The global oil and gas industry finds itself at a pivotal juncture, navigating intense market volatility alongside an accelerating imperative for decarbonization. While traditional hydrocarbon production remains central to the world’s energy mix, strategic investments in carbon capture, utilization, and storage (CCUS) are rapidly emerging as a critical avenue for value creation and risk mitigation. This isn’t just about environmental compliance; it’s about securing future revenue streams, attracting capital in an ESG-conscious landscape, and ensuring the long-term viability of industrial assets. For investors, understanding the technological advancements and market dynamics within CCUS is crucial to identifying the next generation of energy leaders.

Advanced Carbon Capture: A Deep Dive into Technological Maturity

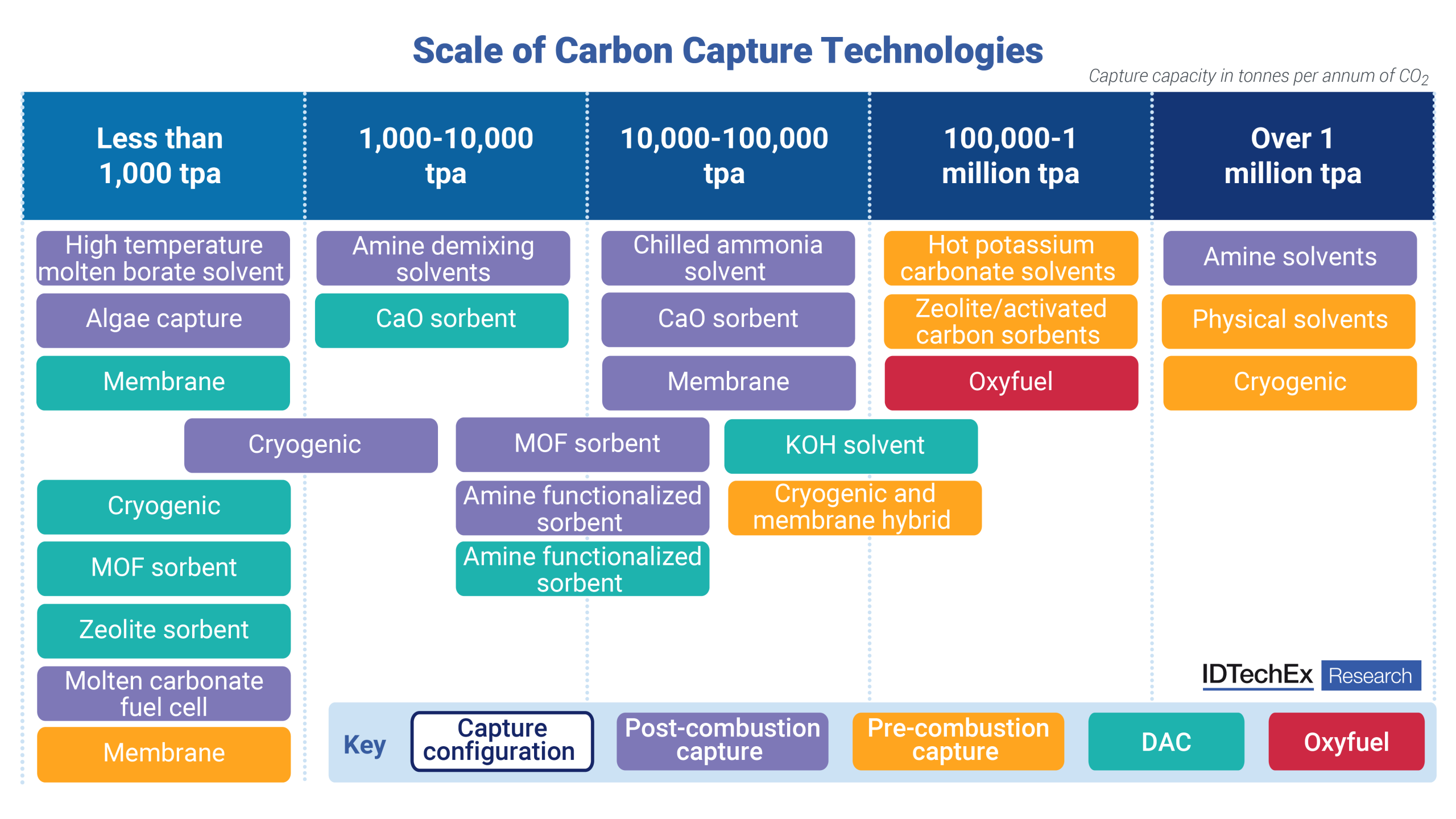

The foundational technology for post-combustion carbon capture, particularly in sectors like natural gas processing and potentially power generation, steelworks, and cement plants, centers on amine solvent systems. These established methods leverage strong chemical bonds to efficiently separate CO2 from flue gases, offering high absorption capacity and selectivity. Industry leaders such as Mitsubishi Heavy Industries, Shell, and SLB Capturi are deploying advanced, often proprietary, amine blends designed to reduce regeneration energy penalties and enhance absorption efficiency. These innovations are critical for driving down the operational costs associated with large-scale carbon removal, making it a more economically viable solution for heavy industry.

