The International Maritime Organization’s (IMO) decision to postpone the adoption of its Net-Zero Framework (NZF) for an additional year sends ripples across the global energy landscape, creating both uncertainty and strategic opportunities for oil and gas investors. While seemingly a delay in a niche regulatory sphere, its implications for shipping, fuel demand, and the broader energy transition are profound. This pause allows for a critical re-evaluation of the framework’s mechanisms, from clean fuel availability to carbon-trading dynamics, forcing investors to recalibrate their outlooks for maritime decarbonization and the associated capital allocation. For those tracking the pulse of the energy market, this isn’t just a bureaucratic hiccup; it’s a pivotal moment demanding a deeper dive into the structural challenges and potential pathways forward, all set against a backdrop of dynamic crude prices and looming geopolitical energy decisions.

The Regulatory Pause and its Market Implications

The IMO’s one-year delay in finalizing its Net-Zero Framework highlights significant underlying challenges in the push for maritime decarbonization. This isn’t merely about pushing back a deadline; it’s an acknowledgment of the framework’s current ambiguities, contentious elements, and the practical difficulties in implementation. For oil and gas investors, this extended timeline translates into continued regulatory uncertainty, impacting investment decisions in alternative fuels, shipbuilding technologies, and associated infrastructure. While some might view this as a setback for green initiatives, it also presents an opportunity for a more robust and pragmatic framework to emerge, potentially creating clearer investment signals in the future.

Amidst this regulatory recalibration, the broader energy market is experiencing notable shifts. As of today, Brent Crude trades at $90.38 per barrel, marking a significant 9.07% decline within the day, with its range fluctuating between $86.08 and $98.97. Similarly, WTI Crude stands at $82.59, down 9.41%, having traded between $78.97 and $90.34. This bearish sentiment extends to refined products, with gasoline prices currently at $2.93, down 5.18% today. This downward pressure on crude prices is not an isolated event; Brent has seen a substantial 19.9% drop from $112.78 just two weeks ago. Such market volatility, coupled with regulatory delays, underscores the complex environment in which energy transition investments are being weighed. Lower crude prices, while potentially easing immediate inflationary pressures, can also dampen the economic incentive for rapid adoption of higher-cost alternative fuels in the short term, pushing back the breakeven point for new decarbonization technologies.

The Clean Fuel Chasm: Availability and Infrastructure Bottlenecks

A critical revelation from expert analysis points to a substantial disparity between the projected availability of clean fuels and the targeted demand within the IMO’s initial framework. This gap, exacerbated by severe infrastructure constraints, casts a long shadow over the feasibility of the prescribed transition timeline. For investors, this is not just a theoretical problem; it represents concrete challenges and, conversely, specific investment opportunities. The question often posed by our readership, “How well do you think Repsol will end in April 2026?” reflects a broader investor interest in how integrated energy companies, with their refining capabilities and potential for alternative fuel production, are navigating this evolving landscape. Companies positioned to bridge this clean fuel supply gap, whether through advanced biofuels, green ammonia, or methanol production, stand to gain significantly.

However, the infrastructure challenge is equally daunting. Developing the necessary bunkering facilities, storage, and distribution networks for these new fuels requires massive capital expenditure and long lead times. Without adequate infrastructure, even abundant clean fuel production would remain bottlenecked. This bottleneck directly impacts the shipping industry’s ability to comply with future regulations and, by extension, the financial performance of maritime operators. Investors should be scrutinizing companies’ long-term capital allocation strategies, looking for those making tangible commitments to both alternative fuel production and the development of the supporting logistical backbone. The delay offers a window to address these fundamental limitations, but the scale of the investment required remains immense.

