The recent U.S. strike near Iran’s Kharg Island, a pivotal node in global energy trade, has once again thrust Middle Eastern geopolitical tensions into the spotlight for oil and gas investors. While initial reports indicate that critical oil infrastructure was deliberately avoided, and export operations continue, the incident serves as a stark reminder of the region’s inherent volatility and the potential for supply disruptions. For investors navigating a complex market, understanding the immediate implications, the broader geopolitical backdrop, and the forward-looking indicators is paramount. Our proprietary data pipelines reveal a nuanced market reaction, with crude prices exhibiting relative stability in the immediate aftermath, yet the underlying concerns about shipping security and future escalation remain palpable. This analysis delves into the strategic importance of Kharg, the current market dynamics, and the key data points investors should monitor in the coming weeks to position their portfolios effectively.

Kharg Island: A Critical Juncture for Global Crude Exports

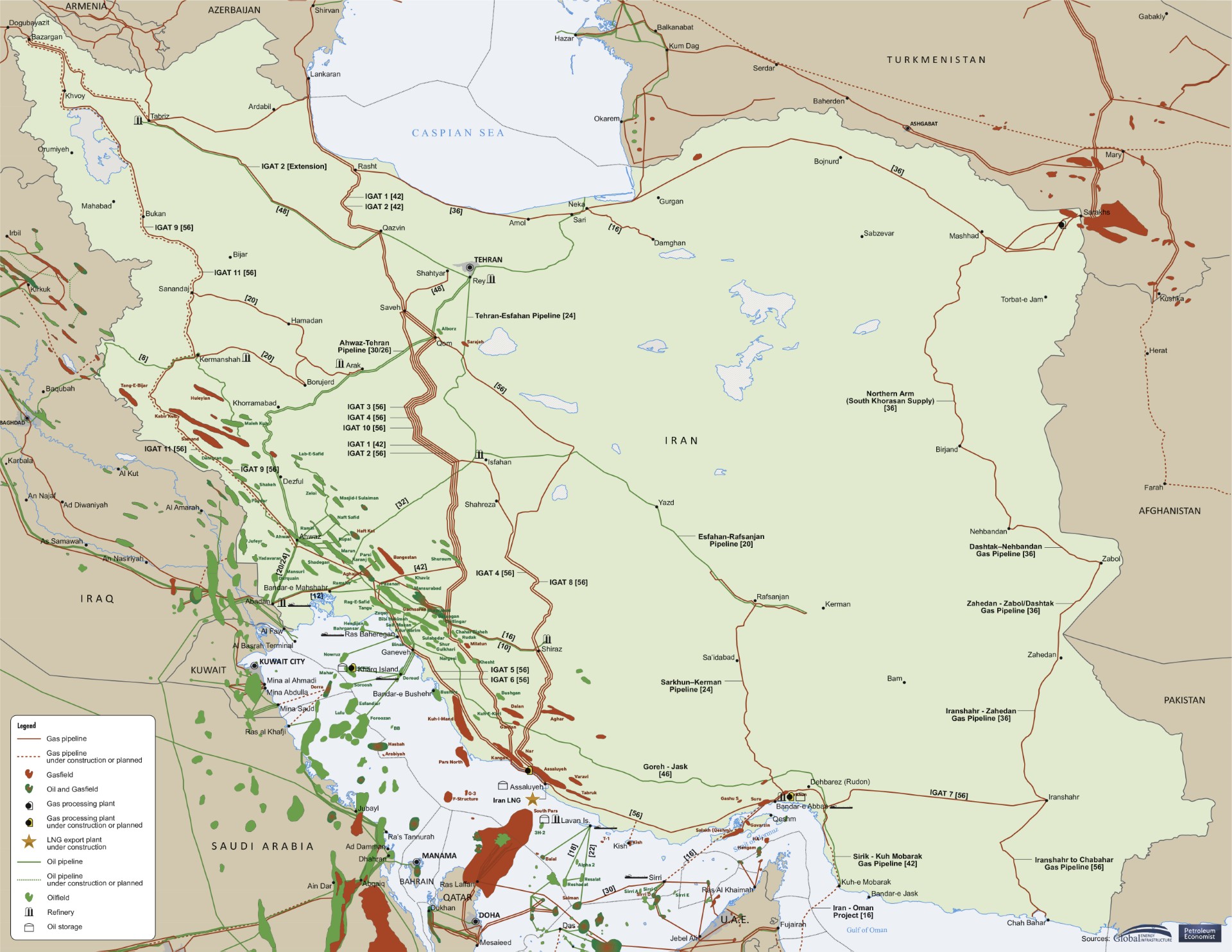

Kharg Island stands as the undisputed heart of Iran’s crude export capabilities, handling approximately 90% of the nation’s total shipments, with a significant portion destined for China. The recent U.S. military action in its vicinity, targeting non-oil installations, was a calculated move to exert pressure without directly disrupting global energy supply. This strategic restraint was met with a clear warning from Tehran: any assault on its energy infrastructure would trigger retaliatory strikes against U.S.-linked energy assets across the region. Despite the heightened alert, proprietary tanker monitoring data from TankerTrackers.com confirmed that two large crude carriers, one capable of transporting about 2 million barrels, were berthed and operations continued hours after the strike. Iranian media corroborated these reports, underscoring that the immediate threat to physical supply from Kharg was averted. However, the incident undeniably exposed the fragility of such critical infrastructure. As analysts at JPMorgan have previously noted, a scenario where Kharg Island were taken offline “could quickly force Iran to curtail production and place a significant portion of its exports at risk,” illustrating the high stakes involved in any direct impact on this hub.

Market Dynamics: Muted Reaction Amid Lingering Uncertainty

In the wake of the Kharg Island incident, the immediate market response has been surprisingly restrained, reflecting perhaps the specific nature of the strike that avoided oil facilities. As of today, Brent crude trades at $92.9 per barrel, marking a modest -0.36% decline within a daily range of $92.57 to $94.21. Similarly, WTI crude is priced at $89.24, down -0.48%, fluctuating between $88.76 and $90.71. These relatively small daily movements suggest that while the geopolitical tension is acknowledged, the market is not currently pricing in a significant, imminent supply disruption from Kharg itself. However, this short-term stability contrasts sharply with the broader trend. Our 14-day Brent data shows a more significant correction, with prices falling from $101.16 on April 1st to $94.09 on April 21st, representing a $7.07 or 7% drop. This broader decline indicates that other factors, such as demand concerns or the unwinding of previous risk premiums, have been exerting downward pressure on prices, overshadowing the immediate Kharg event. Moreover, the enduring issue of shipping disruptions through the Strait of Hormuz, a conduit for roughly one-fifth of global oil and natural gas exports, continues to be a major concern, with vessel-tracking data indicating minimal tanker traffic since the conflict began. This ongoing challenge to maritime security remains a critical, unresolved risk for global supply chains.

