GORDON FELLER, Contributing Editor

Fig. 1. Brazil’s pre-salt areas. Map: Petrobras.

Brazil’s oil and gas sector moved through 2025 with the force of its own geology. By January 2026, crude production had climbed to 3.95 MMbpd, a 14.6% surge year-on-year, while natural gas output rose 20% to 6.8 Bcfd. In October 2025, combined hydrocarbon output briefly touched 5.25 MMboed, a milestone that had seemed aspirational just two years earlier.

The engine powering this acceleration is Brazil’s pre-salt polygon, the ultra-deepwater reservoirs beneath a thick salt layer off the southeastern coast, Fig. 1. By early 2025, pre-salt fields were delivering nearly 80% of national crude production, with the Búzios field—the world’s largest offshore pre-salt development—receiving its seventh FPSO, P-78, in September 2025. It is capable of producing 180,000 bopd. In February 2026, yet another FPSO (P-79) arrived on site as the field’s eighth producing unit, Fig. 2. It also has a production capability of 180,000 bopd.

According to Juliana Miguez, research manager, Latin America Upstream Oil & Gas, at Wood Mackenzie, “with industry heavyweights again leading the competition, Brazil’s pre-salt has consolidated as the playground for those with deep pockets. The large resource base and impressive well deliverability produce some of the most attractive development economics outside of tight oil.”

Fig. 2. The eighth FPSO to be installed at Petrobras’ Búzios field, P-79, arrived on site in February 2026. Image: Petrobras.

The single most geopolitically significant event of the 12-month period came in February 2025, when Brazil’s National Council for Energy Policy formally approved the country’s entry into OPEC’s Charter of Cooperation. The timing was provocative: it was just nine months before Brazil hosted COP30 climate talks in Belém. The decision crystallized the central tension of the country’s energy moment—positioning itself simultaneously as a global climate leader and a committed, growing hydrocarbon producer. Energy Minister Alexandre Silveira was unapologetic in his defense: “We should not be ashamed of being oil producers. Brazil needs to grow, develop and create income and jobs.”

Analysts across Asia—Brazil’s largest crude export market—watched the OPEC+ move with strategic interest. China’s refineries, led by Sinopec and CNOOC, significantly increased their liftings of Brazilian pre-salt crude throughout 2025, drawn by its quality and the absence of U.S. tariff complications affecting other suppliers.

Consider the conclusion drawn by Dr. Erica Downs, Senior Research Scholar, Center on Global Energy Policy, Columbia University (in “Where China Gets Its Oil: Crude Imports in 2025,” Columbia CGEP, January 29, 2026): “Brazil’s increasing production and China’s view of the country as a reliable supplier likely contributed to the 28% increase in Brazil’s exports to China.”

INTERNATIONAL CAPITAL FLOWS

For international oil majors, Brazil became a destination of choice. Shell—whose Brazilian pre-salt production now represents roughly 15% of the company’s global output—celebrated first oil at Mero-4 in May 2025. TotalEnergies, Equinor, and QatarEnergy continued ramping commitments; the Sépia complex drew a notable consortium including Malaysa’s Petronas, reflecting Southeast Asian sovereign capital entering Brazil’s deepwater sector for the first time. The July 2025 Equatorial Margin auction was the clearest signal yet that the world’s most capitalized energy companies view Brazil’s frontier acreage as indispensable to their portfolios.

Fig. 3. At its headquarters in Rio de Janeiro, Petrobras has been pursuing a careful balance between oil and gas development and energy transition. Image: Petrobras.

ENERGY TRANSITION

Petrobras’ 2025–2029 strategic plan increased transition-related investment by 42% to $16.3 billion, representing 15% of total capital expenditures, Fig. 3. A further $5.3 billion were ring-fenced for decarbonization of Scope 1 and 2 emissions. Brazil’s world-leading CCUS program—already the largest operational offshore carbon capture program globally, with over 53.8 million tons of CO₂ reinjected since 2015—expanded its scope.

The 2024 New Gas Law continued reshaping the domestic gas market, with third-party pipeline access driving new competition in distribution for the first time in decades. TAG’s $5.2 billion pipeline infrastructure upgrade program and the commissioning of a private LNG terminal in October 2024 illustrated how Brazil’s gas logistics are being restructured outside Petrobras’s direct orbit.

Ali El Hage Filho and Lívia Amorim, at law firm Veirano Advogados, said it clearly: “The New Gas Law established the foundations for the development of a liquid and competitive gas market in which there is no vertically integrated incumbent, there is open access to essential facilities and to the gas transmission system, and where the transport capacity is contracted by means of an entry-exit regime. As a result, a competitive market is expected, which will bring new investments into the industry as well as cost reduction and higher gas consumption.” (Chambers Global Practice Guide: Oil, Gas and the Transition to Renewables 2025 — Brazil, August 2025)

The influential President of the Brazilian Institute of Oil, Gas and Biofuels, Roberto Ardenghy, said it this way: “We want to show that we are also part of the solution to achieve emission reduction targets and discuss with all public and private actors the best way to conduct the transition process.” (IBP press release, “IBP supports the launch of a Catavento study on the energy transition from oil and gas,” April 1, 2025).

