Alaskan Offshore Lease Sale: A Bellwether for Investor Appetite Amidst Shifting Market Dynamics

The recent federal oil and gas lease sale in Alaska’s Cook Inlet, which saw a resounding zero bids for approximately 1 million acres, delivers a stark message to investors. Far from signaling a lack of potential resources, this outcome highlights a critical shift in how oil and gas companies are evaluating frontier exploration. While policy initiatives aim to expand domestic production, market economics, high operational costs, and evolving investor priorities are clearly dictating where capital flows. For seasoned oil and gas investors, this event isn’t just a footnote; it’s a significant indicator of the current risk-reward calculus in an increasingly complex energy landscape.

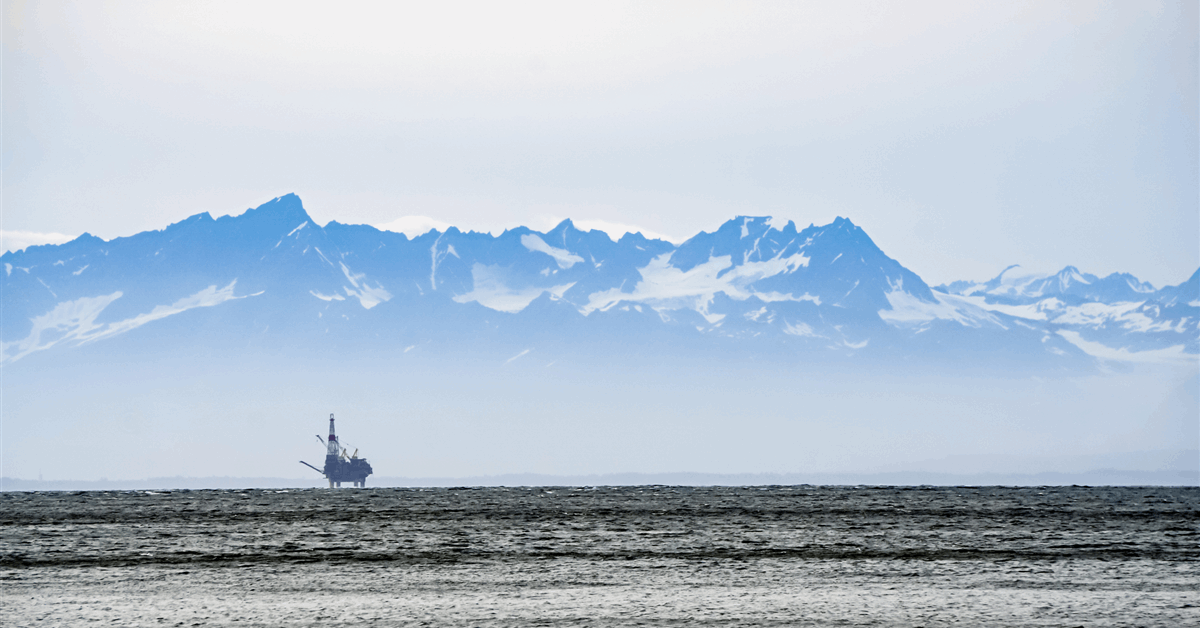

The High Cost of Arctic Ambition: Why Cook Inlet Fell Flat

The Trump administration’s mandate to open up more federal lands and waters for energy development, including areas like Cook Inlet off Alaska’s south-central coast, was met with an undeniable lack of industry enthusiasm. The absence of bids for a million acres underscores the formidable challenges inherent in Alaskan exploration. Operating in the Arctic and sub-Arctic regions demands significant capital investment for specialized equipment, robust infrastructure, and enhanced safety protocols to contend with extreme weather conditions, remote logistics, and stringent environmental regulations. These factors drive up the per-barrel cost of discovery and development considerably compared to more accessible, established basins. Furthermore, Alaska’s oil production has been declining for decades, adding another layer of perceived risk regarding the economic viability of new, unproven plays. The Bureau of Ocean Energy Management may reiterate its commitment to a “regular, predictable federal leasing schedule” to achieve “American Energy Dominance,” but the market’s response demonstrates that economic realities currently outweigh political directives.

Market Realities: Price Stability Meets Capital Discipline

The lack of interest in Cook Inlet must be viewed through the lens of current market conditions and prevailing investor sentiment regarding capital allocation. As of today, Brent crude trades at $93.04 per barrel, reflecting a slight dip of 0.21% within a daily range of $92.57 to $94.21. Similarly, WTI crude stands at $89.43, down 0.27%, with its day range between $88.76 and $90.71. While these prices remain robust compared to historical averages, the 14-day trend for Brent shows a decline from $101.16 on April 1st to $94.09 on April 21st, representing a significant $7.07 (or 7%) drop. This recent softening, even from elevated levels, reinforces a cautious approach among producers. Companies are prioritizing capital discipline, focusing on shareholder returns, and allocating investment to lower-cost, quicker-to-market projects with established infrastructure – often in regions like the Permian Basin – rather than committing to high-cost, long-lead-time frontier exploration. The current price environment, while supportive of existing production, isn’t quite high enough to incentivize the substantial upfront investment and elevated risk profile associated with challenging plays like Cook Inlet.

Investor Focus: Navigating Price Trajectories and Regional Performance

Our first-party reader intent data reveals that investors are keenly focused on understanding future price movements and evaluating company performance in the current environment. Common questions revolve around the trajectory of WTI prices and predictions for the price of oil per barrel by the end of 2026. This intense focus on forward price outlook directly impacts appetite for long-term, high-risk projects. The Cook Inlet outcome suggests that, even with favorable policy, the smart money is not chasing every potential resource. Instead, it’s seeking predictability and lower execution risk. For example, some investors are specifically asking about the performance outlook for companies like Repsol in April 2026, indicating a preference for evaluating established players and their existing asset portfolios rather than speculative new ventures in difficult operating environments. The absence of bids signals that, for now, the perceived risk and cost of Alaskan offshore exploration outweigh the potential reward, even at today’s healthy crude prices.

Upcoming Catalysts and the Future of Energy Investment

Looking ahead, several upcoming energy events will provide crucial data points that could further shape investment decisions and the long-term outlook for challenging regions like Alaska. The EIA Weekly Petroleum Status Reports on April 29th and May 6th, alongside the Baker Hughes Rig Counts on April 24th and May 1st, will offer fresh insights into domestic supply, demand, and drilling activity. If these reports continue to show robust production growth from lower-cost shale plays, it will further diminish the relative attractiveness of frontier areas. Moreover, the EIA Short-Term Energy Outlook on May 2nd will provide updated macro forecasts for supply, demand, and prices, which could either bolster or dampen the case for long-term, capital-intensive projects. The Cook Inlet lease sale failure serves as a real-world stress test for the “American Energy Dominance” agenda. It demonstrates that while political will can open doors, it is ultimately market forces, investor capital discipline, and economic viability that determine whether those doors are walked through. For investors, monitoring these upcoming data releases will be critical to understanding how the industry continues to navigate the balance between resource potential and financial prudence.