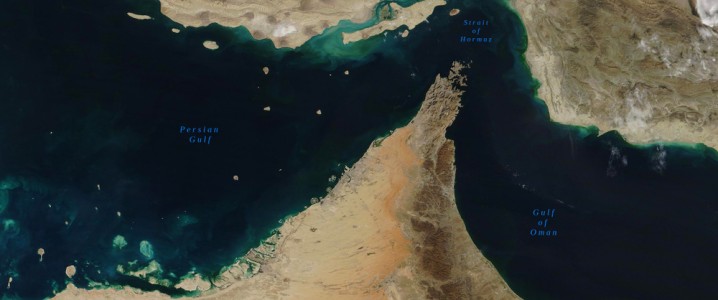

The Strait of Hormuz, a narrow choke point through which a staggering one-fifth of global oil supply normally passes, is once again at the epicenter of escalating geopolitical tensions. Recent declarations by Iran’s Islamic Revolutionary Guard Corps (IRGC) asserting “complete control” over this vital waterway, coupled with fresh attacks on commercial vessels, have sent ripples of concern through global energy markets. For oil and gas investors, this isn’t merely a news headline; it’s a critical development that demands immediate and thorough analysis of its potential impact on supply security, crude prices, and investment strategies. While the immediate market reaction might seem counterintuitive, the underlying risks are profound and warrant close attention as we navigate a volatile landscape.

Hormuz Tensions Escalate: A Critical Supply Chokepoint Under Threat

The IRGC’s audacious claim of full control over the Strait of Hormuz, as conveyed through Iranian state media on Wednesday, injects a dangerous new dynamic into an already fraught region. This declaration follows disturbing reports of new attacks on commercial shipping lanes critical to the Gulf’s energy exports. In one incident, a vessel operating approximately 137 nautical miles east of Muscat reported a nearby explosion on Tuesday evening. Hours later, a tanker near the Emirati port of Fujairah, roughly seven nautical miles offshore, sustained minor damage from an unidentified projectile. While both incidents thankfully resulted in no major injuries or significant damage, they are stark reminders of the vulnerability of maritime trade in the region. The Strait of Hormuz is not just a shipping lane; it’s a geopolitical flashpoint responsible for the transit of about 20 million barrels per day of crude and petroleum products. The intensifying conflict involving the U.S., Israel, and Iran directly threatens this indispensable corridor, leading maritime authorities to issue heightened alert warnings for vessels operating in the area. Ship-tracking data has already indicated a slowdown in tanker movements, with shipping analytics firms like Clarksons Research estimating thousands of vessels remain idle across the Gulf as operators meticulously assess the escalating security risks.

Market Disconnect? Prices Retreat Despite Geopolitical Premium

Given the severe supply implications of a disrupted Strait of Hormuz, one might expect a dramatic surge in crude prices. Yet, our live market data reveals a more nuanced picture. As of today, Brent Crude trades at $90.38, while WTI Crude is at $82.59. Gasoline prices stand at $2.93 per gallon. This current price point for Brent represents a significant retreat from the $112.78 seen on March 30th, marking a nearly 20% decline in just over two weeks. This raises a crucial question that many investors are asking: “Is WTI going up or down?” and “What do you predict the price of oil per barrel will be by the end of 2026?” The immediate market reaction suggests that while the geopolitical risk is acknowledged, other factors may be exerting stronger downward pressure. This could include broader macroeconomic concerns, demand fears, or the market potentially underestimating the duration and severity of any future supply disruptions. Investors appear to be balancing the immediate, tangible threat of supply cuts against a potentially weaker global demand outlook. However, this apparent market “disconnect” could quickly resolve if a significant, sustained disruption in the Strait materializes, pushing prices sharply higher as the true geopolitical premium is finally priced in.

Upcoming Events to Watch: OPEC+ and Inventory Data

The coming two weeks are packed with critical energy events that will shape investor sentiment, especially against the backdrop of heightened Hormuz tensions. On Monday, April 20th, the OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting will convene. This will be followed by the full OPEC+ Ministerial Meeting on Saturday, April 25th. These gatherings are crucial. Against the backdrop of potential supply disruptions from the Middle East, OPEC+ members will be assessing global supply-demand balances. Will the increased geopolitical risk encourage them to maintain or even deepen existing production cuts to support prices, or might the potential for a severe supply shock prompt discussions about market stability and potentially even a cautious increase in output if the situation escalates? Their decisions will be heavily scrutinized. Furthermore, weekly inventory data from the American Petroleum Institute (API) on April 21st and April 28th, and the official EIA Weekly Petroleum Status Reports on April 22nd and April 29th, will provide critical insights into U.S. supply-demand dynamics. Alongside the Baker Hughes Rig Count on April 24th and May 1st, these reports offer a snapshot of North American production and consumption, which could either alleviate or exacerbate fears stemming from the Middle East. Unexpected inventory builds could temper price hikes, while drawdowns would amplify concerns.

Navigating the Investment Landscape: Risk and Opportunity

For oil and gas investors, the current environment demands a blend of vigilance and strategic foresight. The Strait of Hormuz situation introduces an undeniable “geopolitical risk premium” that, while not fully reflected in current prices, remains a potent latent force. While isolated voyages, such as the tanker Pola recently transiting the strait, demonstrate that movement hasn’t ceased entirely, the mere *threat* of disruption significantly impacts shipping insurance rates and operational costs for energy companies. Investors must evaluate their portfolios for exposure to companies with significant operations or transport routes reliant on the Gulf. The question of “what the price of oil per barrel will be by the end of 2026” becomes exponentially more complex, as this geopolitical wild card can swiftly redraw supply-demand models. Companies with diversified asset bases, robust logistical capabilities, or strong domestic production in less volatile regions may offer a degree of insulation. Conversely, the potential for a sustained supply shock could drive significant upside for pure-play upstream producers, albeit with corresponding increases in risk. Monitoring diplomatic efforts, military posturing, and the rhetoric from all involved parties will be as critical as tracking market fundamentals in the weeks and months ahead.