The global energy landscape is undergoing a profound transformation, with the electric vehicle (EV) sector emerging as a formidable challenger to traditional internal combustion engine (ICE) dominance. A recent announcement from BYD, a leading EV manufacturer, regarding its ambitious flash charging network expansion into South Africa, underscores the accelerating pace of this transition. This move, mirroring similar plans for Europe, signals a concerted effort to dismantle range anxiety and charging bottlenecks, directly impacting long-term demand projections for crude oil and refined products. For savvy oil and gas investors, understanding these strategic shifts is paramount to navigating an increasingly complex market and identifying future value drivers.

BYD’s Aggressive EV Infrastructure Play in Emerging Markets

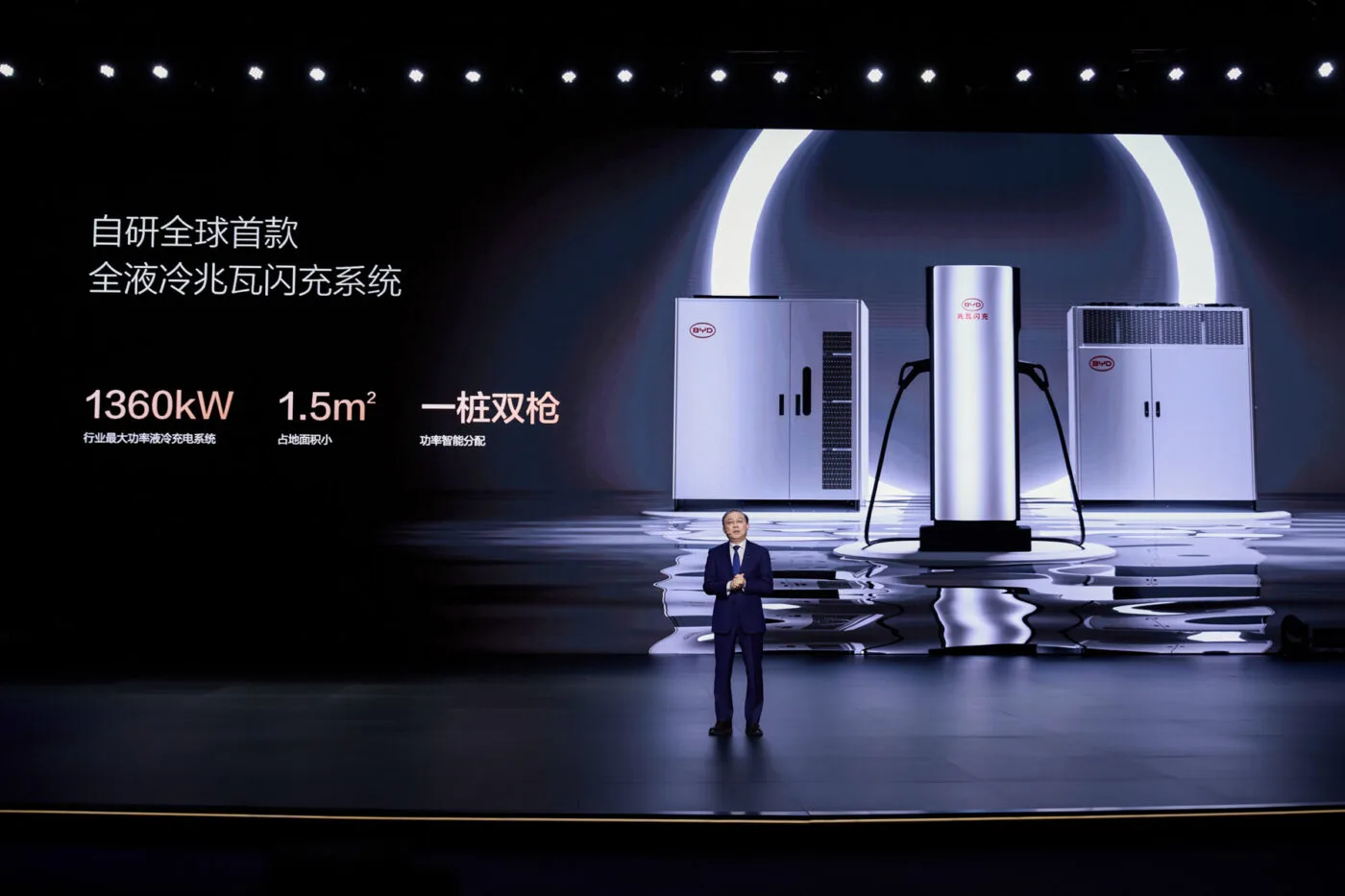

BYD’s commitment to deploying 1,000 kW flash charging stations in South Africa, with initial installations slated for April or May 2026, marks a significant milestone in EV adoption beyond established Western markets. This high-power charging technology, capable of adding 400 kilometres of range in just five minutes (based on the CLTC cycle, enabling a 100 kWh battery to go from 7% to over 50% in the same timeframe), directly addresses one of the primary consumer concerns for EV ownership: charging speed and accessibility. The company plans to rapidly expand its South African dealer network, aiming for 200 to 300 flash charging stations by the end of 2027, with an ultimate goal of 100% national coverage, extending beyond major cities to smaller towns and communities. This strategic saturation of charging infrastructure, powered by a combination of mains electricity and solar energy, highlights a proactive approach to market penetration and lays a robust foundation for future EV sales, inevitably chipping away at gasoline demand.

