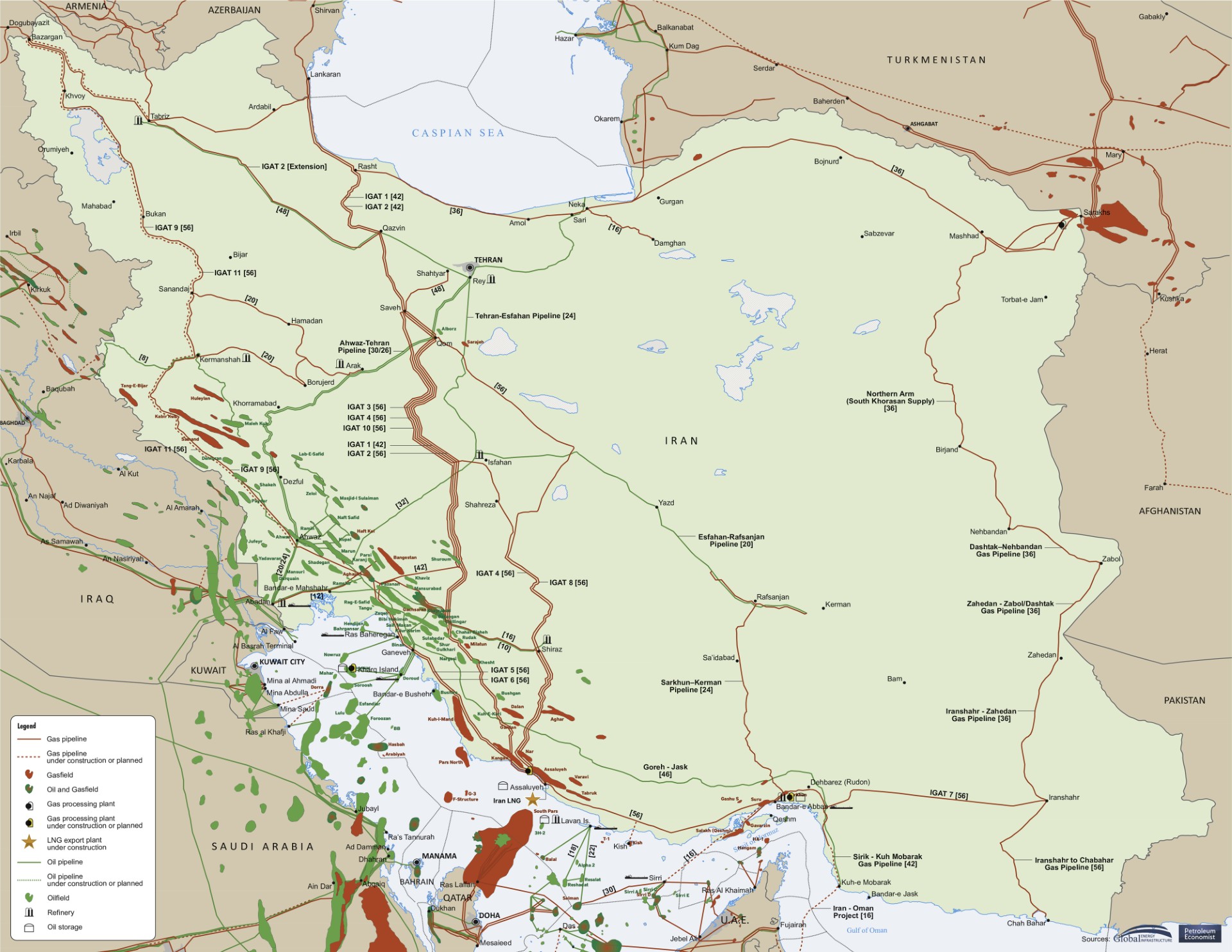

The global energy landscape remains a crucible of geopolitical tension and economic forces, nowhere more evident than in the recent volatility surrounding the Strait of Hormuz. Just weeks ago, the market witnessed Brent crude surging past the critical psychological threshold of $100 a barrel for the first time since August 2022, fueled by significant maritime disruptions in the Persian Gulf. This dramatic ascent, driven by concerns of the largest oil market supply disruption in history, sent ripples across investor portfolios and triggered swift policy considerations. However, our proprietary OilMarketCap.com data pipelines reveal a more nuanced picture today, underscoring the market’s dynamic response and the ongoing battle between supply anxieties and demand realities. Understanding this evolving narrative is crucial for investors navigating the complexities of the current oil and gas market.

Hormuz Fallout vs. Current Market Snapshot: A Reassessment

The initial shockwaves from the Arabian Gulf, marked by multiple vessel attacks and fears of a broadening campaign of maritime disruption, undeniably propelled crude benchmarks upward. On March 12th, Brent crude experienced a notable 9.2% surge, settling above $100, while West Texas Intermediate (WTI) climbed 9.7% to a near four-year high of $95.73. Analysts and market participants quickly flagged the potential for sustained high prices, with some even drawing parallels to the 2008 peak if flow disruptions through Hormuz persisted. Indeed, the International Energy Agency characterized the situation as the largest supply disruption in the history of the global oil market, triggering wild price swings exacerbated by financial flows into options and exchange-traded funds.

