The Geopolitical Shift and its Market Ramifications

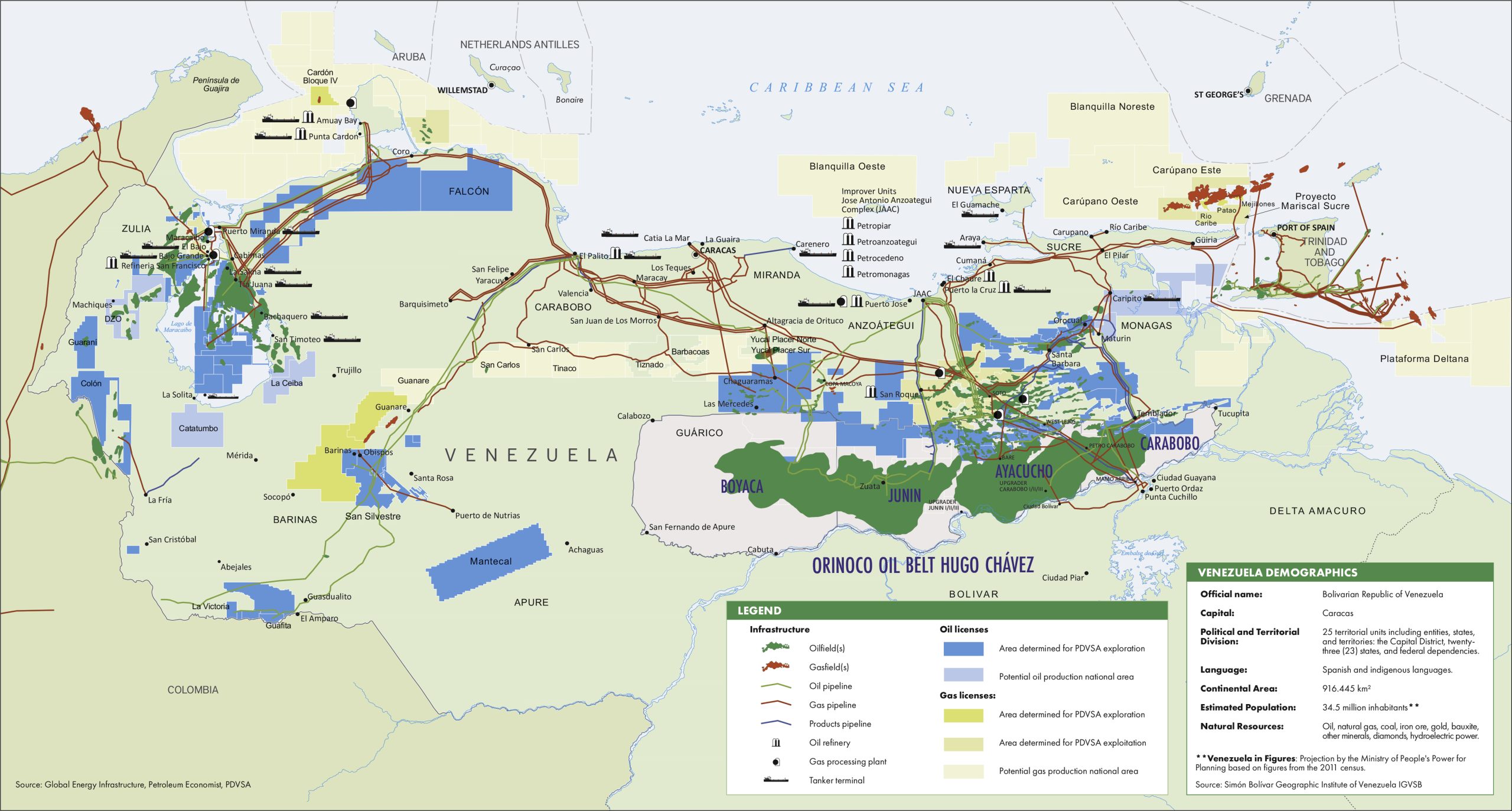

The global energy landscape is currently undergoing a subtle but potentially transformative shift, with significant attention now focused on Venezuela’s vast oil reserves. Following the recent capture of Venezuelan President Nicolás Maduro, the U.S. government has signaled a renewed openness for American oil majors to re-engage with the country’s beleaguered energy sector. U.S. Energy Secretary Chris Wright confirmed extensive discussions with executives from major players like ConocoPhillips, ExxonMobil, and Chevron Corp., indicating a strong appetite for re-entry. Chevron, notably the sole U.S. major maintaining operations in Venezuela, is already poised for a rapid ramp-up, with expectations for others to follow suit. This development arrives at a critical juncture for crude markets. As of today, Brent crude trades at $90.34, registering a slight decline of 0.1%, while WTI crude sits at $86.97, down 0.51%. This current market stability, however, masks significant volatility over the past two weeks, during which Brent crude experienced a nearly 20% drop, falling from $118.35 on March 31st to $94.86 just yesterday. Such price swings underscore the market’s sensitivity to supply-side news, making the prospect of revitalized Venezuelan production an increasingly compelling topic for investors.

Navigating the Investment Landscape: Billions at Stake

For US oil majors, returning to Venezuela presents both immense opportunity and formidable challenges. The country holds some of the world’s largest proven oil reserves, but its production capacity has been crippled by years of underinvestment, mismanagement, and corruption under the previous regime. The U.S. Energy Secretary, Chris Wright, has been in constant communication with executives from Exxon, Chevron, and ConocoPhillips since Maduro’s apprehension, noting a surge of interest from dozens of American firms. However, companies are proceeding with caution. Both Exxon and ConocoPhillips previously operated in Venezuela, only to have their assets nationalized by former President Hugo Chávez in the mid-2000s. This history casts a long shadow, making guarantees of “physical and financial security” paramount before committing the “tens of billions of dollars” required to truly revitalize the industry over the next decade. Our proprietary reader intent data reveals a consistent investor concern regarding future oil price stability, with many actively asking about the short-term direction of WTI and long-term forecasts for crude prices through 2026. The willingness of majors to deploy significant capital in Venezuela will hinge directly on their confidence in a stable, predictable operational and fiscal environment, mitigating the substantial political and operational risks inherently linked to such large-scale, long-term investments.

Venezuela’s Production Potential and Global Supply Impact

