As the energy landscape continues its dynamic evolution, investors in the oil and gas sector are increasingly scrutinizing the long-term viability and strategic positioning of decarbonization technologies. Among these, Carbon Capture and Storage (CCS) stands out, but the investment thesis is far from monolithic. The core question for astute investors is no longer a simple ‘yes or no’ on CCS, but rather where this technology delivers genuine and sustainable climate value, optimizing both environmental impact and financial returns in a world grappling with energy security and climate goals.

The Nuance of Carbon Capture: Beyond ‘Yes or No’

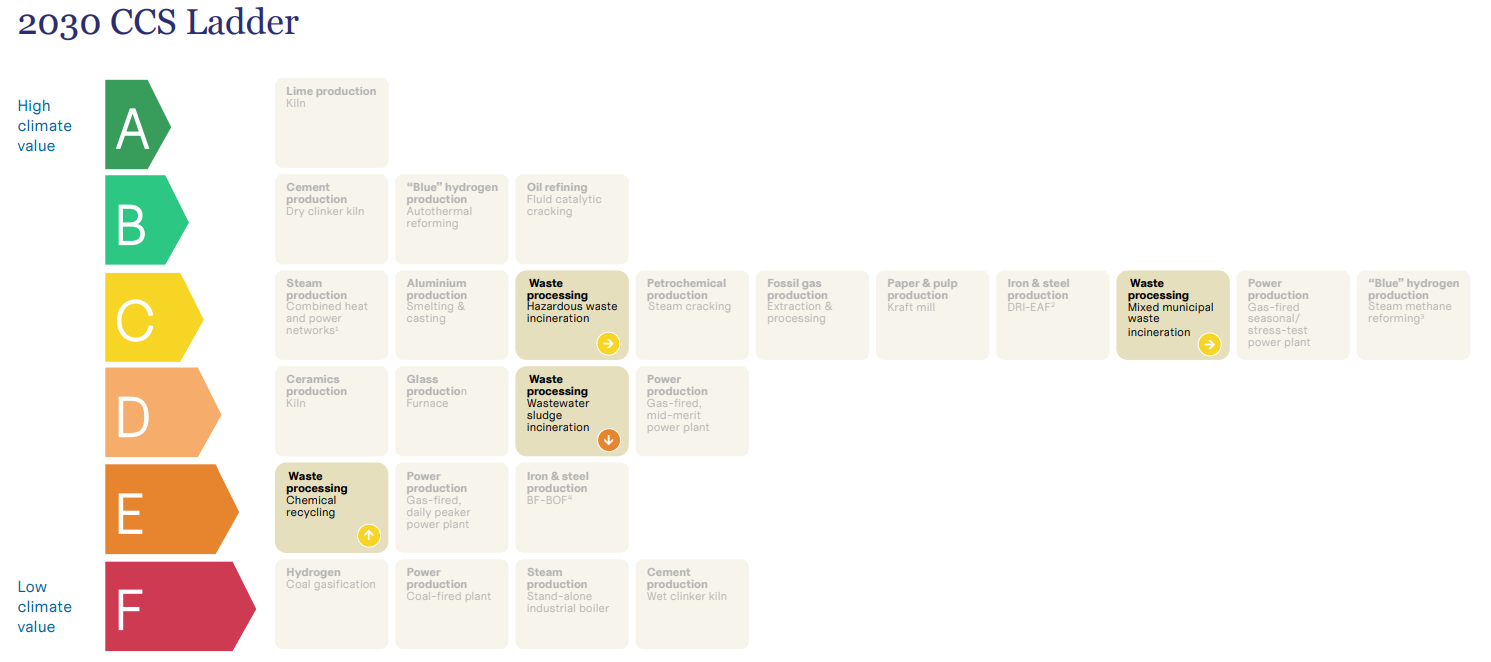

For too long, the discourse around Carbon Capture and Storage has been overly simplified, often leading to polarized views that obscure its true potential and limitations. Savvy investors understand that a more sophisticated framework is required to differentiate between high-impact applications and those where capital might be better deployed elsewhere. The latest analytical frameworks, such as the “CCS Ladder,” provide just this kind of granular insight, assessing applications across critical industrial sectors for their climate value in both 2030 and 2050.

This comprehensive evaluation hinges on three core criteria: the competitive landscape of alternative solutions, the sheer mitigation potential of CCS in a given process, and its overall feasibility from technical and economic standpoints. Experts like Domien Vangenechten, Programme Lead, EU Industry at E3G, emphasize that Europe’s industrial transformation necessitates such smart choices on CCS, ensuring every euro spent maximizes both climate and competitiveness gains. Similarly, Georg Kobiela, Policy Lead at Bellona Deutschland, points to the imperative of prioritizing CCS applications based on transparent, evidence-based climate benefit to efficiently deploy public funds and achieve maximum impact. This structured approach helps investors identify where CCS is truly indispensable, where it serves a crucial transitional role, and where its relevance naturally declines as other solutions prove superior.

