The global energy market stands at a precarious crossroads, with escalating tensions in the Middle East casting a long shadow over critical supply lines for both crude oil and liquefied natural gas (LNG). Recent analyses underscore the fragility of these flows, particularly concerning the Strait of Hormuz and Iran’s export infrastructure, suggesting that while a geopolitical risk premium is already embedded in current prices, the true cost of a significant disruption could be far more severe. Investors must brace for heightened volatility and potential price spikes, as the market’s current trajectory may not fully reflect the acute vulnerabilities that could materialize with further escalation.

The Hormuz Chokepoint: Global Energy’s Achilles’ Heel

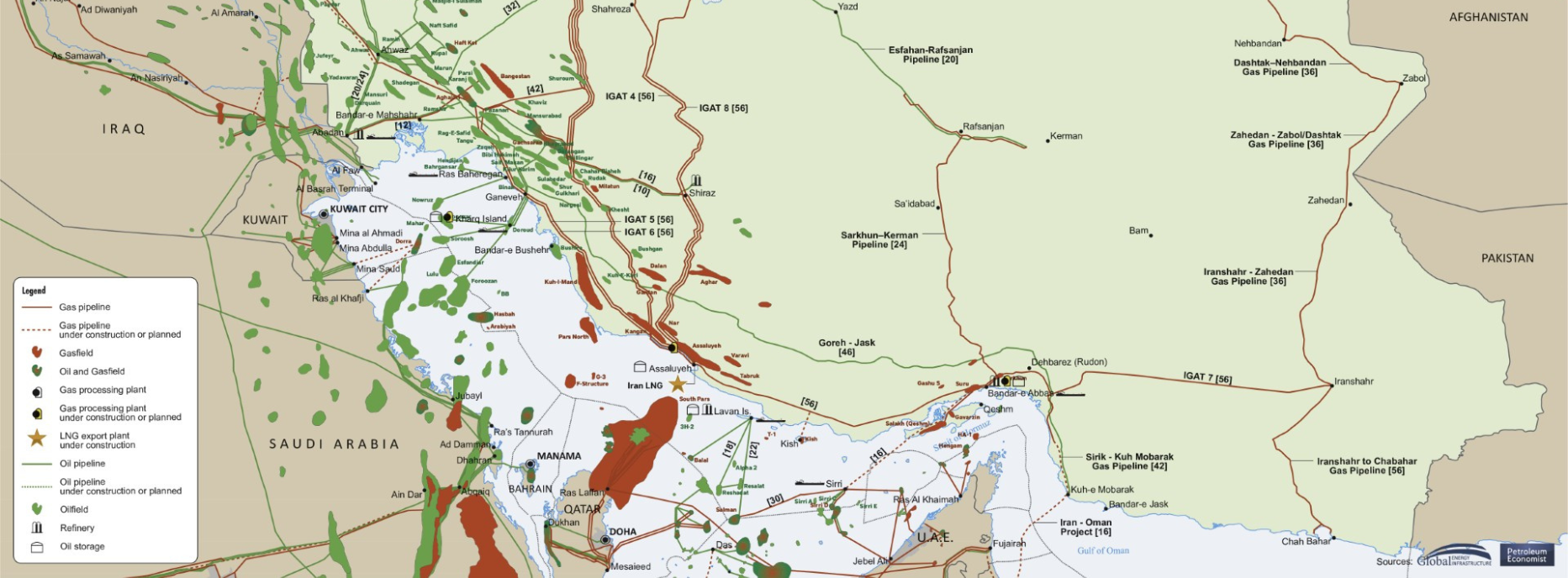

The Strait of Hormuz represents an irreplaceable artery for global energy trade, funneling an astonishing 14 million barrels per day (MMbpd) of crude oil – roughly one-third of all seaborne supply – along with an estimated 20% of global LNG volumes. This concentration of critical infrastructure in a politically volatile region creates an inherent and formidable risk. Industry analysis suggests that even a temporary, one-month closure of this vital passage could trigger a massive draw of approximately 400 million barrels from global inventories. Such a scenario would swiftly deplete the existing, albeit modest, market surplus and ignite a fierce scramble among importers, inevitably driving prices significantly higher as nations compete for rapidly diminishing prompt supply.

