The global oil market is once again grappling with the intricate dance between geopolitical tensions and fundamental supply-demand dynamics. Following recent escalations in the Middle East, U.S. Energy Secretary Chris Wright has stepped forward to assuage market anxieties, asserting that the current surge in oil prices is largely a “fear premium” and that global energy supplies remain robust. Investors, however, are rightfully scrutinizing this optimistic outlook, seeking clarity on the true duration of disruptions and the underlying health of crude fundamentals. At OilMarketCap, our proprietary data pipelines offer a granular view, allowing us to dissect the Secretary’s claims against real-time market movements and upcoming catalysts that will truly shape investor sentiment.

Deconstructing the ‘Fear Premium’: Market Realities vs. Official Rhetoric

Secretary Wright’s assertion that the market is exhibiting an “emotional reaction” to a temporary conflict, rather than a genuine supply shortage, paints a picture of short-lived volatility. He suggested that even in a “worst-case” scenario, significant disruptions to shipping lanes like the Strait of Hormuz would be a matter of weeks, not months. While such statements aim to calm nerves, the market’s initial reaction was palpable. However, a closer look at our live data snapshot reveals a nuanced picture. As of today, Brent Crude trades at $92.78, down 0.49% within a daily range of $92.57 to $94.21. Similarly, WTI Crude is at $89.4, experiencing a 0.3% decline, fluctuating between $88.76 and $90.71. This intraday dip, while minor, suggests some tempering of aggressive buying. More significantly, our 14-day Brent trend data indicates that prices have already retreated from $101.16 on April 1st to $94.09 on April 21st, representing a notable 7% decline. This suggests that while an initial fear premium certainly drove prices higher, the market may have already begun to price in a de-escalation or, at the very least, a re-evaluation of the conflict’s immediate impact on global supply. The Secretary’s comments, therefore, align with a trend that was already underway, perhaps reinforcing the market’s move away from peak fear.

Navigating Supply Claims and Hormuz Headwinds

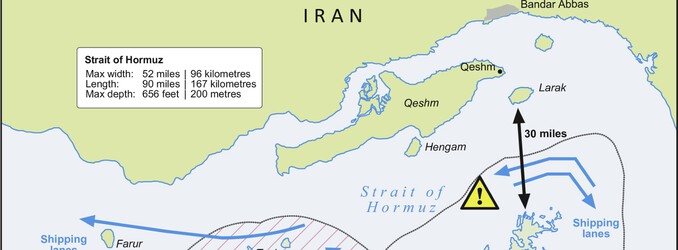

A cornerstone of the Secretary’s argument is the sufficiency of global oil and natural gas supplies, coupled with an explicit statement that there are “no plans to target Iran’s oil industry, their natural gas industry, or anything about their energy industry.” This latter point is critical for investors, as direct targeting of a major producer’s infrastructure would fundamentally alter the global supply landscape. However, the operational reality on the ground presents a challenge to the ‘temporary’ narrative. While the Secretary cited a tanker transit through the Gulf, our intelligence indicates that Hormuz transit remained near a standstill for a sixth day, with only Iran-linked tankers reportedly making the crossing. This discrepancy between official statements and observed shipping activity creates uncertainty. For investors trying to answer “Is WTI going up or down?”, the ongoing disruption in a critical choke point for over 20% of the world’s oil supply cannot be easily dismissed, even if the geopolitical timeline is compressed to a few weeks. The market is weighing the potential for quick resolution against the tangible, albeit perhaps short-term, impact on oil flows and the associated risk premiums.

Forward Outlook: Key Data Points for Informed Investment Decisions

Beyond the immediate geopolitical headlines, savvy investors understand that fundamental data will ultimately dictate market direction. Our proprietary event calendar highlights several crucial upcoming releases that will offer invaluable insights into the true state of global supply and demand, helping to answer perennial questions like “what do you predict the price of oil per barrel will be by end of 2026?”

- On Wednesday, April 22nd, and again on April 29th and May 6th, the EIA Weekly Petroleum Status Report will provide essential data on U.S. crude oil and product inventories, refining activity, and demand. Significant draws could signal tightening markets, while builds would counter the fear premium narrative.

- The Baker Hughes Rig Count, scheduled for Friday, April 24th, and again on May 1st, offers a leading indicator of future U.S. oil production. A sustained increase in active rigs could point to growing supply capacity, dampening long-term price expectations.

- API Weekly Crude Inventory reports on April 28th and May 5th will offer an early look at U.S. stock levels, often setting the tone for the official EIA release.

- Perhaps most critically for longer-term predictions, the EIA Short-Term Energy Outlook (STEO) on May 2nd will present the U.S. government’s comprehensive forecasts for crude oil, natural gas, and refined products through the end of 2026. This report is a vital input for investors constructing their own price models and assessing the Secretary’s long-term optimism regarding supply sufficiency.

These data points provide concrete anchors in a volatile market, allowing investors to move beyond speculative headlines and ground their decisions in measurable supply-demand indicators. While the Secretary suggests a temporary blip, these reports will reveal whether underlying market conditions support a swift return to lower price levels.

Investor Sentiment and the Path Ahead

The questions from our readers this week underscore the market’s current uncertainty: “Is WTI going up or down?” and “what do you predict the price of oil per barrel will be by end of 2026?” The Energy Secretary’s comments lean heavily towards a downward trajectory in the near term, once the “fear premium” dissipates. The recent 7% decline in Brent over the past two weeks suggests that this unwinding might already be in progress, independent of the Secretary’s public statements. However, the path forward is rarely linear. While there are “no plans” to target Iranian oil infrastructure, the ongoing geopolitical friction in a region critical to global energy flows means that risk premiums can re-emerge swiftly. Furthermore, while U.S. retail gasoline prices have seen some relief, now at $3.1 per gallon (down 0.64% today), compared to the recent spike, they remain above the $3 mark that the administration aims for. This indicates that the market is still processing a complex array of factors.

For investors, the key lies in maintaining vigilance. The Secretary’s perspective offers a potential ceiling to the “fear premium,” suggesting that the current Middle East crisis may not metastasize into a prolonged supply disruption. However, the upcoming fundamental data releases will provide the essential ground truth. OilMarketCap’s real-time data and event tracking empower investors to make informed decisions, distinguishing between rhetorical calming and the tangible shifts in supply, demand, and inventory that truly drive market direction.