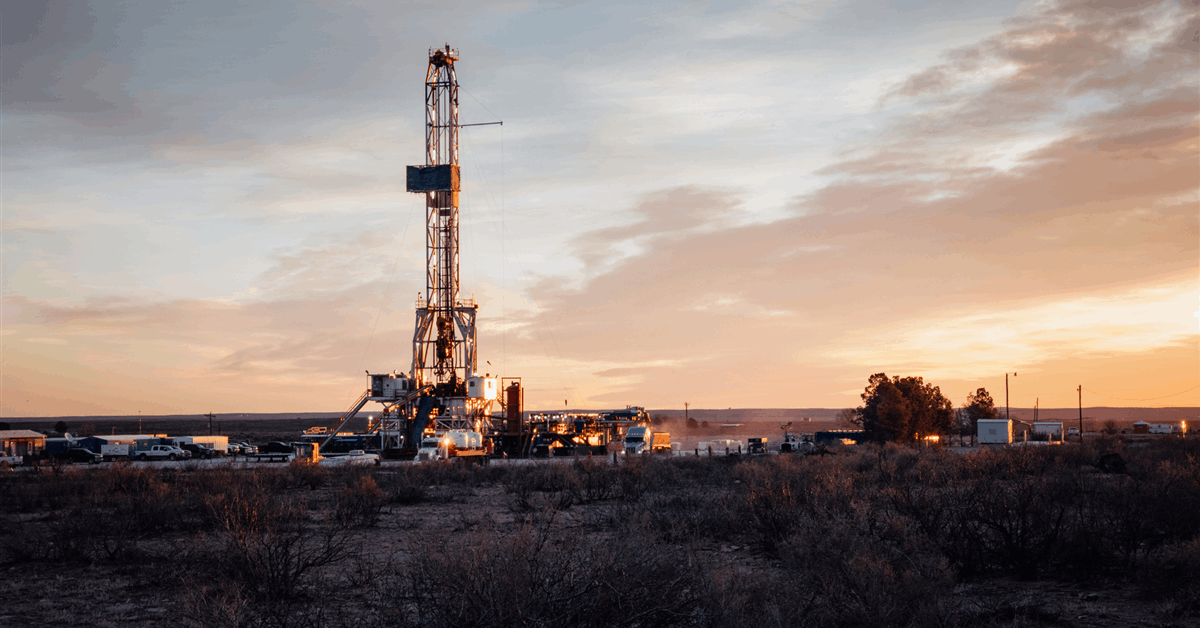

Introduction: Navigating the Adjusted Pathway for Rafael Gas

Buru Energy Ltd. has recalibrated the development timeline for its Rafael natural gas project in Western Australia’s Canning Basin, a strategic move designed to enhance resource certainty while maintaining the ambitious target of late 2027 for first cashflow. This adjustment, shifting the order of drilling activities, is a critical development for investors closely watching the maturation of Australia’s onshore gas resources. Rafael stands as the sole confirmed conventional gas and liquids source onshore Western Australia north of the North West Shelf Project, underscoring its pivotal role in regional energy security and supply for the Pilbara and Northern Territory. For investors, understanding the implications of this revised strategy is paramount to assessing the project’s long-term value and de-risked pathway.

Strategic Sequencing: De-risking Rafael’s Resource Potential

The core of Buru’s timeline adjustment lies in a revised drilling sequence: instead of recompleting the 2021 discovery well as a producer first, the company will now prioritize drilling and testing the Rafael B appraisal well. This pivotal shift, with drilling planned to commence in June 2026, is explicitly aimed at “reducing risk and increasing the probability of higher reserves.” This decision directly addresses a fundamental concern for investors: the certainty and magnitude of the resource base. The project’s current assessment of contingent and unrisked gross recoverable volumes, ranging from 85-523 Bscf of gas and 1.8-10.6 MMstb of condensate, represents a significant spread. By targeting Rafael B first, Buru intends to narrow this range, providing a more robust foundation for a Final Investment Decision (FID) and offering greater clarity on the project’s ultimate economic potential over its projected 20-year production life. This methodical approach to resource de-risking is a positive signal for those seeking long-term, stable returns in the upstream sector.

Macro Market Volatility vs. Domestic Project Resilience

The revised Rafael timeline unfolds against a backdrop of considerable volatility in global energy markets. As of today, Brent crude trades at $90.38 per barrel, representing a notable daily decline of 9.07%, while WTI crude sits at $82.59, down 9.41%. This recent dip is part of a broader trend, with Brent having fallen from $112.78 to $91.87 over the past 14 days, marking an 18.5% decrease. Gasoline prices have also seen a downturn, currently at $2.93, a 5.18% reduction today. While Rafael is primarily a domestic gas and condensate project, these macro price movements undeniably influence investor sentiment across the entire energy complex. The condensate component of Rafael’s production will be directly exposed to global crude prices, making the current market softening a factor to monitor. However, the project’s focus on supplying trucked liquefied natural gas (LNG) to the Pilbara and Northern Territory taps into a robust domestic demand curve, potentially offering some insulation from the wildest swings in international markets. Investors are keenly observing these trends, frequently asking about the trajectory of crude oil prices, with many seeking predictions for Brent by the end of 2026. Rafael’s strategic positioning to meet regional energy needs could provide a degree of resilience in an otherwise unpredictable global landscape.

Partnerships and Regulatory Support Paving the Way

Beyond the drilling sequence, two other critical elements bolster Rafael’s development pathway: a strategic partnership with Clean Energy Fuels Australia (CEFA) and crucial government approval. Earlier this month, Buru secured a two-year extension from Western Australia’s Mines, Petroleum and Exploration Department, pushing the deadline for a production license application to July 2027. This extension is vital, providing the necessary breathing room to complete “important work, including the maturation of technical and commercial work with our development partner.” The collaboration with CEFA is designed to create a comprehensive value chain, with CEFA owning the downstream components of the project. This partnership is particularly compelling as it combines Buru’s upstream resource and expertise with CEFA’s established downstream and midstream capabilities, strong financial backing, and existing footprint in the Western Australian domestic LNG market. The agreement outlines a business model as the basis for future binding agreements, expected to be executed in late 2025. This integrated approach, supported by regulatory flexibility, significantly de-risks the project’s commercialization path and enhances its attractiveness for long-term investors.

Upcoming Catalysts and the Broader Energy Horizon

For investors tracking Rafael, the immediate focus should be on the planned June 2026 commencement of drilling for Rafael B, a significant operational catalyst that will provide crucial data on resource confirmation. The broader energy market, however, offers a continuous stream of events that will shape the investment climate. In the coming days, the OPEC+ Joint Ministerial Monitoring Committee (JMMC) and the full Ministerial Meeting are scheduled for April 18th and 19th, respectively. Decisions from these meetings regarding production quotas will directly impact global supply dynamics and, consequently, the price environment for crude and condensate. This directly addresses one of the most frequent questions from our readership: “What are OPEC+ current production quotas?” Further market insights will come from the API Weekly Crude Inventory (April 21st, 28th) and EIA Weekly Petroleum Status Reports (April 22nd, 29th), which offer a granular view of U.S. supply and demand. The Baker Hughes Rig Count (April 24th, May 1st) will also provide a pulse on North American drilling activity. While Rafael is a long-term project with its own unique timeline, these macro-level events collectively contribute to the overarching investor sentiment and the economic models underpinning future energy developments. The successful execution of Rafael’s revised timeline, coupled with a favorable macro environment, positions the project as a compelling long-term investment in Australia’s evolving energy landscape.