Parallel to its South African ambitions, BYD is also setting its sights on Europe, with plans for an initial network of several hundred charging stations in 2026, targeting 200 to 300 by the end of the second quarter. While the European solution might feature a single charging cable for 1,000 kW compared to China’s two-cable setup, the underlying objective remains the same: to rapidly build out a high-speed charging ecosystem that makes EV ownership increasingly practical and appealing. This multi-continent infrastructure push by a major EV player signals a powerful trend that oil and gas investors cannot afford to ignore, as it directly influences the pace of fuel switching globally.

Market Volatility Meets Long-Term Demand Headwinds

The accelerating build-out of EV infrastructure occurs against a backdrop of significant volatility in the traditional oil markets. As of today, Brent Crude trades at $90.38, reflecting a substantial 9.07% decline within the day, having ranged from $86.08 to $98.97. Similarly, WTI Crude stands at $82.59, down 9.41%, with its daily range spanning $78.97 to $90.34. Gasoline prices have also seen a notable dip, currently at $2.93, a 5.18% decrease. This recent downturn follows a broader trend, with Brent having fallen by $22.4, or 19.9%, from $112.78 on March 30th to its current level. While short-term supply-demand imbalances and geopolitical factors often drive such sharp movements, the long-term trajectory of oil demand is increasingly influenced by structural shifts like the widespread adoption of EVs.

Our proprietary reader intent data indicates that investors are keenly focused on the future of oil prices, with questions like “what do you predict the price of oil per barrel will be by end of 2026?” frequently surfacing. While specific price predictions remain challenging, the aggressive EV expansion by players like BYD introduces a powerful deflationary force on future demand. Every flash charging station installed, every EV sold, represents a direct reduction in the reliance on gasoline and diesel. This fundamental shift underscores the need for oil and gas companies to adapt, diversify, and focus on capital discipline, as the era of continually expanding demand may be drawing to a close, particularly in the light vehicle segment.

Strategic Market Entry and Localized Solutions

BYD’s approach to market entry in South Africa offers valuable insights into how global EV players are navigating new territories. Despite significant investment in charging infrastructure, the company currently has no plans for local vehicle or battery manufacturing. As Stella Li noted, manufacturing investments are typically reserved for markets where BYD has a substantial existing presence. This strategy allows the company to rapidly establish a consumer base and build brand loyalty through an accessible charging network before committing to the capital-intensive process of local production. This “infrastructure-first” approach is particularly relevant for emerging markets where grid stability and energy access can be inconsistent.

The decision to power flash chargers with a combination of mains electricity and solar energy, including an agreement with South African electricity supplier Eskom, is a pragmatic solution to potential grid limitations. This hybrid model enables BYD to deploy infrastructure even in areas with insufficient grid capacity, accelerating the rollout and ensuring broader coverage. For oil and gas investors, this highlights the intertwined nature of the energy transition, where EV adoption is not just about vehicles but also about the underlying power generation and distribution infrastructure. Investments in renewable energy and grid modernization, particularly in regions like Africa, are increasingly becoming critical enablers for the EV revolution, suggesting new avenues for capital deployment within the broader energy sector.

Navigating Upcoming Events Amidst a Shifting Paradigm

For oil and gas investors, the coming weeks are packed with events that will undoubtedly influence short-term market dynamics, even as the long-term energy transition accelerates. The OPEC+ JMMC Meeting on April 19th and the subsequent OPEC+ Ministerial Meeting on April 20th are critical for understanding immediate supply-side decisions and production quotas, which our readers are actively inquiring about. These meetings often trigger significant price movements, directly impacting the profitability of exploration and production companies.

Further insights into market fundamentals will come from the API Weekly Crude Inventory reports on April 21st and 28th, followed by the EIA Weekly Petroleum Status Reports on April 22nd and 29th. These data releases provide vital statistics on U.S. crude, gasoline, and distillate inventories, offering a snapshot of current supply and demand balances. The Baker Hughes Rig Count on April 24th and May 1st will also offer a forward-looking indicator of drilling activity and potential future production. While these events remain crucial for short-to-medium-term trading strategies, investors must simultaneously integrate the implications of aggressive EV expansion into their long-term outlook. The rapid deployment of flash charging networks by companies like BYD represents a structural shift that will incrementally, but inexorably, redefine the demand curve for fossil fuels, making the transition a central theme for all energy investment decisions going forward.