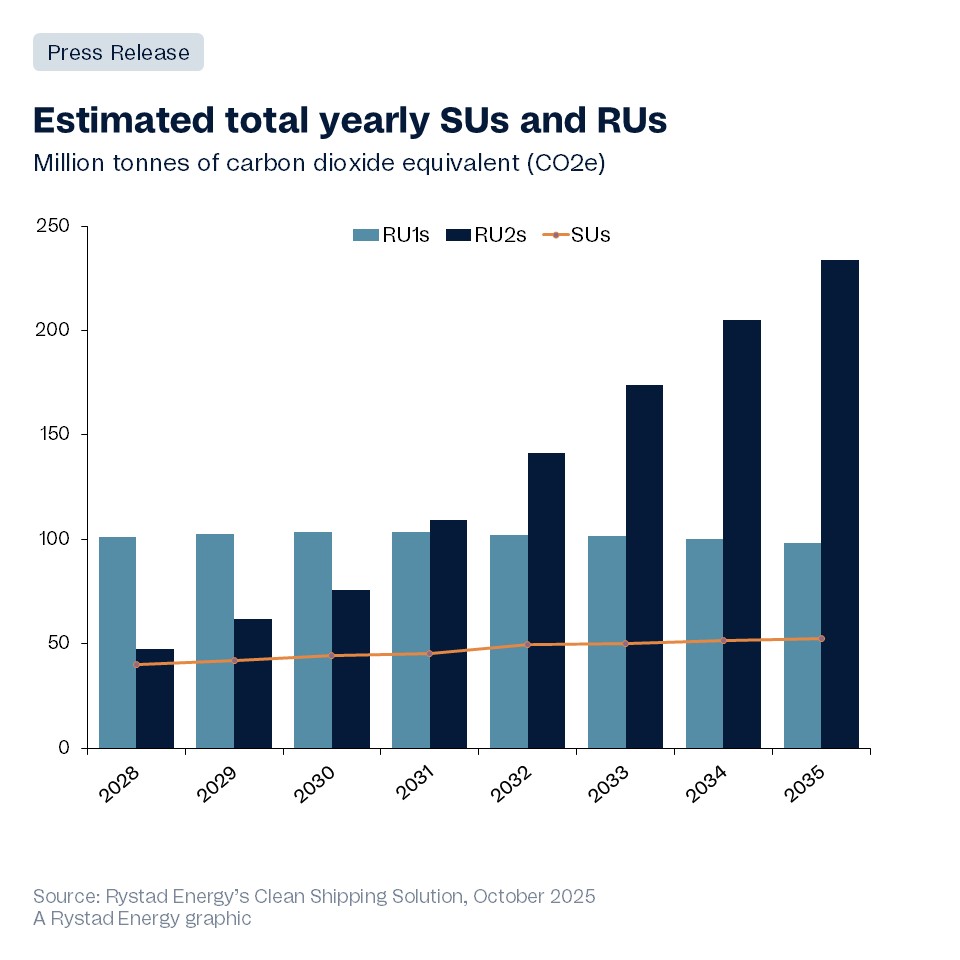

Carbon Credits: A Looming Supply Shortage and Price Surge

Perhaps one of the most immediate and impactful financial implications of the Net-Zero Framework, even in its delayed state, lies within its carbon-trading mechanism. Expert analysis reveals a persistent structural deficit in the availability of Tier II remedial unit offsets, expected to outstrip available surplus units through 2035. Under the proposed framework, vessels meeting direct targets generate Surplus Units (SUs), while non-compliant vessels generate Remedial Units (RUs), categorized as Tier I (meeting base target) or Tier II (not meeting base target). The critical issue arises because non-compliant vessels would need to acquire SUs to offset their Tier II RUs.

This anticipated imbalance, where demand for Tier II offsets significantly exceeds supply, is projected to drive trading prices sharply towards the Tier II penalty ceiling. For investors, this translates into a quantifiable increase in operating costs for a substantial portion of the global shipping fleet. Companies with older, less efficient vessels or those heavily reliant on conventional fuels will face escalating compliance expenses, directly impacting their profitability. Conversely, companies investing early in fuel efficiency or alternative-fuel vessels will not only avoid these penalties but could also generate valuable Surplus Units, creating a new revenue stream. This dynamic ties directly into broader investor concerns, such as “What do you predict the price of oil per barrel will be by end of 2026?” because the cost of carbon compliance will increasingly influence the economic viability of different fuel choices and overall energy demand projections for the maritime sector.

Strategic Horizons: What Investors Should Watch Next

The IMO’s extended timeline for its Net-Zero Framework aligns with a period of intense activity in the broader energy market, offering investors a critical window for strategic positioning. The delay provides member states an opportunity to refine the framework, potentially leading to a more realistic and actionable plan. For investors, the focus must now shift to anticipating these refinements and their potential impact on energy demand and supply. Key to this outlook are the upcoming OPEC+ meetings, with the JMMC scheduled for April 19th and the full Ministerial Meeting on April 20th. These gatherings are crucial for establishing production quotas and will undoubtedly influence global crude supply, which in turn affects the economic viability of alternative fuels and the impetus for decarbonization investments.

Our readership consistently inquires about “OPEC+ current production quotas,” underscoring the market’s sensitivity to these decisions. Any adjustments to quotas could significantly impact the prevailing crude price environment, influencing the cost-benefit analysis for shipping companies considering expensive transitions to cleaner fuels. Furthermore, the weekly API and EIA inventory reports on April 21st, 22nd, 28th, and 29th, alongside the Baker Hughes Rig Count on April 24th and May 1st, will provide granular insights into immediate supply-demand dynamics and drilling activity. Investors should closely monitor these indicators. A sustained period of lower crude prices, potentially influenced by OPEC+ decisions, might temporarily decelerate the transition to more expensive clean fuels, offering a reprieve for traditional fossil fuel infrastructure but intensifying the pressure on IMO to design a robust reward mechanism that truly incentivizes sustainable practices regardless of short-term market fluctuations.

Designing for Sustainable Returns: The Reward Mechanism

Beyond the penalties and offsets, the efficacy of the IMO’s Net-Zero Framework hinges critically on the design of its reward mechanism. Industry analysis emphasizes the need to prevent the framework from becoming a mere penalty-collection system. For long-term oil and gas investors, this aspect holds significant weight. A well-structured reward system – one that genuinely incentivizes sustainable practices, technological innovation, and early adoption of clean fuels – could unlock substantial capital for green maritime solutions. While the cost gap between conventional and clean fuels is expected to narrow as technology matures and economies of scale are achieved, proactive incentives are essential to accelerate this process.

Investors should be looking for signals that the refined NZF will incorporate tangible benefits for compliant vessels and companies that exceed targets, not just penalize those that fall short. This could manifest as preferred access to ports, reduced levies, or tradable credits with higher value. Such mechanisms would transform decarbonization from a pure cost burden into a competitive advantage and a source of sustainable returns. Companies actively lobbying for a robust reward system and demonstrating a clear pathway to leveraging such incentives are likely to be attractive long-term plays in the evolving energy and maritime landscape. The next year offers a crucial opportunity for the IMO to embed these principles, laying a foundation for a truly effective and equitable transition.