Oil Plunges: Iran Talks Outweigh Hormuz Concerns

The energy market experienced a dramatic shift recently, as crude prices saw one of their most significant intraday swings on record. This volatility was primarily triggered by comments from President Donald Trump suggesting that discussions to de-escalate the conflict with Iran were underway, despite immediate denials from Tehran. The prospect of even a glimmer of resolution sent a ripple through futures contracts, temporarily overshadowing the acute physical supply risks that have dominated headlines. For investors, this whipsaw action underscores a market highly sensitive to geopolitical rhetoric, often at odds with persistent on-the-ground realities, demanding a nuanced approach to navigating current and future positions.

The Volatility Paradox: De-escalation Hopes vs. Persistent Risk

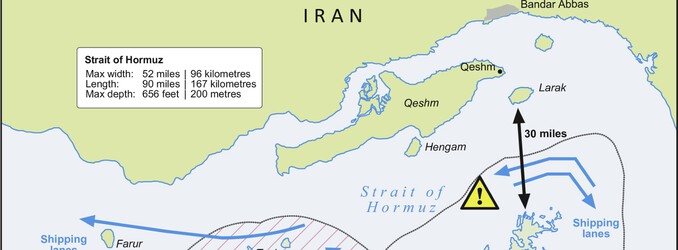

Today’s market snapshot reveals Brent Crude trading at $92.54, down 0.75% within a day range of $91.39 to $94.21, while WTI Crude stands at $88.78, reflecting a 0.99% decline from its range of $87.64 to $90.71. These figures represent a partial recovery and subsequent decline from a much sharper dip, where Brent initially plummeted as much as 14% to near $96 per barrel following initial de-escalation signals. This extreme intraday movement illustrates the market’s hyper-sensitivity to any hint of geopolitical resolution, even if unsubstantiated. While the immediate price action pointed downward, it’s crucial for investors to remember the underlying supply landscape. The Strait of Hormuz remains severely constrained, disrupting approximately 20% of global oil and LNG flows, a situation the International Energy Agency has characterized as one of the most significant supply disruptions in history. Despite the recent price plunge, tanker traffic has not resumed normal operations, with shipowners still reluctant to transit due to ongoing security concerns. This creates a paradox where speculative hopes for de-escalation clash directly with an undeniable physical supply crunch. Furthermore, the broader trend over the past two weeks has seen Brent decline from $101.16 on April 1st to $94.09 yesterday, indicating sustained downward pressure on prices even before this latest development, suggesting that while the immediate catalyst was geopolitical, underlying factors may also be at play.

Decoding Investor Sentiment: What’s Driving the Questions?

Amidst such unprecedented volatility, our proprietary reader intent data offers invaluable insight into the immediate concerns of oil and gas investors. A predominant theme this week revolves around directional uncertainty, with many asking simply whether WTI crude is “going up or down.” This fundamental question highlights the immediate struggle market participants face in interpreting conflicting signals and positioning their portfolios. Beyond short-term movements, there’s significant interest in the longer-term outlook, with queries like “what do you predict the price of oil per barrel will be by end of 2026?” This indicates that investors are not only reacting to daily swings but are also attempting to model the lasting impact of current events on future valuations. The specific interest in individual companies, such as inquiries about how Repsol might perform by the end of April 2026, further underscores a broader strategy to identify resilient or undervalued assets within a turbulent sector. These questions collectively paint a picture of investors actively seeking clarity and actionable intelligence, grappling with both macro-geopolitical forces and their micro-economic implications for specific energy investments.

Geopolitical Chess: The Illusion of a Quick Resolution

The recent market reaction clearly demonstrates how a single statement, even one quickly denied, can trigger massive price swings. President Trump’s assertion of “productive conversations” regarding a potential resolution, even suggesting a deal within days, contrasted sharply with Iranian officials’ swift denial of any negotiations. This diplomatic back-and-forth injects extreme uncertainty, making the market vulnerable to headline-driven trading rather than underlying fundamentals. While U.S. actions, including releases from strategic reserves and temporary sanctions waivers, have aimed to alleviate market pressure, their impact is limited as long as the core issue of physical supply constraints persists. The Strait of Hormuz remains effectively closed for significant commercial traffic, and analysts widely agree that a genuine reopening of this critical chokepoint is essential to restore flows and normalize the market. Until such a concrete de-escalation occurs, the oil market will likely continue to exhibit extreme volatility, with prices reacting sharply to every political pronouncement, regardless of its immediate veracity or tangible impact on crude supply.

Navigating the Near-Term: Key Catalysts and Market Monitors

For investors seeking to make informed decisions in this hyper-volatile environment, monitoring upcoming market catalysts is paramount. While geopolitical headlines will continue to dictate short-term swings, fundamental data releases offer crucial insights into the true state of supply and demand. On April 22nd, the EIA Weekly Petroleum Status Report will provide a critical update on U.S. crude inventories, refining activity, and product demand, offering a real-time pulse of the domestic market. This will be followed closely by the Baker Hughes Rig Count on April 24th, which signals future production trends. The API Weekly Crude Inventory on April 28th and another EIA report on April 29th will further refine our understanding of inventory dynamics. Looking into early May, the EIA Short-Term Energy Outlook on May 2nd will be particularly influential, offering the agency’s updated forecasts for prices, supply, and demand through the coming months, which could significantly influence investor sentiment. Subsequent API and EIA reports on May 5th and 6th, respectively, will continue to provide essential weekly data. These scheduled releases become even more critical during periods of geopolitical uncertainty, as they provide concrete, quantifiable metrics against which to measure the market’s actual health, helping investors discern between speculative noise and verifiable shifts in energy fundamentals.