Beyond Kharg: The Widening Arc of Geopolitical Risk

While the focus remains on Kharg Island, investors must broaden their perspective to the wider regional energy landscape. The U.S. strike and Iran’s subsequent warnings highlight the vulnerability of an interconnected network of critical energy infrastructure across the Gulf. Key facilities such as Saudi Arabia’s Ras Tanura export terminal, the world’s largest oil loading facility, and its Abqaiq processing hub, a cornerstone of global crude supply, are prime examples. Similarly, the Fujairah oil hub in the United Arab Emirates, a vital bunkering and storage location outside the Strait of Hormuz, represents another critical node. Any escalation that targets these facilities would have far more severe and immediate consequences for global oil supply than the recent Kharg incident. Investor inquiries, such as “what do you predict the price of oil per barrel will be by end of 2026?”, underscore the deep uncertainty surrounding long-term price trajectories. The incident at Kharg serves as a potent reminder that such predictions are highly susceptible to sudden shifts in geopolitical dynamics. The risk of miscalculation or an unintended escalation remains high, demanding constant vigilance from investors tracking their energy portfolios.

Navigating the Near-Term Outlook: Key Data Points for Astute Investors

For investors seeking clarity amidst the volatility, and looking to answer questions like “is WTI going up or down,” the next few weeks offer several crucial data releases that will shape the market narrative. Our proprietary event calendar highlights key dates for assessing supply, demand, and sentiment:

- EIA Weekly Petroleum Status Reports: Scheduled for April 22nd, April 29th, and May 6th, these reports are indispensable. They provide real-time insights into U.S. crude oil and product inventories, refinery utilization, and demand indicators. Any unexpected builds or draws, especially in light of the ongoing Middle East tensions and Strait of Hormuz shipping slowdowns, could significantly sway market sentiment and price direction.

- Baker Hughes Rig Counts: On April 24th and May 1st, the Baker Hughes Rig Count will offer a gauge of North American drilling activity. A rising count could signal an anticipated increase in future supply, potentially counteracting geopolitical risk premiums, while a decline might suggest producers are exercising caution.

- EIA Short-Term Energy Outlook (STEO): The release on May 2nd is particularly significant. The STEO provides the U.S. government’s updated forecasts for crude oil and natural gas prices, supply, and demand. This comprehensive outlook will incorporate recent geopolitical developments and offer crucial guidance for investors looking to refine their end-of-year 2026 price predictions and strategic positioning.

Monitoring these data points in conjunction with the evolving geopolitical situation will be critical for making informed investment decisions. The interplay between fundamental supply-demand dynamics and persistent geopolitical risk will dictate crude price movements in the immediate future, demanding a flexible and data-driven approach from all market participants.