The global oil market is poised for a significant shift as Venezuela, a nation once central to crude supply, signals a potential resurgence. Recent statements from U.S. Energy Secretary Chris Wright project a substantial increase in Venezuelan oil production, estimating a rise of 30% to 40% by 2026. This translates to an additional 300,000 to 400,000 barrels per day (bpd) entering the market, a development that could reshape supply dynamics and offer compelling investment opportunities. This analysis delves into the implications of this potential output surge, examining its impact on market prices, the geopolitical context driving this shift, and the critical upcoming events investors should monitor.

Venezuela’s Return: A New Supply Variable

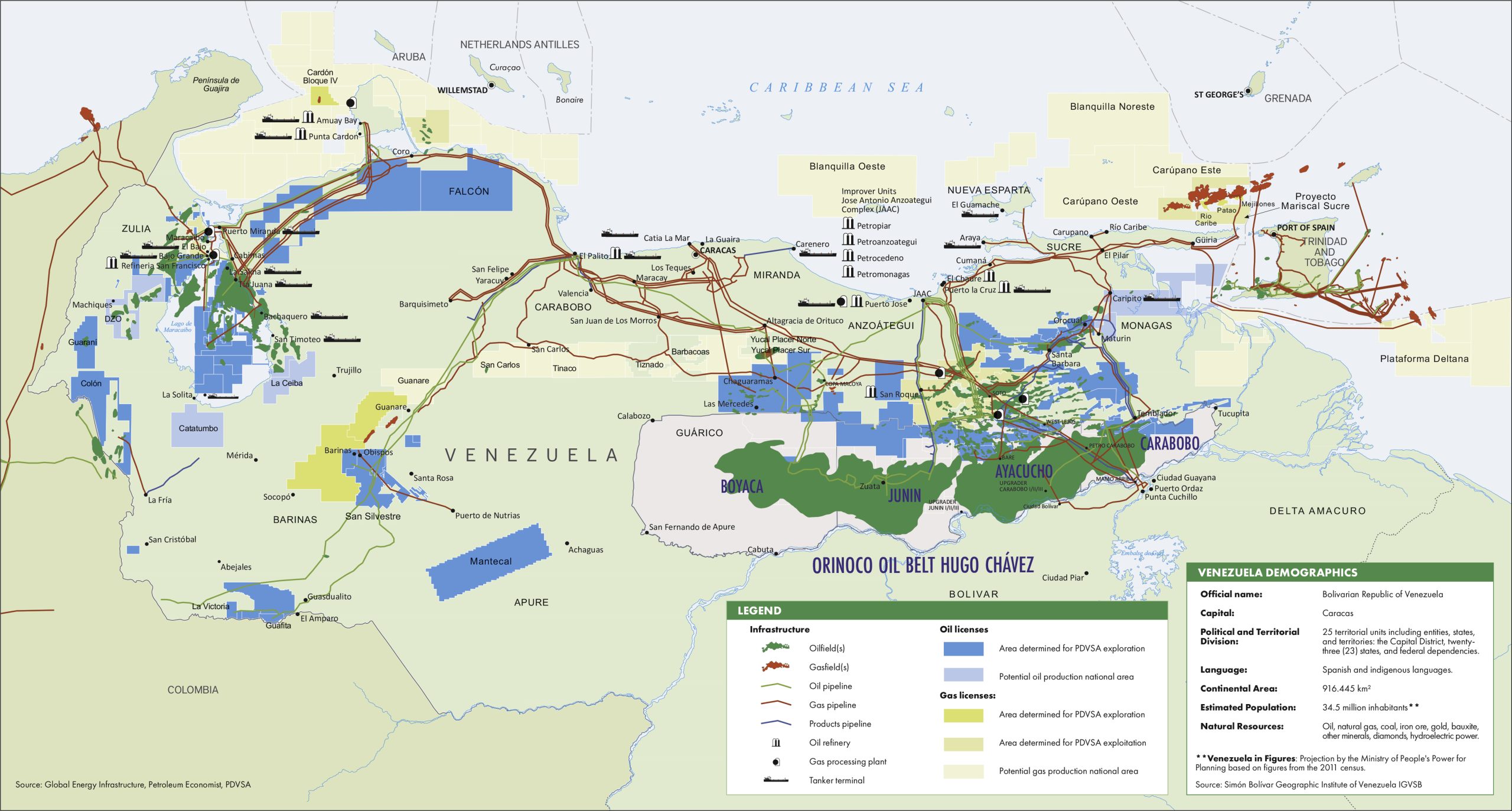

The prospect of Venezuela significantly boosting its oil output marks a pivotal moment for global energy markets. Secretary Wright’s projections of a 30-40% increase, or 300,000-400,000 bpd, by 2026 are not merely aspirational. They are underpinned by a tangible shift in U.S. policy and a renewed interest from international energy firms. This potential rebound is particularly striking given Venezuela’s dramatic production decline since 2017, when U.S. financial sanctions crippled its oil industry, causing output to fall by roughly half. The recent decision by the U.S. administration to issue licenses allowing certain Western oil companies to operate in Venezuela has opened the door for this recovery. Secretary Wright explicitly noted “enormous” interest among companies looking to re-engage with the Latin American producer, signaling a readiness to deploy capital and expertise to revitalize the nation’s vast crude reserves. For investors, this represents a new, potentially significant source of supply that could influence long-term price forecasts and create opportunities in associated service sectors.

Market Dynamics and Investor Questions in a Shifting Landscape

The potential return of substantial Venezuelan crude comes at a critical juncture for the global oil market. As of today, Brent Crude trades at $94.74, posting a robust 4.77% gain for the day, with WTI Crude similarly strong at $91.54, up 4.71%. Gasoline prices have also climbed, reaching $3.15, a 3.95% increase. However, this daily strength masks a recent period of volatility; the 14-day trend for Brent shows a significant correction, falling from $118.35 on March 31 to $94.86 on April 20, a nearly 20% decline. This inherent market volatility directly addresses the core concerns our readers frequently raise, such as “is WTI going up or down?” and “what do you predict the price of oil per barrel will be by end of 2026?” The reintroduction of Venezuelan supply adds a complex layer to these questions. While today’s market is showing bullish signs, sustained Venezuelan production increases, if realized, could exert downward pressure on prices in the medium to long term, especially if global demand growth moderates. Investors must weigh the immediate supply-side tightness against the looming potential for increased output from previously constrained sources like Venezuela, impacting their positioning in oil majors and related equities.

