Image: Shell’s Prelude FLNG

Floating liquefied natural gas (FLNG) terminals are gaining momentum on the global LNG market, with capacity expected to triple by 2030 according to research from Rystad Energy. Once hindered by technical and operational challenges, FLNG projects are now achieving utilization rates comparable to onshore terminals. With LNG demand rising alongside the growing viability of smaller gas fields, FLNG is emerging as a faster, more flexible and cost-effective solution capable of adapting to shifting market dynamics while unlocking previously stranded reserves.

Image: Rystad Energy

Rystad Energy estimates global FLNG capacity will reach 42 million tonnes per annum (MMtpa) by 2030, climbing to 55 Mtpa by 2035, almost four times the 14.1 Mtpa recorded in 2024. Terminals commissioned before 2024 achieved an average utilization rate of 86.5% in 2024 and 76% to date in 2025, figures comparable to global onshore LNG facilities.

“FLNG has come a long way in less than a decade. The only real roadblocks were early teething issues that come with any new technology, as seen with projects like Shell’s Prelude, which faced cost overruns and unstable output. But since then, the industry has matured significantly, including Prelude itself. Utilization rates are improving, the technology is proving reliable across a range of environments, and the economics are starting to make more sense. From navigating permitting challenges in Canada to unlocking remote offshore reserves in Africa and Asia, FLNG is finally going mainstream,” said Kaushal Ramesh, Vice President, Gas & LNG Research, Rystad Energy.

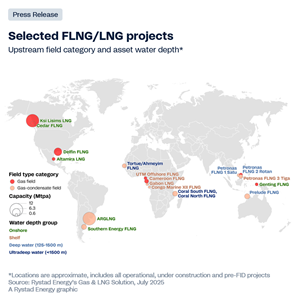

Without a prior blueprint to follow, early FLNG projects, such as Shell’s Prelude, built in South Korea by the Technip–Samsung consortium, became a negative demonstration of FLNG’s early limitations. Costs ballooned to $2,114 per tonne for liquefaction alone. However, as the industry gained operational and construction experience, capital expenditure per tonne has declined significantly, bringing costs in line with onshore LNG projects.

Proposed developments along the US Gulf Coast now average around $1,054 per tonne. Delfin FLNG, a proposed project in the US, sits just above that average at $1,134 per tonne, while Coral South FLNG in Mozambique, which is similar in scale, reports a comparable liquefaction cost of $1,062 per tonne. However, we note that project concepts are not entirely comparable. Some are complex integrated producers with upstream components as part of the LNG facilities, while others simply liquefy pipeline-spec gas.

In parallel, FLNG developers are increasingly turning to vessel conversions as a cost-efficient alternative to newbuild facilities. Projects such as Tortue/Ahmeyim FLNG, Cameroon FLNG and Southern Energy’s FLNG MK II have achieved notably lower capex levels of $640, $500 and $630 per tonne, respectively, by repurposing Moss-type LNG carriers. These conversions benefit from the vessels’ modular spherical tank design, which allows for simpler integration of prefabricated liquefaction modules. With several Moss-type LNG tankers expected to retire in the coming years, more could be repurposed, expanding the pipeline of lower-cost FLNG solutions.

FLNG vessels are also proving their operational flexibility across diverse environments, from deepwater to ultra-deepwater fields and even onshore supply. Should certain projects stall, their vessel could be relocated or sold, demonstrating the inherent mobility and adaptability of FLNG assets.

In the current energy environment, where markets remain tight but face the risk of oversupply, speed to first production is critical. Extended construction timelines delay revenue generation and expose projects to a higher risk of cost overruns. Rystad Energy data also shows that FLNG units can be delivered significantly faster than onshore liquefaction facilities, enabling quicker final investment decisions and more agile execution. On average, newbuild FLNG projects are completed in approximately three years, compared to about 4.5 years (capacity-weighted) for operational onshore plants. For FLNG vessels currently under construction, the average projected build time is even lower at 2.85 years. This accelerating timeline is a key factor in the growing preference for FLNG, as developers seek to minimize exposure and accelerate returns.