The global oil and gas industry continues to demonstrate a strategic commitment to long-term resource development, a trend underscored by recent significant contract awards to major subsea engineering and construction firms. Subsea7 S.A. has notably bolstered its project backlog with substantial new wins, securing a “large” contract from Equinor for the Fram Sor development offshore Norway, alongside a “sizeable” award in Egyptian waters. These developments are not merely transactional successes; they represent critical indicators of sustained upstream investment, particularly in deepwater and brownfield expansion projects, signaling confidence in future hydrocarbon demand despite evolving energy landscapes. For investors, these contracts provide valuable insight into the operational stability and growth trajectory of key service providers within the energy infrastructure ecosystem.

Deepwater Resilience: Subsea7’s Strategic Wins in Norway

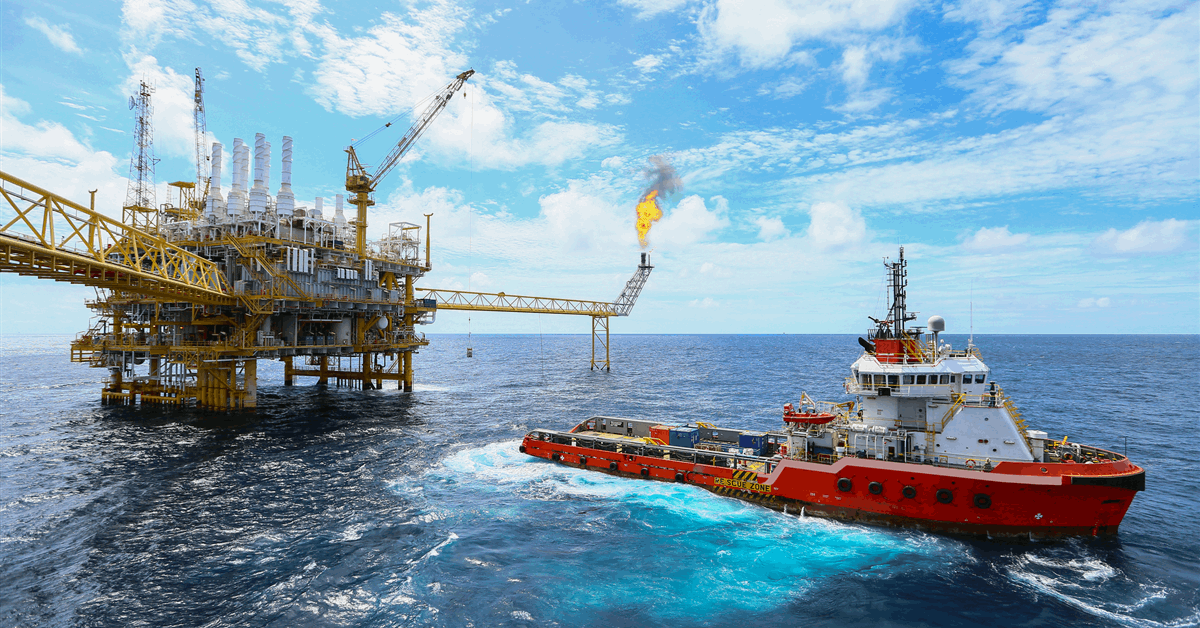

Subsea7’s latest engagement with Equinor on the Fram Sor development marks a significant endorsement of its deepwater capabilities and a continuation of a long-standing collaboration. Defined as a contract valued between $300 million and $500 million, this award encompasses the engineering, procurement, construction, and installation (EPCI) of crucial subsea structures and flowlines. Specifically, the scope includes 53 kilometers of production, gas lift, and water injection lines, alongside the installation of the umbilical system. This complex undertaking targets the Fram Sor area, situated north of the Equinor-operated Troll C platform, leveraging existing infrastructure for efficient tie-back. The project’s timeline, with offshore installation activities slated for 2026 through 2028, highlights the multi-year commitment involved in such deepwater endeavors. While the contract remains subject to authority approval of the Plan for Development and Operations (PDO), its progression from an earlier front-end engineering and design (FEED) study indicates a high probability of sanction. For investors tracking the Norwegian Continental Shelf (NCS), this project signals Equinor’s continued investment in maximizing recovery from mature areas, providing a stable revenue pipeline for specialized contractors like Subsea7.

Expanding Footprint: The Egyptian Offshore Opportunity

Beyond the established markets of the North Sea, Subsea7 has strategically expanded its operational footprint with a “sizeable” contract win offshore Egypt. Valued between $50 million and $150 million, this award, from an undisclosed client, involves the engineering, procurement, commissioning, and installation of flexible pipelines, umbilicals, and associated subsea components. The project’s focus on a tie-back to existing infrastructure aligns with a global trend of optimizing current assets and extending field life, a cost-effective approach for producers. Project management and engineering work have already commenced across Subsea7’s offices in France, Portugal, and Egypt, with offshore activities anticipated to begin in 2026. This diversification into key North African markets not only strengthens the company’s regional presence but also leverages its expertise in delivering innovative, efficient solutions for strategically important energy projects. The Egyptian contract underscores the growing demand for subsea services in emerging offshore provinces, driven by a desire to bring new gas and oil resources online to meet both domestic and export requirements.

Navigating Market Dynamics: Backlog Growth Amidst Price Volatility

These significant contract wins provide a robust foundation for Subsea7’s future earnings in an oil market that continues to present dynamic conditions. As of today, Brent crude trades at $94.85 per barrel, reflecting a marginal dip of 0.08% within a day range of $94.42 to $94.91. Similarly, WTI crude stands at $91.19, down 0.11%. Looking at the broader trend, Brent has seen a notable decline of 12.4% over the last 14 days, moving from $108.01 on March 26th to $94.58 on April 15th. This recent softening in crude prices, while not drastic, typically prompts investors to assess the resilience of upstream capital expenditure plans. However, the multi-year nature of projects like Fram Sor and the Egyptian tie-back demonstrates that major energy companies are making investment decisions based on long-term price outlooks rather than short-term fluctuations. This stability in contracting provides a critical buffer for subsea service providers, securing revenue streams well into the latter half of the decade. Investors are keenly asking about the base-case Brent price forecast for the next quarter and the consensus for 2026, and these contracts suggest that upstream operators, at least in the deepwater segment, are still budgeting for prices that support substantial investment.

Forward Outlook: Key Catalysts and Industry Indicators

Looking ahead, the formal authority approval of the Plan for Development and Operations (PDO) for the Fram Sor project will serve as a near-term catalyst for Subsea7, solidifying the “large” contract into the firm’s order book. Beyond specific project milestones, the broader market will be closely monitoring a series of upcoming events that could influence the overall investment climate for the oil and gas sector. The OPEC+ Joint Ministerial Monitoring Committee (JMMC) meeting on April 18th, followed by the full Ministerial meeting on April 20th, are pivotal. Any signals regarding production policy shifts from these gatherings could directly impact crude prices and, consequently, the appetite for new upstream developments. Furthermore, weekly indicators such as the Baker Hughes Rig Count, scheduled for April 17th and April 24th, will offer insights into drilling activity, while the API Weekly Crude Inventory (April 21st, April 28th) and EIA Weekly Petroleum Status Reports (April 22nd, April 29th) will provide crucial data on supply-demand balances. These data points, while focused on the short to medium term, collectively inform the long-term investment decisions that drive demand for subsea EPCI services. The consistent flow of substantial contracts into firms like Subsea7 underscores the industry’s unwavering commitment to securing future energy supplies, demonstrating a belief in sustained demand through the decade and beyond.