Geopolitical Realignments and Investment Pathways

The U.S. policy shift enabling Venezuela’s oil sector recovery is deeply rooted in geopolitical strategy. Following the capture of leader Nicolás Maduro earlier this year, the U.S. administration has actively sought to stimulate Venezuela’s oil industry and revive its local economy. This strategic pivot moves beyond punitive sanctions to a more pragmatic approach aimed at stabilizing the region and potentially diversifying global energy sources. For investors, this opens up specific avenues. Companies like Repsol, which readers have inquired about (“How well do you think Repsol will end in April 2026?”), or other Western firms that have previously operated in Venezuela, could be prime beneficiaries of this re-engagement. The “enormous interest” cited by Secretary Wright suggests a competitive landscape for re-entry, but also significant potential for those companies able to navigate the operational and political complexities. This involves not only direct exploration and production but also infrastructure development, refining, and export logistics, all of which will require substantial investment to bring Venezuela’s capabilities back to pre-sanction levels.

Critical Dates and Forward-Looking Analysis for Energy Investors

Monitoring upcoming energy events is paramount for investors seeking to capitalize on or mitigate risks associated with the evolving oil market, particularly with the new variable of Venezuelan output. The immediate calendar is packed with significant data releases and meetings that will shape market sentiment. On April 21, the OPEC+ JMMC Meeting will be closely watched; any indication of quota adjustments or commentary on global supply could influence prices, especially if the cartel begins to factor in potential non-OPEC+ increases from Venezuela. The EIA Weekly Petroleum Status Reports on April 22 and April 29 will offer crucial insights into U.S. crude inventories, refining activity, and demand, providing a snapshot of the world’s largest consumer market. The Baker Hughes Rig Count on April 24 and May 1 will illustrate drilling activity trends, a key indicator of future supply from North America. Finally, the EIA Short-Term Energy Outlook on May 2 is a must-read for any investor asking about 2026 price predictions. This report will provide updated forecasts, potentially incorporating the anticipated Venezuelan production increase and offering a clearer picture of the supply-demand balance. These events, combined with the geopolitical shifts, will collectively define the investment landscape for oil and gas throughout the remainder of 2026 and beyond.