Beyond traditional amines, the pursuit of cost reduction is spurring significant R&D. Water-lean amine solvents, being developed by entities like ION Clean Energy and Pacific Northwest National Laboratory, aim to improve energy efficiency by reducing the specific heat required for solvent regeneration. Another compelling innovation is biphasic amine demixing, commercialized by firms such as Axens and CarbonOro. This technology allows the solvent to separate into two phases post-capture, meaning only the CO2-rich phase requires regeneration, substantially cutting energy demand. On the equipment front, companies like Baker Hughes and Carbon Clean are enhancing mass transfer through solutions like rotating packed beds, which reduce the physical footprint and capital cost of absorber columns by utilizing centrifugal force over gravity for gas-liquid contact. These advancements underscore a mature yet highly dynamic technological landscape, ripe for further investment and deployment.

Market Volatility Reinforces the CCUS Imperative

The current macro environment for crude oil underscores the urgency for diversification and long-term strategic planning. As of today, Brent Crude trades at $90.38 per barrel, marking a significant 9.07% decline within a single trading day, with its range fluctuating between $86.08 and $98.97. Similarly, WTI Crude has fallen to $82.59, down 9.41% today, experiencing a daily range of $78.97 to $90.34. This sharp downturn is not an isolated event; the 14-day trend for Brent shows a steep decline from $112.78 on March 30th to its current level, representing a nearly 20% erosion of value. Such dramatic price swings highlight the inherent volatility of commodity markets and the need for energy companies to build resilience beyond mere production volumes.

In this context, investments in CCUS are not just about environmental stewardship; they are a strategic hedge against future carbon pricing mechanisms and a means to future-proof existing assets. By enabling decarbonization without necessitating deindustrialization, CCUS allows heavy industries, many of which are O&G customers or even integrated players, to continue operations in a carbon-constrained world. This creates a new avenue for revenue and service provision, offering a more stable earnings profile that can withstand the cyclical nature of crude oil prices. For investors, this translates into a compelling argument for allocating capital to companies demonstrating a robust CCUS strategy, mitigating exposure to purely commodity-driven returns.

Upcoming Catalysts and Forward-Looking Investor Strategies

The immediate future holds several key events that will shape the traditional oil market, indirectly influencing the strategic importance of CCUS investments. The OPEC+ Joint Ministerial Monitoring Committee (JMMC) Meeting on April 19th, followed by the full OPEC+ Ministerial Meeting on April 20th, are critical. Investors are keenly watching for any signals regarding production quotas, which directly impact global supply and, consequently, crude prices. Given the recent steep decline in Brent and WTI, any indication of supply tightening could provide a floor, while an unchanged stance might exacerbate downward pressure. Following these, the API Weekly Crude Inventory reports on April 21st and 28th, and the EIA Weekly Petroleum Status Reports on April 22nd and 29th, will offer vital insights into demand dynamics and U.S. inventory levels. These reports often trigger short-term market reactions, creating both opportunities and risks.

Against this backdrop of imminent supply-demand news, the forward-looking investor is also considering the broader trajectory of energy markets. While immediate attention is on price movements, the long-term value proposition lies in companies that can adapt. A strong CCUS portfolio signals a company’s commitment to the energy transition, potentially making it more attractive to institutional investors with ESG mandates. We anticipate that companies with demonstrable progress in CCUS will increasingly differentiate themselves, even amidst commodity price volatility. This strategic foresight becomes a powerful narrative for long-term growth, regardless of short-term crude market gyrations.

Addressing Investor Questions: Value Creation Beyond the Barrel

Our proprietary reader intent data reveals a keen focus among investors on traditional market fundamentals. Questions like “What do you predict the price of oil per barrel will be by end of 2026?” and “What are OPEC+ current production quotas?” dominate discussions, underscoring a primary concern with crude prices and supply-side management. Furthermore, specific queries about company performance, such as “How well do you think Repsol will end in April 2026?”, indicate a desire to understand how individual firms navigate the current environment.

While these questions are valid, a complete investment thesis for the modern oil and gas sector must extend beyond the barrel. CCUS directly addresses the implicit question of how energy companies will generate value in a decarbonizing world. For a company like Repsol, or any integrated energy major, investing in CCUS technologies means not only reducing their own operational emissions but also opening up new service markets for industrial decarbonization. It’s about securing future permits, avoiding potential carbon taxes, and ultimately creating new revenue streams from carbon capture and storage credits. These investments transform an environmental liability into a tangible asset, providing a crucial element of stability and growth that may not be fully captured by short-term oil price forecasts. The ability to offer decarbonization solutions positions these companies as integral players in the broader energy transition, appealing to a wider pool of capital and building a more resilient business model for the future.