The global energy landscape continues its rapid evolution, presenting both significant challenges and compelling investment opportunities. In an environment marked by geopolitical shifts and an accelerating energy transition, the strategic build-out of critical infrastructure is proving paramount. Recent contract awards to Lithuania-based MT Group highlight a dual-pronged investment thesis: bolstering immediate energy security through LNG and laying foundational steps for a decarbonized future with green hydrogen.

Germany’s LNG Security Imperative: A Long-Term Infrastructure Play

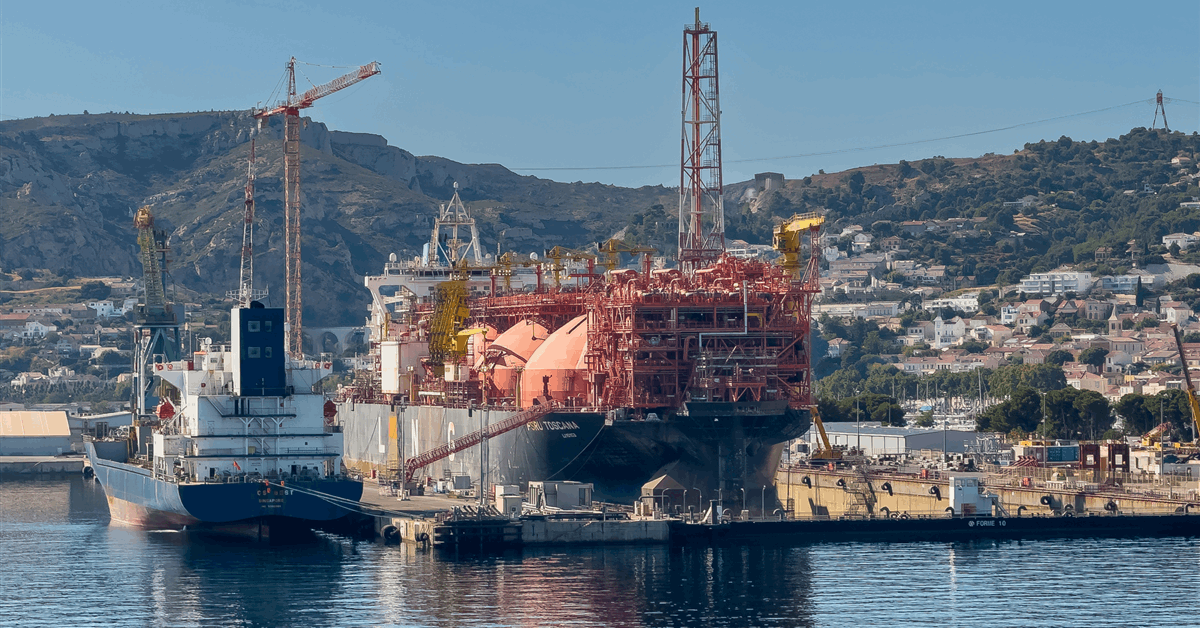

Germany’s swift pivot away from Russian pipeline gas has underscored the critical need for diversified energy supplies, making LNG infrastructure a cornerstone of its national energy strategy. MT Group’s major contract for the execution of all topside and onshore-based infrastructure at the Brunsbüttel FSRU LNG Terminal’s new jetty represents a significant step in solidifying this security. Awarded by Worley on behalf of Deutsche Energy Terminal GmbH, Germany’s state-owned FSRU operator, this agreement covers a full package of mechanical, piping, electrical, instrumentation, civil installation, and tie-in works into the existing grid system. This is part of Phase 2, which involves the permanent relocation and integration of the FSRU at its final jetty. For investors, this signifies a long-term commitment to LNG import capacity, moving beyond temporary solutions to create robust, lasting infrastructure.

This development is particularly relevant as our readers frequently inquire about the drivers behind Asian LNG spot prices. While short-term spot market volatility remains a factor, Germany’s investment in Brunsbüttel demonstrates a strategic imperative to secure reliable, flexible access to global LNG supplies, mitigating reliance on any single source or transient price fluctuations. This long-term vision for energy independence creates a stable demand environment for specialized EPC firms like MT Group, which also secured an earlier contract in October for a 50-megawatt heater facility at Brunsbüttel, showcasing its expanding footprint in this vital European energy hub.

Crude Market Headwinds: Shifting Capital to Resilient Infrastructure

The broader energy market context, particularly in crude, is characterized by notable volatility, influencing investor sentiment across the sector. As of today, Brent crude trades at $95.02, showing a marginal daily gain. However, this masks a broader softening trend, with the benchmark having fallen sharply by over 12% from its $108.01 level just two weeks ago. This significant downturn, alongside our readers’ consistent interest in base-case Brent price forecasts for the next quarter and year, underscores the prevailing uncertainty in commodity markets.

In this environment of fluctuating crude prices, investments in stable, government-backed energy infrastructure projects, such as the Brunsbüttel LNG terminal, become increasingly attractive. These projects offer more predictable revenue streams and are less susceptible to the immediate swings of commodity markets compared to upstream exploration or production ventures. For investors seeking both stability and strategic exposure to Europe’s evolving energy mix, the focus shifts towards critical midstream and downstream assets that underpin national energy security, providing a potential hedge against broader market turbulence.

The Green Hydrogen Horizon: Diversification and Future Growth

Beyond immediate energy security, MT Group’s activities also reflect the accelerating momentum behind the energy transition. The company, acting as the full-scope EPC provider for the Vilnius Green Hydrogen Production Facility in Lithuania, has awarded a major supply contract to IMI for a 3-MW PEM electrolyzer. This unit is destined for a facility designed to decarbonize district heating through locally produced green hydrogen, a joint initiative by Vilnius District Heating Company and Vilnius City Municipality.

This project is a clear indicator of the strategic diversification being undertaken by key players in the energy infrastructure sector. For investors, the Vilnius project offers a glimpse into the future energy mix, highlighting the long-term potential of green hydrogen as a decarbonization solution. While commissioning is planned for 2026, the current commitment to deliver equipment by the fourth quarter of this year signals tangible progress in an emerging, high-growth segment. Such ventures position EPC firms like MT Group at the forefront of the energy transition, offering exposure to innovative technologies and sustainable growth pathways.

Navigating the Next Fortnight: Macro Catalysts for Energy Investment

Investors looking for directional cues in the broader energy market will closely watch several key events over the next two weeks. The OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting on April 18, followed by the Full Ministerial Meeting on April 20, will be critical in shaping crude supply policy and, consequently, global oil prices. Any decisions from these gatherings could significantly impact the market sentiment for both traditional oil and gas and indirectly influence capital allocation towards alternative energy projects.

Further insights into market fundamentals will come from the recurring API Weekly Crude Inventory reports (April 21, April 28) and the EIA Weekly Petroleum Status Reports (April 22, April 29), which provide essential data on demand and supply balances. Additionally, the Baker Hughes Rig Count on April 17 and April 24 will offer a pulse on upstream activity. While these events primarily impact crude, their ripple effects are felt across the entire energy complex. Stable, long-term infrastructure investments like the Brunsbüttel LNG terminal or the Vilnius green hydrogen facility can offer a degree of insulation from the short-term market reactions driven by these macro catalysts, appealing to investors seeking resilience in a dynamic energy landscape.