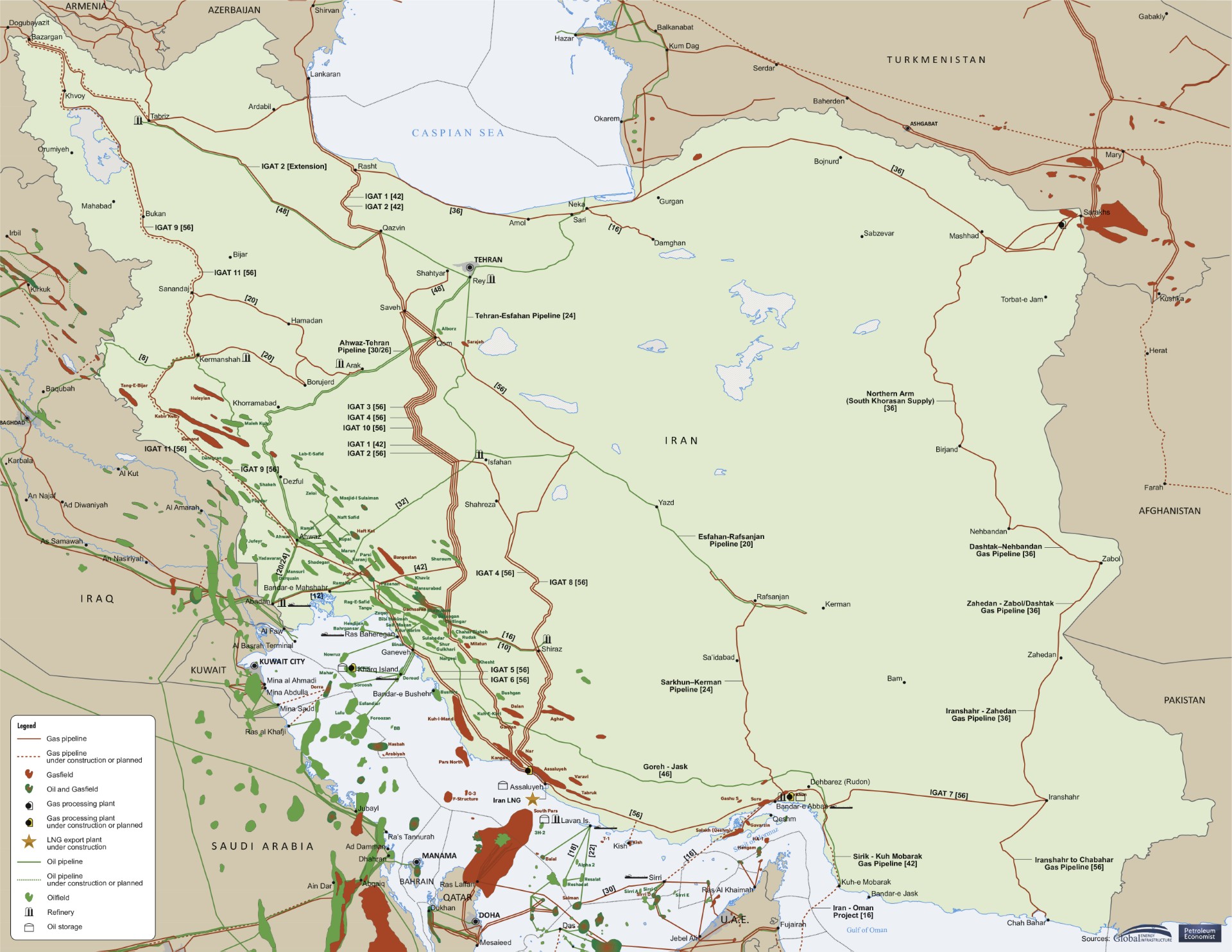

The global oil and gas landscape is once again gripped by heightened geopolitical tensions, with escalating conflict in the Middle East sending shockwaves through energy markets, particularly across Asia. The recent widening of hostilities, sparked by U.S. and Israeli actions against Iran, has brought critical shipping lanes under severe threat, most notably the Strait of Hormuz. This narrow yet vital waterway, through which a significant portion of the world’s crude oil and refined products flows, has seen traffic severely disrupted, creating an immediate and profound supply crunch for key Asian economies. Investors are keenly watching how this disruption translates into sustained price movements and shifts in regional energy security, demanding a clear understanding of both immediate market reactions and forward-looking implications.

