The global energy landscape is once again grappling with heightened geopolitical risk following a rare joint condemnation from a coalition of major world economies regarding ongoing threats to navigation in the Strait of Hormuz. Leaders from the United Kingdom, France, Germany, Italy, the Netherlands, Japan, and Canada have collectively voiced strong concerns over recent actions by Iran, including attacks on commercial vessels and critical oil and gas infrastructure. This concerted international stance underscores the severity of the situation at one of the world’s most vital maritime chokepoints, directly impacting global oil supply chains and, consequently, the investment outlook for the energy sector.

For investors, the implications are profound. The Strait of Hormuz is the narrow gateway through which roughly a fifth of the world’s total oil consumption passes daily. Any disruption here poses an immediate and significant threat to global energy security, with potential ripple effects across commodity markets, inflation, and economic stability. Understanding the nuances of this escalating tension, coupled with the market’s current response and forward-looking indicators, is crucial for navigating the inherent volatility in oil and gas investing.

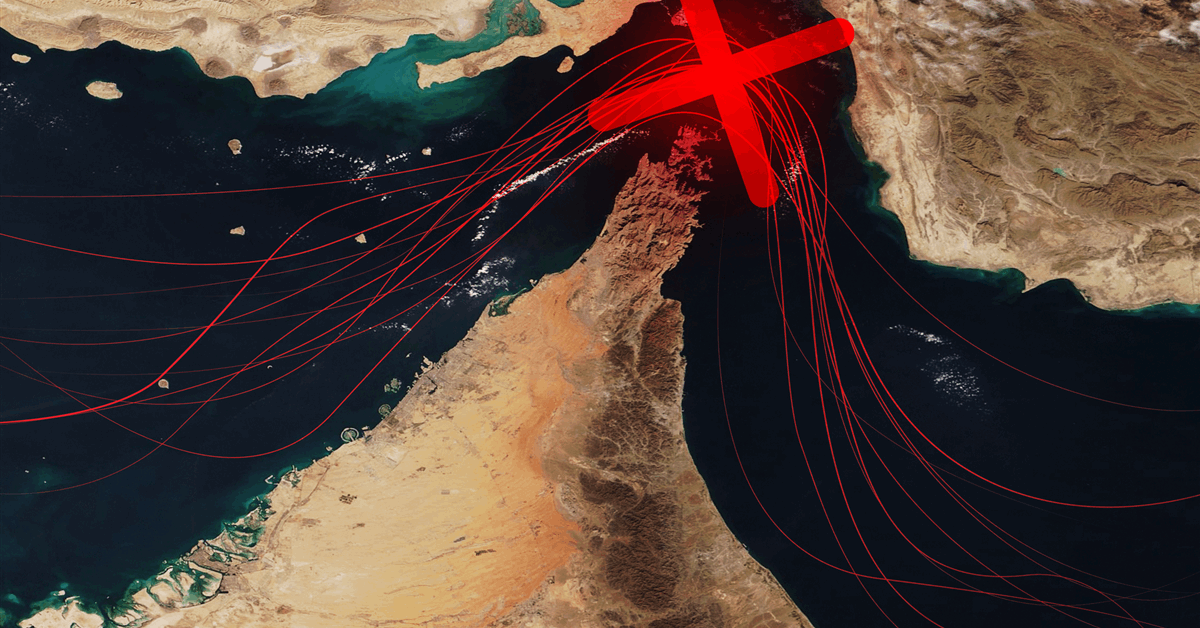

Geopolitical Tensions Escalate: The Hormuz Chokepoint Under Threat

The recent joint statement from leading global economies highlighted grave concerns over Iran’s persistent interference with international shipping and attacks on civilian infrastructure within the Gulf region. This includes direct threats to oil and gas installations and what has been termed a “de facto closure” of the Strait of Hormuz to commercial shipping. The leaders emphasized that freedom of navigation is a fundamental principle of international law, and any sustained disruption to global energy supply chains constitutes a serious threat to international peace and security. Such actions, including the reported laying of mines and drone attacks, aim to impede the free flow of critical energy resources, directly impacting not only energy-importing nations but also the broader global economy, particularly the most vulnerable populations.