Brazil’s proven reserves told a parallel story of abundance. Government data confirmed 16.8 Bbbl in proven oil reserves at end-2024—a 6% year-on-year increase—with 81% concentrated in pre-salt formations. Petrobras separately reported a 6% increase in its share of proven reserves to 12.1 Bbbl, reflecting successful drilling across its Búzios and Mero campaigns. Over the past decade, national reserves have expanded 29%, a rate that places Brazil among the world’s most reserve-rich growth stories.

The 12 months ahead will test whether Brazil’s extraordinary production momentum can be sustained. Four structural forces will define the period: the FPSO delivery pipeline; the political economy of the 2026 presidential election; OPEC+ dynamics; and the pace of energy transition investment. Each carries its own risk-and-reward calculus.

THE FPSO PIPELINE

Petrobras’ 2026–2030 plan targets operated hydrocarbon output of 4.5 MMboed by 2029, nearly 10% above 2025 levels. Achieving this requires the successful commissioning of at least three new FPSOs over the coming year, with the P-84 and P-85 vessels—each rated for 225,000 bpd—scheduled for 2029–2030 delivery but requiring subsea installation work, beginning in 2026–2027. With Korean and Singaporean yards operating near capacity, any slippage in construction timelines cascades directly into production targets.

THE EQUATORIAL MARGIN

The Equatorial Margin will be the sector’s most consequential story over the next year. Following Ibama’s controversial approval of a drilling license for Block 59, early well results from the 19 blocks awarded in July 2025 are expected by mid-2026. A significant commercial discovery would reshape Brazil’s long-term production ceiling and trigger a new licensing round. Any environmental incident in this biodiverse coastal zone, however, could trigger regulatory reversal with consequences far beyond the Equatorial Margin itself.

Participation by Chevron and ExxonMobil signals a strategic repositioning. U.S. supermajors, under intense shareholder pressure to demonstrate portfolio quality, view Brazil as offering the rare combination of world-class geology, low breakeven costs, and established rule of law. CNPC’s presence alongside them in the auction was equally strategic—a statement of China’s intent to be embedded in Brazil’s upstream, long before first production.

OPEC+ DYNAMICS

As OPEC+ continues reversing voluntary production cuts agreed in late 2024, Brazil—not bound by quota obligations—will face diplomatic pressure to moderate its public growth signals. Brasília is expected to hold firm. Brazil’s structural position as OPEC’s most production-flexible non-quota member gives it unusual leverage: it can grow output, regardless of cartel decisions while benefiting from the price floor that collective OPEC+ restraint provides. This asymmetric arrangement will be increasingly resented by core OPEC members, as Brazilian volumes reach 4.2+ MMbopd.

Fig. 4. Location of the Santos basin, offshore Brazil. Map: Petrobras.

Canada’s involvement in Brazil’s energy sector is likely to deepen through infrastructure rather than upstream. Canadian pension giants—CPPIB, OTPP, and Brookfield—have significant indirect exposure to Brazilian gas infrastructure through TAG’s pipeline network and gas distribution utilities. As TAG targets BRL 5.2 billion in pipeline upgrades through 2028 under the New Gas Law framework, Canadian institutional capital will find structured opportunities that satisfy ESG mandates while benefiting from Brazil’s gas demand growth.

2026 PRESIDENTIAL ELECTION

Brazil’s 2026 presidential election will force a public reckoning over oil revenues versus climate commitments that the Lula administration has so far managed to keep in separate political compartments. Candidates across the spectrum will need to stake positions on Petrobras’ dividend policy, Equatorial Margin expansion, and the pace of transition spending. Oil sector stocks will be unusually sensitive to shifting poll numbers. A government perceived as willing to revisit Petrobras’s pricing mandate—a flashpoint under the Bolsonaro administration—would rattle international investors, who have calibrated their Brazil exposures on regulatory stability.