The Strait of Hormuz Bottleneck and Asia’s Immediate Supply Shock

The direct impact of the Mideast conflict on energy trade has been swift and severe, especially for nations heavily reliant on Middle Eastern crude and products. The effective halt of traffic through the Strait of Hormuz has created an unprecedented logistical challenge. In Singapore, the world’s premier bunkering port, shipping fuel suppliers are reportedly fulfilling only partial orders, citing drastically reduced incoming volumes. This bottleneck extends beyond crude, affecting various refined products and feedstocks critical to Asian industries. South Korean petrochemical producer Yeochun NCC, for instance, has declared force majeure on certain sales due to significant delays in naphtha feedstock arrivals. These real-time disruptions underscore the precariousness of global energy supply chains and Asia’s disproportionate vulnerability to Middle Eastern instability.

Market Dynamics Amidst Supply Fears: A Closer Look at Crude Prices

Despite the severe supply constraints emerging from the Middle East, the immediate reaction in benchmark crude prices has been nuanced. As of today, Brent crude trades at $93.04, reflecting a modest daily decrease of 0.21%, with its intraday range spanning $92.57 to $94.21. Similarly, WTI crude stands at $89.43, down 0.27%, moving between $88.76 and $90.71 today. However, this recent daily stability masks a more significant trend over the past two weeks. Brent, for example, has seen a notable decline from $101.16 on April 1st to $94.09 just yesterday, marking a 7% drop. This divergence—a recent downtrend despite escalating conflict—highlights a complex interplay of factors. While the physical market is tightening in Asia, broader macroeconomic concerns, potential demand destruction, and perhaps the market’s assessment of the conflict’s duration or the effectiveness of alternative supply routes may be tempering a more dramatic price surge. Investors are clearly attempting to balance immediate geopolitical risk against longer-term demand outlooks, leading to increased volatility.

Asia’s Reactive Measures: Export Cuts, SPRs, and Potential Rationing

The escalating energy crunch is forcing Asian governments and industries to implement drastic measures to secure domestic supplies. China, the world’s largest oil importer and Asia’s third-largest fuel exporter, has instructed its major refiners to halt exports of diesel and gasoline. This directive includes canceling existing shipments and refraining from new contracts, signaling a clear prioritization of domestic energy security over export revenue. Japan, which procures approximately 90% of its crude from the Middle East, is now considering tapping its strategic petroleum reserves (SPRs) to alleviate the strain, with refiners actively lobbying the government for releases. Even more critically, nations like India, heavily reliant on Middle Eastern liquefied petroleum gas (LPG) for cooking, are in urgent talks with producers to mitigate dwindling supplies, with few viable alternatives given the distance of U.S. cargoes. The situation is so dire in some areas that governments, such as Bangladesh, are preparing to reduce deliveries to petrol pumps and asking citizens to curtail non-essential travel, hinting at potential rationing scenarios across the region. These actions reflect the profound and immediate impact of disrupted Mideast supply on everyday life and economic stability.

Investor Outlook: Navigating Volatility and Forward Catalysts

Our proprietary reader intent data reveals a consistent theme this week: investors are grappling with significant uncertainty regarding crude price direction. Many are asking “is WTI going up or down?” and seeking predictions for “the price of oil per barrel by end of 2026.” This reflects a market searching for clarity amidst conflicting signals. The ongoing Mideast tensions are undeniably bullish for crude, yet recent price weakness suggests other factors are at play. For the immediate term, investors should closely monitor upcoming data releases. The EIA Weekly Petroleum Status Reports, scheduled for April 22nd and April 29th, will provide critical insights into U.S. inventory levels, refining activity, and demand indicators, offering a domestic counterpoint to the international supply concerns. Further out, the May 2nd EIA Short-Term Energy Outlook will be particularly influential, as it will incorporate the latest geopolitical developments into its projections, potentially guiding expectations for prices through the remainder of 2026. These reports, alongside the Baker Hughes Rig Count on April 24th and May 1st, will offer a comprehensive picture of both supply-side activity and demand trends, helping investors calibrate their positions in what remains a highly volatile and geopolitically charged market.