The strategic importance of the Strait cannot be overstated. It connects the Persian Gulf to the open ocean, serving as the sole maritime passage for crude oil and liquefied natural gas (LNG) from countries like Saudi Arabia, Iran, Iraq, Kuwait, Qatar, and the UAE. While the immediate impact of these threats has been limited to date, the sustained rhetoric and specific incidents reported by international bodies suggest a growing risk premium that could materialize rapidly. Investors must recognize that even the perception of a sustained blockade can trigger significant market shifts, compelling a re-evaluation of supply security and alternative routes.

Navigating Market Volatility: A Disconnect in Crude Prices?

Despite the escalating geopolitical rhetoric and the clear threat to a major oil artery, the immediate market reaction has been somewhat muted, suggesting a complex interplay of factors influencing investor sentiment. As of today, April 22, 2026, Brent Crude trades at $91.9 per barrel, reflecting a 1.44% decline for the day, with its range fluctuating between $91.39 and $94.21. Similarly, WTI Crude sits at $88.23, down 1.61% from its open, trading within a daily range of $87.64 to $90.71. Gasoline prices have also seen a slight dip, currently at $3.09, down 0.96%.

This recent softening in prices, even with the looming threat in the Gulf, raises questions for investors who might expect an immediate spike. Indeed, our proprietary data shows that Brent crude has trended downwards by approximately $7.07, or 7%, over the past 14 days, falling from $101.16 on April 1st to $94.09 on April 21st. This downward pressure, even amidst geopolitical uncertainty, highlights the market’s current focus on broader supply-demand dynamics and perhaps a belief in the international community’s ability to contain the immediate crisis. Many investors are asking, “Is WTI going up or down?” The answer is nuanced: while the Hormuz situation presents significant upside risk, other factors like potential demand concerns or strategic releases are providing a counter-balance, keeping prices anchored for now. However, this delicate balance could be easily upset by any further escalation.

Global Response and Supply-Side Resilience

The international community’s response to the threats in the Strait of Hormuz extends beyond mere condemnation. The joint statement welcomed the International Energy Agency’s (IEA) decision to authorize a coordinated release of strategic petroleum reserves (SPR). This proactive measure aims to stabilize energy markets by injecting additional supply should disruptions materialize. Such releases have historically been used to mitigate price spikes during crises, providing a temporary buffer against supply shocks.

Furthermore, the leaders committed to working with certain producing nations to increase output, signaling a concerted effort to boost global supply capacity. This coordinated approach aims to demonstrate a readiness to offset potential shortfalls, which could temper speculative buying in the market. Domestically, industry groups like Offshore Energies UK (OEUK) have also affirmed the UK offshore energy sector’s readiness to contribute to boosting supplies, emphasizing the importance of diverse and secure energy sources. This multi-pronged strategy, combining emergency reserves with commitments from producers, suggests a significant effort to build resilience against the current geopolitical headwinds, providing a critical layer of reassurance for investors concerned about the immediate supply outlook.

Forward Outlook: Key Catalysts and Investment Horizon

For investors focused on the oil and gas sector, the coming weeks will present a series of critical data points that will further shape market sentiment and price trajectories. Beyond the immediate geopolitical concerns in the Strait of Hormuz, the fundamental supply-demand picture remains a powerful driver. Our proprietary event calendar highlights several upcoming releases that demand close attention.

This week, on Wednesday, April 22nd, the EIA Weekly Petroleum Status Report will offer fresh insights into U.S. crude oil and product inventories, refining activity, and demand indicators. This will be followed by the Baker Hughes Rig Count on Friday, April 24th, providing a pulse on North American drilling activity and future supply potential. These reports are recurring events, with subsequent releases for API Weekly Crude Inventory on April 28th and May 5th, and EIA Weekly Petroleum Status Reports on April 29th and May 6th. Any significant shifts in these metrics, particularly concerning inventory builds or draws, could either exacerbate or alleviate the market’s response to geopolitical tensions.

A particularly influential release will be the EIA Short-Term Energy Outlook (STEO) on Saturday, May 2nd. The STEO provides updated forecasts for supply, demand, and prices across various energy commodities, offering a crucial baseline for investors asking, “What will the price of oil per barrel be by end of 2026?” This report will integrate the latest geopolitical developments and economic projections, potentially offering a clearer long-term price signal. While no single report can predict the future with certainty, these scheduled data releases, coupled with the ongoing dynamics in the Gulf, will be instrumental in shaping the investment thesis for the remainder of 2026. Investors should monitor these events closely for signs of market rebalancing or further supply-side pressures, which will dictate the risk-reward profile of energy assets.