However, the market’s narrative has since evolved. As of today, Brent crude trades at $92.85, down 0.42% within a day range of $92.57-$94.21. Similarly, WTI crude stands at $89.39, reflecting a 0.31% decline for the day, with its range between $88.76-$90.71. Our 14-day Brent trend data further highlights this shift: from a peak of $101.16 on April 1st, Brent has steadily declined to $94.09 by April 21st, representing a $7.07 or 7% drop. This significant retracement from the recent highs suggests that while the geopolitical risk premium remains a factor, initial panic has somewhat subsided, or at least been balanced by other market forces. Policy interventions, alongside mixed signals regarding the resumption of full flows through the Strait, have contributed to this recalibration, preventing a sustained breach of the $100 psychological barrier for Brent.

Policy Responses and Their Temporary Nature

In response to the escalating prices and the potential economic fallout, governments moved swiftly, albeit with measures that often carried a temporary label. The administration, for instance, announced plans to issue 30-day waivers for the Jones Act, a maritime law requiring American-built ships for domestic port transport. These waivers aimed to allow foreign tankers to supply East Coast refiners with fuel from the Gulf Coast, intending to alleviate price pressures. Alongside this, discussions around strategic petroleum reserve (SPR) releases, with plans to release 172 million barrels, also entered the public discourse. While these actions provided some immediate relief, as one prominent analyst noted, such measures are “only a temporary fix.” The longer the underlying disruption endures, the less effective these short-term actions become in fundamentally altering oil prices.

The market’s reaction to these policy moves was evident in the trimming of earlier gains, but their capacity to fundamentally shift the supply-demand balance in the face of a major disruption is limited. The core issue remains the millions of barrels potentially trapped or delayed in transit through a critical global chokepoint. While a temporary increase in shipping flexibility or a draw from reserves can buy time, they do not resolve the root cause of the supply risk. Investors must recognize the distinction between market-calming rhetoric and genuine, sustainable solutions to supply chain vulnerabilities.

Navigating Investor Concerns: Price Trajectory and Outlook

Our proprietary reader intent data reveals a consistent theme among investors: a keen interest in the future direction of oil prices. Questions like “is WTI going up or down?” and “what do you predict the price of oil per barrel will be by end of 2026?” underscore the uncertainty and the need for clear, data-driven analysis. Given the current dynamics, where Brent has retreated from its $100 peak, the immediate trajectory appears to be a tug-of-war. The underlying geopolitical tensions in the Middle East, particularly around the Strait of Hormuz, continue to represent a potent upside risk. Any re-escalation or further confirmation of prolonged disruption could quickly send prices climbing again.

However, demand-side concerns, coupled with the temporary calming effect of policy responses and potential for diplomatic de-escalation, provide a counterweight. The recent cancellation of fuel-export cargoes by Chinese refiners, following directives to halt new contracts, signals a potential softening of demand from a key consumer, which could cap upside movements. While Goldman Sachs previously warned of Brent potentially exceeding its 2008 peak of $147.50 if Hormuz flows remained depressed through March, the current market reality suggests this extreme scenario has not materialized in the short term. For the remainder of 2026, the oil market will likely remain highly sensitive to geopolitical developments, global economic growth forecasts, and the pace of energy transition. Investors should anticipate continued volatility, with both upward and downward pressures vying for dominance.

Key Data Points on the Horizon for Informed Decisions

For savvy investors looking to capitalize on, or hedge against, the ongoing market fluctuations, closely monitoring upcoming energy events is paramount. Our proprietary calendar highlights several critical releases in the coming weeks that will offer fresh insights into supply-demand balances and production trends. Tomorrow, on April 22nd, the EIA Weekly Petroleum Status Report will provide crucial data on U.S. crude oil, gasoline, and distillate inventories, as well as refinery utilization rates. A significant draw in crude inventories could signal tighter supply than anticipated, potentially boosting prices, while a build might exert downward pressure.

Further insights into U.S. production activity will come with the Baker Hughes Rig Count on April 24th and again on May 1st. Changes in active drilling rigs can be a leading indicator of future supply. Additionally, the API Weekly Crude Inventory reports on April 28th and May 5th will offer an early look at inventory movements. Perhaps most significant for longer-term outlooks will be the EIA Short-Term Energy Outlook (STEO) due on May 2nd. This report provides updated forecasts for supply, demand, and prices, offering a foundational perspective for the coming months and quarters. Given the current gasoline price at $3.11, down 0.64% for the day, these reports will also be critical in understanding refined product markets and their impact on overall crude demand. These scheduled data releases will be instrumental in assessing the true impact of recent disruptions and the effectiveness of global supply adjustments, guiding investors in their strategic positioning.