A new and unusually early tropical cyclone, Fina, is rapidly developing off Australia’s Northern Territory coast, posing a significant and immediate threat to key energy infrastructure. Expected to intensify to a Category Two system before making landfall potentially as early as Friday or Saturday, Fina introduces an unexpected supply-side risk to global energy markets already grappling with volatility. For investors, this event warrants close monitoring, as it could disrupt crucial liquefied natural gas (LNG) export operations from Australia, a top global supplier. Our analysis leverages OilMarketCap’s proprietary market data and reader intent signals to dissect the potential impact on crude, gas, and refined product prices, offering forward-looking insights into how this weather event intertwines with broader market fundamentals and upcoming energy catalysts.

Cyclone Fina: An Early-Season Threat to Australian LNG Exports

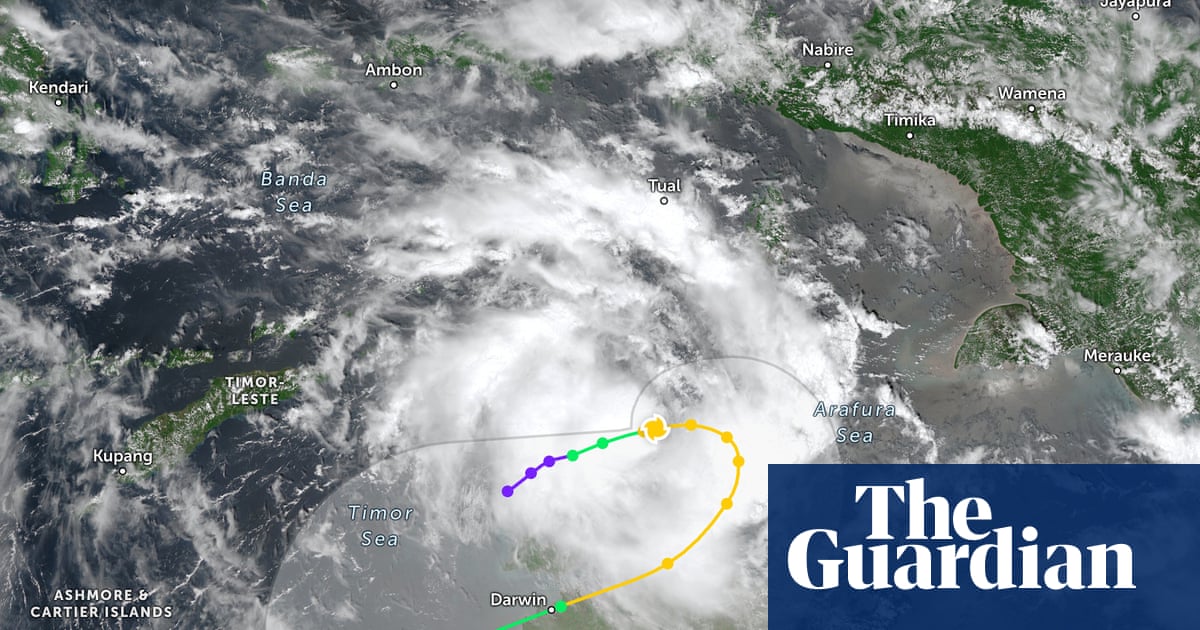

Tropical Cyclone Fina, currently a Category One system positioned approximately 370 kilometers north-east of Darwin, is on a trajectory that could see it cross the Northern Territory coast by Friday or Saturday. This timeline is remarkably early, with meteorologists noting it could equal the earliest cyclone landfall in Australia’s recorded history, challenging records set in 1973 and 2013. The Bureau of Meteorology anticipates Fina will intensify to a Category Two system before impact, bringing with it the potential for significant wind gusts and rainfall. While small in size, its compact nature suggests it could spin up rapidly, leading to swift intensification.