Navigating Market Volatility: A Backdrop for CCS Investment

The strategic evaluation of long-term decarbonization technologies like CCS occurs against a backdrop of persistent energy market volatility. As of today, Brent crude trades at $93.86 per barrel, marking a significant 3.79% increase for the day. WTI crude also saw a strong rebound, reaching $90.22, up 3.2%. While these daily gains might signal short-term bullish sentiment, a broader look reveals the inherent unpredictability of the market. Over the past 14 days alone, Brent crude has seen a substantial decline, dropping from $118.35 on March 31st to $94.86 on April 20th, representing a nearly 20% depreciation. This sharp swing underscores the challenges investors face when projecting future energy prices and, by extension, the economic viability of energy-intensive projects.

Our proprietary reader intent data shows that investors are keenly focused on these price dynamics, with common queries ranging from “is WTI going up or down” to “what do you predict the price of oil per barrel will be by end of 2026?” This direct interest in future oil prices highlights the critical need for robust analysis that can withstand market fluctuations. Investing in CCS requires a long-term perspective, yet the ongoing volatility in crude prices directly influences the cost of operations, the competitiveness of fossil fuel-based industries, and the overall economic landscape in which decarbonization projects must thrive. Understanding where CCS provides durable value, irrespective of short-term price swings, becomes paramount for capital allocation.

High-Value Pillars and Shifting Sands: Where CCS Truly Shines

The detailed analysis of CCS applications reveals a crucial distinction between sectors where the technology is a permanent fixture and those where its role is temporary or diminishing. For investors, identifying these “high-value” pillars is key to making informed decisions. CCS remains critical for hard-to-abate industrial sectors such as lime and, to a lesser extent, cement production. In these industries, process emissions resulting from limestone decomposition have extremely limited viable alternatives. Consequently, the climate value of CCS in these areas is assessed as high and stable, extending through 2050, making them compelling targets for sustained investment.

Conversely, the power sector presents a different picture. Here, the value of CCS is seen as low and decreasing. The rapid advancements and scaling of renewable energy sources, coupled with cost-effective energy storage solutions and enhanced grid flexibility, are delivering deeper emissions cuts at significantly lower costs. This makes CCS in power generation a less attractive proposition compared to the accelerating deployment of renewables. Between these two extremes lie “variable-value” sectors like waste processing and hydrogen production. The role of CCS here is dynamic, influenced by factors such as residual emissions, shifts in demand, and broader system dynamics. While alternatives like circularity, advanced recycling, and renewable hydrogen show immense scaling potential, they also face economic, infrastructure, and deployment uncertainties, creating a complex investment landscape where careful, ongoing evaluation is essential.

Forward-Looking Catalysts: Upcoming Events and Long-Term Outlook for Decarbonization

Understanding the immediate and medium-term catalysts in the energy market is crucial for investors positioning their portfolios for the future of decarbonization. The coming days and weeks are packed with events that will shape the energy outlook, indirectly influencing the investment thesis for CCS. Today, April 21st, marks an OPEC+ JMMC Meeting, which will provide vital signals on global crude supply strategies. Any decisions on production adjustments will have direct implications for crude prices and, by extension, the financial health of the very industries considering CCS investments.

Beyond immediate supply-side news, the EIA Weekly Petroleum Status Reports on April 22nd and April 29th will offer critical insights into U.S. inventory levels and demand trends. Further out, the EIA’s Short-Term Energy Outlook (STEO) on May 2nd is particularly significant. This report provides comprehensive forecasts for energy markets, encompassing crude oil, natural gas, and renewables. For investors considering CCS, the STEO’s projections on future energy prices, policy environments, and the competitive landscape for other decarbonization technologies will be instrumental. A clear understanding of these forecasts helps investors gauge the long-term economic viability and strategic imperative of CCS projects, especially in light of reader questions concerning the “price of oil per barrel by end of 2026.” While these events primarily focus on traditional energy markets, their ripple effects on capital allocation, policy incentives, and overall industry sentiment are profound for the evolving CCS investment landscape.

The future of Carbon Capture and Storage as an investment vehicle is undeniably complex, demanding a sophisticated, data-driven approach. Investors must look beyond generalized narratives and instead focus on the specific, high-value applications where CCS delivers indispensable climate benefit, particularly in hard-to-abate industrial sectors like cement and lime. Navigating this landscape requires not only an understanding of the intrinsic value proposition of CCS but also a keen awareness of broader energy market dynamics, including current price volatility and upcoming catalytic events. By combining proprietary market insights with forward-looking analysis of policy and technological shifts, investors can strategically allocate capital to capitalize on the nuanced, yet significant, opportunities within the evolving decarbonization economy.