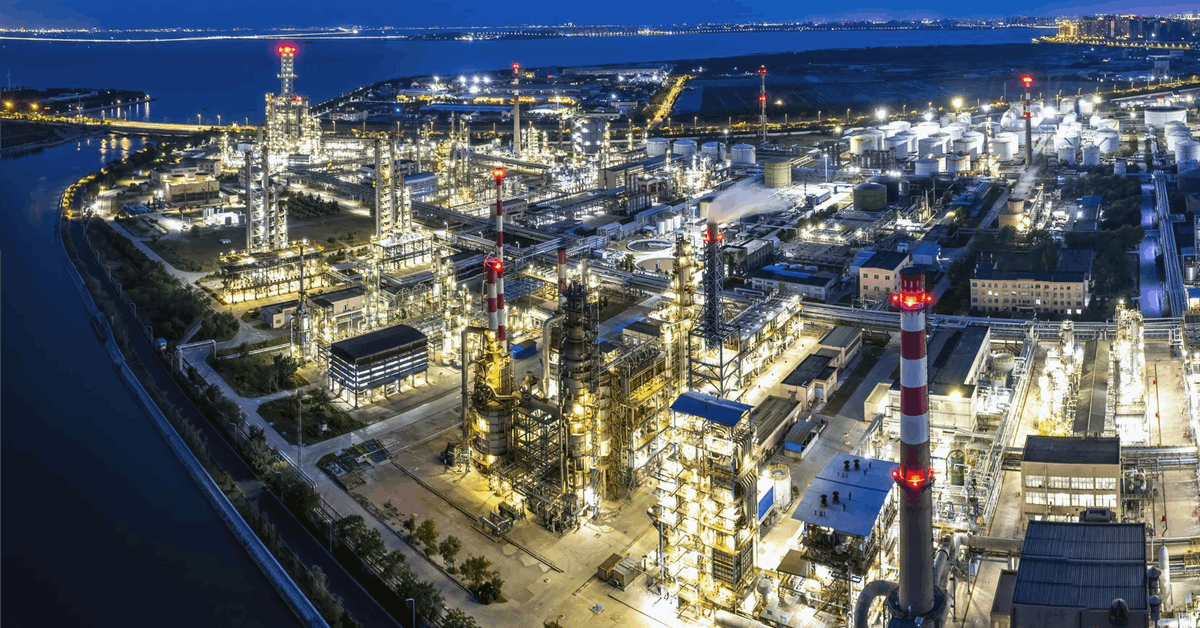

China’s colossal petrochemical and oil refining sector is on the cusp of a transformative overhaul, with Beijing poised to implement sweeping changes designed to curb persistent overcapacity and steer the industry towards higher-value production. This strategic pivot, expected to roll out within the next month, carries significant implications for global energy markets, crude demand, and the investment landscape for integrated oil and gas players. As a senior analyst, we view this as a critical development that warrants close scrutiny, impacting everything from refining margins to the competitive dynamics in specialty chemicals.

China’s Strategic Pivot in Petrochemicals

The impending policy shift by the Chinese government directly addresses the long-standing issue of oversupply in lower-value bulk petrochemicals and transport fuels. Facing rapid electrification that is eroding traditional gasoline and diesel demand, and grappling with broader deflationary pressures, Beijing is compelling its industrial giants to adapt. The proposed measures are comprehensive: approximately 40 percent of the country’s petrochemical facilities, those over 20 years old, will be mandated to undergo retrofitting to enhance yields and efficiency. More significantly, investment will be actively redirected towards advanced materials. This includes a strategic emphasis on specialty fine chemicals critical for emerging technologies such as artificial intelligence, robotics, semiconductors, biomedical devices, batteries, and renewable energy, rather than continuing to flood markets with already oversupplied bulk commodities.

Furthermore, the plan targets the rationalization of the refining sector itself. Smaller oil refiners, specifically those with less than 2 million tons of annual capacity, face potential closure. This is a direct response to the estimated 60 million tons of excess capacity in the transport fuels sector, which has driven down operating rates and pressured profit margins. The broader objective is to cap China’s total refining capacity at one billion tons annually by 2025, a clear signal that the era of unchecked expansion is over. This top-down rationalization is not merely an economic adjustment; it’s a strategic reorientation aimed at enhancing industrial competitiveness and achieving technological self-sufficiency in key sectors.