PETROBRAS INVESTMENT PLAN EVOLUTION

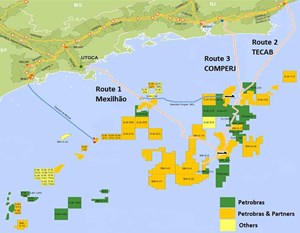

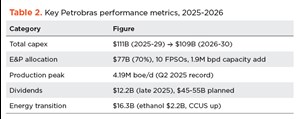

In late 2024, Petrobras unveiled a $111 billion five-year strategic plan for 2025-2029, prioritizing E&P, with $77 billion allocated—about 70% of the total—to offshore pre-salt fields. This includes deploying 10 FPSOs by 2030, targeting a production peak of 3.2 MMboed, and $3 billion for the Equatorial Margin near the Amazon. By mid-2025, second-quarter capex hit $4.4 billion (up 9% quarter-on-quarter and 32% year-on-year for the first half at $8.5 billion), fueling new wells in the Campos and Santos basins (Fig. 4), though net debt surged 27% to $58.56 billion amid lower oil prices.

By October-November 2025, facing Brent volatility, Petrobras revised its plan down to a $109 billion figure (Tables 1 and 2) for 2026-2030, trimming E&P slightly while boosting energy transition to $16.3 billion (15% of capex, up 42% from prior plan). Ethanol received $2.2 billion, biorefining $1.5 billion, and hydrogen/CCUS $1.4 billion, signaling diversification beyond fossil fuels despite renewables like wind/solar dipping 17%. Midstream/downstream rose to $16 billion from $12 billion, including a $900 million ammonia plant revival.

ACTIVITY HIGHLIGHTS

Petrobras shattered records in second-quarter 2025 with 4.19-MMboed operated production (Table 2), driven by FPSO ramp-ups like Almirante Tamandaré (225,000 bopd), Alexandre de Gusmão, and P-78. Short-term targets climbed to 2.5 MMbopd, with pre-salt dominating (76% of output) and post-salt at 24%.

Delays did hit some projects. The P-80 FPSO and Barracuda/Caratina revitalizations shifted to one year later; Albacora by 10 years; SEAP vessels uncontracted. Petrobras’ international projects grew 30%, including appraising Colombia’s Sirius deepwater find and exploring São Tomé & Príncipe and South African blocks. Divestments continued for liquidity, with new ANP bidding rounds emphasizing mature onshore fields (fracing-adjacent, but not core).

Petrobras’ M&A activity was modest but strategic. Petrobras facilitated cross-border deals via asset sales, contributing to Brazil’s 175 oil/gas transactions in early 2025, attracting U.S./European buyers. Foreign investment is projected at $122 billion by 2029, with partners like Shell fast-tracking Gato do Mato (370+ MMbbl recoverable) alongside Ecopetrol/TotalEnergies, and Chevron/ExxonMobil expanding pre-salt stakes.

Petrobras’ second-quarter 2025 profits rebounded to $4.7 billion from a $480 million loss year-on-year, yet free cash flow fell 44%, due to capex/debt pressures. By the back half of 2025, fortunes flipped: there was a record $6 billion profit and $12.2 billion dividends announced in November, bolstering shares amid Brazil’s non-OPEC+ growth leadership. However, 2026 forecasts warn of M&A slowdowns and election risks, with $45 billion to $55 billion in planned dividends, balancing fiscal needs.

Under Lula, Petrobras has aligned with the national agenda aiming for energy security, rejecting full fracing bans but mandating studies. The national government in Brasília backed hydraulic fracturing selectively, despite green opposition. Gas liberalization advanced via LRCAP 2026 auctions for LNG/pipelines, unlocking infrastructure.

Challenges persisted: volatile prices paused some drilling, there were unitization disputes with partners, and stranded asset risks existed in net-zero transitions. Yet, tax contributions (5% of Brazil’s total investments) and portfolio resilience positioned Petrobras for sustained dominance.

HYDRAULIC FRACTURING INSIDE BRAZIL

Hydraulic fracturing, or fracing, remains a contentious topic in Brazil, with limited but notable developments in investments, policy, and related energy activities over the past 14 months (December 2024 to February 2026). While Brazil’s energy sector has boomed in offshore oil and renewables, onshore fracing—primarily explored in the Paraná basin—has seen cautious progress amid environmental pushback and regulatory hurdles.

The Petrobras five-year plan for 2025-2029 included $3 billion for the Equatorial Margin near the Amazon, where exploratory drilling approvals advanced after IBAMA rejections in 2023 were overturned following proposal amendments. These moves signal indirect support for unconventional plays, potentially paving the way for hybrid onshore-offshore tech applicable to fracing. Petrobras has no explicit fracing plans outlined for 2026, focusing instead on conventional offshore oil expansion. Onshore efforts remain marginal, emphasizing mature fields rather than hydraulic fracturing.

Key onshore activity centers on the Foz do Amazonas basin, where Petrobras secured permits for 15 wells, including two exploratory drills approved after IBAMA revisions. These are conventional vertical wells, not fracing operations, despite environmental opposition over Amazon risks.