The immediate concern for energy markets stems from Fina’s proximity to Darwin, a critical hub for Australia’s vast LNG export industry. Major facilities in the region, including the Darwin LNG plant and numerous upstream gas fields that feed larger export terminals, are vulnerable to such weather events. Historically, cyclones like Marcus in 2018, which made landfall near Darwin as a Category Two system with 130 km/h wind gusts, caused widespread power outages and infrastructure damage. Any disruption to production or export operations, even temporary, would reverberate through the tight global LNG market, potentially creating an immediate supply squeeze and upward price pressure, particularly as the northern hemisphere heads towards peak demand seasons.

Market Volatility Meets Supply Risk: Investor Implications

The emergence of Cyclone Fina comes at a precarious time for energy markets, which have seen considerable price swings recently. As of today, Brent crude trades at $90.17 per barrel, reflecting a sharp decline of 9.28% within the trading day, with prices ranging from $86.08 to $98.97. Similarly, WTI crude has fallen by 9.83% to $82.21, after trading between $78.97 and $90.34. Gasoline prices have also dipped, currently at $2.92, down 5.5% today. This daily downturn extends a broader bearish trend for crude, with Brent having shed over $22 per barrel since March 27th, dropping from $112.57 to $90.17.

Against this backdrop of softening prices, the potential for an LNG supply disruption from Australia introduces an immediate and unpredictable bullish catalyst. While the current market reaction to crude prices suggests broader demand concerns or macroeconomic pressures, a tangible threat to global gas supplies could quickly shift investor focus. Many OilMarketCap readers are actively querying about the future trajectory of oil prices, with common questions including predictions for the price of oil per barrel by the end of 2026. Events like Fina underscore the difficulty in making such long-term forecasts, as unforeseen supply shocks can dramatically alter short-to-medium term market dynamics, adding a significant risk premium to energy commodities.

Climate Change: A Recurring Threat to Energy Infrastructure

Beyond the immediate impact of Cyclone Fina, this early-season event serves as a stark reminder of the increasing long-term risks posed by climate change to global energy infrastructure. Experts indicate that while a warming climate may lead to fewer tropical cyclones globally, those that do form are expected to be more severe, with a higher proportion intensifying to Category Four or Five. This trend of increased intensity and rapid intensification is already being observed, with above-average sea surface temperatures in the Timor Sea – well above the 26.5°C threshold required for cyclone formation – providing ample fuel for storms like Fina.

For investors, this climatic shift translates into heightened operational risks and increased capital expenditure for coastal energy assets, particularly LNG export terminals and offshore production platforms. The need for more robust infrastructure, enhanced disaster preparedness, and potentially higher insurance premiums becomes a critical factor in valuing these long-life assets. Understanding and integrating these evolving climate risks into investment decisions is no longer a peripheral concern but a central pillar of long-term portfolio resilience in the energy sector.

Navigating Upcoming Catalysts and Supply-Side Decisions

The market’s immediate attention, while momentarily diverted by Cyclone Fina, will soon return to a series of critical upcoming events that will further shape energy prices. Today, Friday, April 17th, marks the OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting, followed by the full Ministerial meeting tomorrow. These gatherings are paramount for investors, particularly those asking about current OPEC+ production quotas, as any adjustments to supply policy could significantly amplify or dampen the impact of potential Australian LNG disruptions.

Next week brings the API Weekly Crude Inventory report on Tuesday, April 21st, followed by the EIA Weekly Petroleum Status Report on Wednesday, April 22nd. These reports will provide crucial insights into U.S. supply and demand balances, offering a snapshot of market fundamentals. A surprise draw in inventories, coinciding with potential LNG export disruptions, could trigger a more pronounced upward price reaction. Furthermore, the Baker Hughes Rig Count on April 24th and May 1st will offer forward-looking indicators of future production capacity. Investors must remain agile, interpreting Fina’s localized supply threat within the broader context of OPEC+ decisions and these regular inventory and activity reports, which collectively paint a dynamic picture of global energy supply and demand.