.

To navigate these dynamics, companies should prioritize conducting risk assessments, developing compliance programs, and investing in capacity-building initiatives. Robust systems for monitoring and reporting, investing in training and development programs for local workers, and engaging with local communities is key. By prioritizing transparency, accountability, and community engagement, businesses can build trust with local stakeholders and ensure the long-term sustainability of their operations.

LOCAL CONTENT

Local content legislation requires oil and gas firms to use local suppliers for a set of defined activities. Rodriguez notes that, “when clients ask us about Suriname and Guyana, it’s this which most interests them.”

Guyana’s local content requirements were put in place in 2021, and for Rodriguez, these stand out for being amongst the most ambitious in the region. “They are designed to ensure that the benefits of the oil and gas sector are widely shared amongst local businesses and Guyanese workers.” The local content framework is dynamic, with mechanisms for regular review and adjustment to promote sustainable national development while maintaining competitiveness. The Act’s first schedule lists 40 categories of required goods and services, with plans to expand it after private sector consultations. This requirement differs from one sector to another, in terms of the proportion of management and workforce that must be Guyanese. Generally, however, it requires that a company be 51%-owned by Guyanese shareholders.

Rodriguez puts the spotlight on ExxonMobil’s move to fund an extensive program of local supplier training and orientation to help put in place the necessary supply chain that will meet the government’s local content requirements. “The country’s V.P., Bharrat Jagdeo, warned last November that companies which are non-compliant with local content legislation will face consequences, as the government moves to close legal loopholes.”

All of the hydrocarbon industry’s players—oil and gas operators, service providers, suppliers and others—are, according to Rodriguez, “worried about this. IOCs and contractors must adjust procurement, restructure partnerships, and invest in local capacity to meet stricter targets and avoid penalties.” All upstream firms must submit annual Local Content Plans. Enforcement is now joint between the Local Content Secretariat and Guyana Revenue Authority. Penalties include fines up to G$50 million ($240,000) and loss of certification. Fronts and non-compliant foreign firms face legal risk.

But the plus side is that “local attitudes towards the sector may be improved, clearer expectations may boost investor confidence, and legal expansion may direct ~$350 million or more annually to local firms.”

FTI’s advice is that businesses should focus on developing strategic partnerships with local firms, investing in capacity-building programs, and implementing robust procurement processes to ensure compliance: “When engaging with local regulators, companies would be wise to balance public sector relations with selecting the best provider, as government-recommended partners may not always be the most suitable.” By conducting thorough assessments and prioritizing technical expertise, businesses can avoid penalties and build partnerships that drive long-term success.

In contrast, Suriname does not now have a dedicated local content law or fully formalized policy. Local content is, instead, addressed through clauses in production sharing agreements with oil companies. Such clauses stipulate that goods and services should be sourced locally, if they meet competitive price and quality standards. Rodriguez reports that “local business interests are lobbying for the introduction of a local content law, similar to that in Guyana, as they see advantages for their members in a more comprehensive requirement to use local businesses and local workers.”

Expected features include local procurement targets, training requirements, and supplier registry systems. Compliance depends on PSAs and Staatsolie’s informal oversight. Chevron and ExxonMobil, in partnership with Staatsolie, created a local supplier development program for local companies to develop skills and certifications. Firms are encouraged to register in the Staatsolie SRP and prioritize Surinamese suppliers. Formal audits and penalties will follow, once a legal framework is in place.

Rodriguez thinks that “the issue here is that many local businesses are still developing and may not meet IOCs’ technical and HSE standards. The absence of binding rules creates uncertainty and risks slow implementation without a dedicated, well-resourced enforcement body.” On the plus side, early entrants “can secure a foothold” ahead of Block 58 production growth; demand will rise for local services (e.g. logistics, catering, maintenance); capacity-building efforts (e.g. Blue Wave program) “and a flexible policy approach attract investors.”

Rodriguez concludes: “In the absence of a dedicated local content law, businesses should engage directly with local stakeholders, including government agencies and industry associations, to better understand evolving regulations and identify opportunities. By developing a deep understanding of the local market and building these relationships, companies can position themselves for success as early entrants, mitigating the risks of uncertainty.”

FUTURE PROSPECTS

To gain some perspective, it can be helpful to compare Guyana’s prospects with Suriname’s. For some insight, we consulted with Federico Torretta, a principal with Arthur D. Little’s Buenos Aires office. From a geological standpoint, Guyana has demonstrated stronger prospectivity and resource scale, with over 30 significant discoveries since 2015 and rapid progression from discovery to production. In Suriname, while discoveries have also been notable, they have been fewer in number and size, with commerciality assessments and development timelines proving more complex. The distinct profiles and strategic interests of the operators involved in the main asset developments—ExxonMobil in Guyana and TotalEnergies in Suriname—may also help explain the differing pace and approach in each country.

In terms of the development strategies adopted by each country, Torretta notes an important move: “Guyana opted for a fast-track development model, offering highly attractive fiscal terms and relying entirely on international oil companies for expertise and capital. In contrast, Suriname has adopted a more measured and conservative path, characterized by a higher projected government take and a more proactive—albeit still non-operating—role for its national oil company.”

Torretta’s assessment is that Guyana’s approach has “enabled rapid development, with production on track to reach 1.0 MMbpd by 2025. Suriname, on the other hand, signals a longer-term vision,” emphasizing broader economic transformation driven by the oil and gas sector.

Ultimately, the relative success of either strategy will hinge on the duration of the favorable medium-to-high-price window for hydrocarbons, and on what Torretta considers to be “the ability of each country to wisely manage the wealth generated by their nascent petroleum industries.”

Torretta’s overall conclusion is that “while Guyana has already emerged as a key player in both the U.S. and global oil and gas landscape, Suriname is steadily following in its footsteps, with first offshore production expected by 2028. Despite the undeniable similarities between the offshore production potentials of Guyana and Suriname—including adjacent geological structures—significant differences arise, both geologically and in the strategies each country has adopted to unlock their potential.”

BMI/Fitch concluded in June 2025 that Guyana will continue to “offer a low-cost and low-risk investment destination for upstream producers, with significant growth in oil production over the coming years.” Their current forecasts “expect crude oil and condensate production of 756,000 bpd in 2025, rising to 1.21 MMbpd by 2028 and 1.53 MMbpd in 2034, with risks to the upside from two other pre-FID projects currently under planning.” There are also long-term upside risks to gas production. Despite small gas production to date, the country is “increasingly planning to monetize its gas, reduce flaring and possibly set up an LNG project in the second half of the forecast period. ExxonMobil’s recently announced plans for the Longtail development would include substantial gas monetization” and provide long-term upside risks to BMI/Fitch’s gas forecast.

Related Articles

FROM THE ARCHIVE