The re-entry of US majors into Venezuela could dramatically alter global crude supply dynamics. With its immense heavy crude reserves, a revitalized Venezuelan oil sector, supported by Western technology and capital, could add significant barrels to the global market. While the initial ramp-up would likely be gradual, the long-term potential for increased output from PDVSA, Venezuela’s national oil company, is substantial. This potential comes at a critical juncture for global energy markets. Investors will be closely monitoring the upcoming OPEC+ Joint Ministerial Monitoring Committee (JMMC) Meeting on April 21st, where member nations will reassess market conditions and potentially adjust production quotas. Any clear indications of substantial new Venezuelan output could influence OPEC+’s decisions, potentially offsetting efforts to tighten supply or providing a cushion against unexpected demand surges. Further insights into the overall health of the energy market will arrive with the EIA Weekly Petroleum Status Reports on April 22nd and April 29th, offering a detailed look at US inventory levels and demand trends. These reports, alongside the Baker Hughes Rig Count on April 24th and May 1st, will provide crucial context, allowing investors to gauge how a Venezuelan recovery might interact with prevailing demand and US domestic production.

Strategic Implications for US Majors and Investor Outlook

For US oil majors, particularly ExxonMobil and ConocoPhillips, a return to Venezuela represents a chance to reclaim lost assets and capitalize on a resource base that remains largely undeveloped. Such a move could bolster their long-term production profiles, diversify their portfolios, and potentially lower their finding and development costs compared to frontier regions. The U.S. Energy Secretary Chris Wright’s observation that his phone is “blowing up” with interest from dozens of American firms underscores the broad strategic importance of this opening. From an investor perspective, the immediate impact on stock prices will likely be muted, given the long lead times for significant production increases. However, the prospect of future cash flows and reserve additions will be factored into valuations. Investors should closely watch for concrete announcements regarding investment frameworks, production sharing agreements, and, crucially, the stability of the post-Maduro government. The White House meeting between President Donald Trump and oil executives slated for Friday could provide further clarity on the U.S. administration’s policy support and the path forward. While gasoline prices currently sit at $3.05, up 0.33% today, the broader implications of Venezuelan crude re-entering the market will have a more profound, long-term effect on global benchmark prices and the strategic positioning of the majors. This is a multi-year play, demanding patience and a keen eye on both geopolitical developments and the operational progress within Venezuela.