The Canadian oil and gas sector is once again a focal point for M&A activity, with Strathcona Resources Ltd. (“Strathcona”) amending and extending its unsolicited takeover bid for MEG Energy Corp. (“MEG”). This intensified strategic maneuver, offering MEG shareholders an all-share alternative to the previously announced Cenovus Energy Inc. deal, underscores a battle for control and differing visions for long-term value creation. For investors, the decision is now stark: crystallize value with a cash-heavy offer or embrace the potential upside of a combined, larger entity in a dynamic commodity market.

Strathcona’s Enhanced Offer: A Deeper Dive into Valuation

Strathcona’s revised proposal presents a compelling premium, moving the goalposts significantly for MEG shareholders. Under the terms of the Amended Offer, Strathcona proposes to acquire all outstanding MEG shares not already owned by its affiliates for 0.80 of a Strathcona common share per MEG share. This valuation, based on Strathcona’s volume-weighted average share price on September 5, 2025, equates to $30.86 per MEG share. This represents a substantial 11% premium over the agreement MEG had entered into with Cenovus on August 22, 2025, which was valued at $27.79 per MEG share at that same point. Furthermore, the Amended Offer itself reflects a 10% increase from Strathcona’s original bid of $28.02 per MEG share.

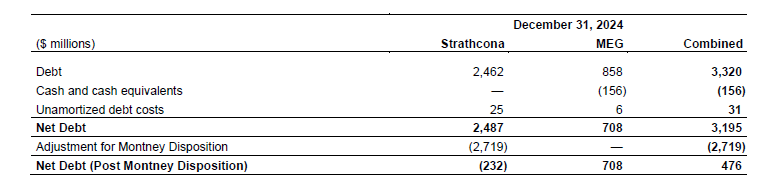

A critical component of Strathcona’s strategy involves a special distribution of $2.142 billion to all Strathcona shareholders in the fourth quarter. Should the Amended Offer succeed, this distribution would equate to approximately $5.22 per Strathcona share. However, if the offer is unsuccessful, existing Strathcona shareholders stand to receive a significantly higher $10.00 per share from this distribution. This structure incentivizes existing Strathcona shareholders while offering MEG shareholders an attractive entry point into a potentially larger, more diversified entity. Upon completion and payment of the special distribution, Strathcona projects approximately 410 million shares outstanding and $3.0 billion in net debt, translating to an estimated 1.1x Net Debt / EBITDA at US$60 WTI, signaling a robust post-transaction financial profile.

Investor Focus: Long-Term Vision Amidst Market Volatility

Amidst ongoing M&A discussions, investors are continuously evaluating fundamental market drivers and strategic positioning. We’ve observed heightened interest in understanding current commodity price movements and the underlying models powering those responses, as well as inquiries into OPEC+ production strategies. These questions directly reflect the environment in which major energy deals like the Strathcona-MEG proposal are being debated.

Strathcona and its largest shareholder, Waterous Energy Fund (WEF), are clearly articulating a long-term vision, positioning the all-share transaction as a means for MEG shareholders to retain significant future upside in their assets, unlike the cash-heavy Cenovus deal which Strathcona claims would limit MEG shareholders to only 4% of future gains through Cenovus ownership. WEF has publicly committed to a long-term view, even offering to enter into a lock-up agreement, directly countering claims made by the MEG board. This commitment from a major shareholder addresses potential investor concerns about post-merger share stability and signals confidence in the combined entity’s future performance. The proposed ownership structure post-deal, with existing MEG shareholders holding 43% of the combined Strathcona, further emphasizes this long-term alignment.

Navigating Current Market Headwinds and Upcoming Catalysts

The backdrop for this high-stakes offer is a dynamic global energy market. As of today, Brent Crude trades at $98.41, reflecting a -0.99% change, with an intraday range of $97.92 to $98.58. WTI Crude is similarly down, trading at $90.13, a -1.14% shift, within a range of $89.57 to $90.24. This recent price action follows a notable trend: Brent crude has seen a significant decline from $112.57 on March 27, 2026, to $98.57 on April 16, 2026, marking a drop of approximately 12.4% over the past fortnight. Such volatility directly influences the perceived value of all-share transactions, as the underlying value of the offer fluctuates with the market price of Strathcona’s shares.

Looking ahead, several key events could introduce further market shifts, impacting the decision-making process for MEG shareholders. The upcoming OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting on April 18, followed by the Full Ministerial OPEC+ Meeting on April 20, are critical catalysts. Investors are keenly asking about OPEC+ current production quotas, and the outcomes of these meetings will directly shape global supply expectations and, consequently, crude prices. Any significant production adjustments could either bolster or challenge the valuation assumptions underpinning Strathcona’s offer. Furthermore, the regular Baker Hughes Rig Count reports (April 17, 24) and the API and EIA weekly inventory reports (April 21/22, 28/29) will provide ongoing insights into North American supply and demand dynamics, adding further layers to the complex investment calculus.

The Investor’s Dilemma: Cash Certainty vs. Future Upside

The Amended Offer by Strathcona forces MEG shareholders to weigh two fundamentally different paths for their investment. On one side, the Cenovus deal offers a more immediate, cash-heavy valuation, providing a degree of certainty but potentially limiting exposure to future growth in the long-life assets. On the other, Strathcona’s all-share proposal, now significantly enhanced, presents an opportunity to participate in a larger, combined entity with potential for greater upside, albeit with inherent market risks tied to commodity price fluctuations and the performance of the integrated company. Strathcona’s argument that the MEG Board Deal is “unfair” due to its “cash-heavy structure” and the “lopsided” market reaction (Cenovus shares rising ~10% post-announcement) aims to sway shareholders towards their vision.

With the Amended Offer set to expire at 5:00 p.m. Mountain Time on October 20, 2025, MEG shareholders face a crucial deadline. The decision hinges on their conviction regarding the long-term prospects of the combined Strathcona entity in a volatile energy market, juxtaposed against the more immediate, but potentially less upside-rich, alternative. Careful consideration of the strategic rationale, the projected financial strength of the combined entity, and the ongoing market catalysts will be paramount for maximizing shareholder value.