Smaller players drove fracing-adjacent M&A. In August 2025, New Stratus Energy inked a $10 million farm-in deal with Vultur Oil in the Reconcavo basin, targeting mature fields with horizontal re-entry and lateral wells—techniques akin to fracing for enhanced recovery. The two-stage investment yields 32.5% working interest in blocks holding 3.07 MMBOE of proved reserves and 4.98 MMBOE, proved-plus-probable, pending ANP approvals. Broader M&A in oil and gas ticked up, with 175 cross-border deals in early 2025, led by U.S. and European firms.

Regulatory green lights emerged despite controversy. In October 2025, IBAMA approved Petrobras’ Amazon drilling after revisions. Nationally, ANP streamlined unconventional licensing, but fracing bans persist in Paraná and Rio Grande do Sul, due to seismic and water concerns. Lula’s administration balanced fossil fuel growth with net-zero pledges, rejecting full fracing bans while mandating environmental impact studies. Opposition intensified, with NGOs decrying Amazon risks and water contamination parallels to U.S. fracing.

Overall, Brazil’s fracing news reflects tentative thawing—bolstered by Petrobras’ capital influx and niche deals—but hobbled by policy caution and green transitions.

CONCLUSION

Fig. 5. A mix of FPSOs and semisubmersible production platforms (like the P-51 pictured) is pushing Brazil’s oil production to new levels. Image: Petrobras.

The geopolitical framing will intensify over the coming year. China’s appetite for Brazilian crude is structural, rather than cyclical. CNPC’s Equatorial Margin participation was a strategic statement, as much as a commercial one. India, too, is evaluating increased offtake arrangements, as its refining complex expands and it seeks alternatives to Middle Eastern supply. Brazil’s emergence as OPEC’s most production-flexible non-quota member gives it unusual leverage—growing output regardless of cartel decisions, while benefiting from the price floor that collective restraint provides.

Perhaps the most nuanced risk in the 12 months ahead is reputational rather than operational. Brazil will carry the diplomatic weight of its COP30 hosting legacy into 2026 international negotiations. If the Equatorial Margin produces an environmental incident—an oil spill in one of the world’s most biodiverse coastal systems—the political and financial fallout would be severe, potentially triggering a reassessment of the entire offshore expansion program in ways that no CEO’s projections currently model.

Brazil stands at a threshold. Its geology is extraordinary, its technical capabilities world-class, its strategic positioning in global energy markets without precedent in its history, Fig. 5. The next twelve months will reveal whether the institutional architecture—regulatory, environmental, political—is robust enough to sustain the ambition of the production plans being written in Petrobras’s Rio de Janeiro headquarters. It’s possible that Brazil could become the world’s fourth-largest oil producer by 2030.

FTI Consulting’s Perspective

Over the past year, Brazil’s oil and gas sector has seen significant growth. National production reached record levels, led by pre-salt developments and strong output from key fields. Petrobras and other companies reached historic production milestones, strengthening the country’s position as a major player in the global market.

Exploration activity has also increased, with more blocks on offer and multiple auctions held across the country, including in the Foz do Amazonas basin near the Amazon River’s mouth. These auctions have drawn both investment interest and growing concern over environmental and Indigenous impacts, given the area’s ecological sensitivity.

Brazil’s oil and gas sector seems to be heading in two directions at once: it is breaking records with production from pre-salt fields, while also pushing an ambitious exploration agenda in frontier areas subject to increasing scrutiny.

With this approach, the sector will probably continue facing many familiar challenges, including:

Bottlenecks in infrastructure and logistics, including limited pipelines, ports, storage facilities and refining capacity.

High operational costs, particularly in the pre-salt fields, as they require advanced technology and specialized techniques to produce efficiently.

Regulatory and social issues, such as strong environmental and Indigenous scrutiny, regulatory hurdles and public opposition.

Looking ahead, Brazil is expected to remain a key player in this market, with production continuing to grow, especially as companies advance the exploration of pre-salt fields. Petrobras and other major players are also investing heavily in infrastructure to bolster output further.

The Lula administration views Brazil’s oil and gas resources as strategic means to fund the country’s energy transition, using the revenues from these sources to support investment in renewables initiatives. Yet, balancing this will be challenging, and its success will depend on how well the government can attract investment, handle social and environmental concerns, and push the energy transition without slowing production. This approach is highly controversial and adds to ongoing tensions about Brazil’s role in sustainable development, as the country tries to position itself as a climate leader.

It will also be important to watch the upcoming presidential elections. While Lula is currently leading the polls, the right-leaning opposition has gained ground. If it were to win, it could prioritize competitiveness and production growth over transitional initiatives. That said, any changes would likely appear as policy adjustments or regulatory tweaks and are unlikely to cause any major shifts in the industry, in the short term.

Related Articles

FROM THE ARCHIVE