Iranian Export Risks and Current Market Dynamics

Beyond the Strait itself, the potential for direct disruption to Iranian crude exports presents another substantial threat. Reports of damage near Kharg Island, a key export terminal, highlight the vulnerability of approximately 2 MMbpd of Iranian crude. Should this terminal face an extended outage, market intelligence indicates Brent crude prices could surge by an additional $10 to $15 per barrel above prior forecasts. As of today, Brent Crude trades at $90.38 per barrel, reflecting a complex interplay of geopolitical fears and broader macroeconomic factors. While this price point suggests a geopolitical premium is already present, it’s crucial to note the recent trend. Our proprietary data indicates Brent has actually seen a significant decline, from $112.78 on March 30th to its current $90.38 on April 17th – a drop of nearly 20% in just two weeks. This divergence suggests that despite the clear and present dangers outlined by analysts, other bearish influences or a perceived lack of immediate escalation might be causing the market to currently underprice the full extent of this geopolitical risk. Investors should recognize this potential disconnect: the market might be complacent, leaving significant upside exposure if the situation deteriorates rapidly from current levels rather than from a lower, pre-tension baseline.

LNG Markets: A Precedent for Rapid Price Adjustment

The liquefied natural gas (LNG) market offers a stark illustration of how quickly supply shocks translate into price volatility. Recent disruptions linked to QatarEnergy, affecting an estimated 10-11 billion cubic feet per day (Bcf/d) – roughly one-fifth of global LNG trade – sent immediate ripples through the market. The Japan-Korea Marker (JKM) price, a key benchmark for Asian LNG, nearly doubled in response to these developments. This rapid and dramatic price surge underscores the inherent inelasticity of short-term LNG supply. Unlike crude oil, where strategic reserves and marginal production increases can offer some buffer, LNG infrastructure requires significant lead times for expansion. Consequently, in the face of multi-Bcf/d supply shocks, the market is compelled to absorb the adjustment primarily through price hikes rather than volume shifts. For investors, this means that while the oil market grapples with potential future disruptions, the LNG sector has already demonstrated its extreme sensitivity, setting a precedent for what could unfold with further regional instability affecting gas flows.

Navigating Uncertainty: Investor Outlook and Upcoming Catalysts

The current landscape naturally raises critical questions for our readers, echoing the sentiment of “is WTI going up or down?” and “what will oil prices be by end of 2026?” Our proprietary intent data shows a clear focus on price direction and long-term forecasts amidst this uncertainty. Indeed, WTI Crude, currently at $82.59 per barrel, has seen an intraday range of $78.97 to $90.34 today, highlighting the extreme volatility investors are already grappling with. While geopolitical price spikes have historically been temporary, the current context presents unique challenges. OECD crude and product inventories, though above five-year averages, could erode quickly under sustained disruption. Moreover, the U.S. Strategic Petroleum Reserve remains approximately 200 million barrels below 2018 levels, significantly limiting its flexibility compared to previous crises.

Looking forward, several key events in the next two weeks will offer crucial insights into market sentiment and potential supply responses. The OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting on April 20th, followed by the full OPEC+ Ministerial Meeting on April 25th, will be critical. Any signals regarding production policy in response to rising geopolitical risks or inventory trends could significantly influence investor confidence. Furthermore, the weekly API and EIA crude inventory reports (April 21st, 22nd, 28th, 29th) will provide real-time data on supply-demand balances, while the Baker Hughes Rig Count (April 24th, May 1st) will offer clues on future production trajectories. Investors should closely monitor these events for any indication of how producers plan to react to or mitigate potential supply shocks, which will be paramount in shaping the trajectory of crude prices through the remainder of 2026. Given the acute geopolitical risks, elevated near-term volatility, widening time spreads, and increased insurance costs are likely to persist as Asian importers, in particular, compete fiercely for prompt supply, making a clear “up or down” prediction for WTI incredibly challenging in the short term, and tying the 2026 outlook closely to the ongoing geopolitical narrative.