Market Headwinds Reinforce Beijing’s Urgency

The timing of China’s proposed industrial reforms is particularly poignant given the recent volatility in global crude markets. As of today, Brent crude trades at $90.38 per barrel, marking a significant daily decline of 9.07% within a range of $86.08 to $98.97. Similarly, WTI crude is priced at $82.59, down 9.41% for the day. This downward pressure extends beyond a single trading session; our proprietary data indicates Brent has plunged by $20.91, or 18.5%, from $112.78 on March 30th to $91.87 just yesterday, April 17th. This rapid deterioration in crude prices, while potentially beneficial for input costs, underscores the broader challenges faced by refiners globally, especially those reliant on lower-value outputs. The retail gasoline price, currently at $2.93 per gallon, down 5.18% today, further highlights the squeezed margins in the downstream sector.

Such market conditions create an imperative for efficiency and value creation. The substantial drops in crude prices, combined with softening demand for traditional transport fuels due to electrification, put immense pressure on refining profitability. Beijing’s push to curb overcapacity and pivot to specialty chemicals is thus not just a long-term strategic move but also an immediate response to difficult market realities. By eliminating inefficient capacity and focusing on high-margin products, China aims to insulate its industry from the vagaries of commodity price swings and evolving demand patterns, thereby improving the overall health and resilience of its energy sector.

The Ethylene Dilemma and Future Investment Directives

While the immediate overhaul targets older facilities and smaller refiners, an emerging concern that reflects China’s broader overcapacity challenge is the looming glut in ethylene. This crucial ingredient for textiles, rubber, and plastics has seen a decade of overzealous investment, with new plants still scheduled to come online through 2028. Industry insiders suggest that new permits for ethylene facilities could face curbs as early as 2026, a priority issue slated for the upcoming Five Year Plan, expected to be unveiled in March. This situation exemplifies the challenge of balancing industrial growth with market realities, as unabsorbed domestic supply risks becoming yet another Chinese export that could draw accusations of dumping from global trade partners.

For investors, this signals a clear divergence in strategic focus. While bulk chemical producers face significant headwinds, the new investment regime will actively favor chemicals used in high-growth, technology-driven sectors. This includes materials for artificial intelligence, robotics, semiconductors, biomedical devices, batteries, and renewable energy infrastructure. Companies positioned in these areas, or those with the agility to retool their operations, stand to benefit from preferential policies and redirected capital. The message is clear: the future of China’s petrochemical sector lies not in volume, but in value and technological sophistication.

Navigating the Landscape: Investor Outlook and Upcoming Catalysts

Investors are keenly watching for how these structural changes in China will impact global oil demand and pricing. Many are asking about the trajectory of oil prices, with questions like “what do you predict the price of oil per barrel will be by end of 2026?” echoing through the market. China’s move to rationalize its refining capacity, particularly the closure of smaller, less efficient plants, could subtly reduce crude import demand in the long term, potentially easing some pressure on global supply. However, the shift towards petrochemical feedstocks for advanced materials might offset some of this reduction, creating a nuanced demand picture.

In the near term, several key events will shape the energy market and influence the backdrop against which China’s reforms unfold. This weekend, the OPEC+ Joint Ministerial Monitoring Committee (JMMC) meets on April 18th, followed by the full OPEC+ Ministerial Meeting on April 19th. These gatherings are critical for understanding future crude production quotas and their potential impact on global supply. Additionally, the market will closely monitor weekly inventory data, with the API Weekly Crude Inventory reports due on April 21st and 28th, and the EIA Weekly Petroleum Status Reports on April 22nd and 29th. These data points offer vital insights into real-time supply and demand dynamics. The Baker Hughes Rig Count, scheduled for April 24th and May 1st, will also provide clues about future production trends. For investors in integrated energy companies and refiners, understanding these global catalysts alongside China’s domestic policy shifts will be paramount for navigating the evolving investment landscape.